Recent Academic Research

Global trading venue immunity, backtest edge survival, China's municipal guarantee erosion, and sequential geopolitical risk learning

Welcome back to another issue of Recent Academic Research!

Let’s get into it.

The Limited Reach of the World Cup Distraction Effect

The famous “World Cup distraction” that halves trading on national exchanges doesn't reach the global, round-the-clock markets where most money now moves, and two common ways of measuring it conjure the effect out of thin air.

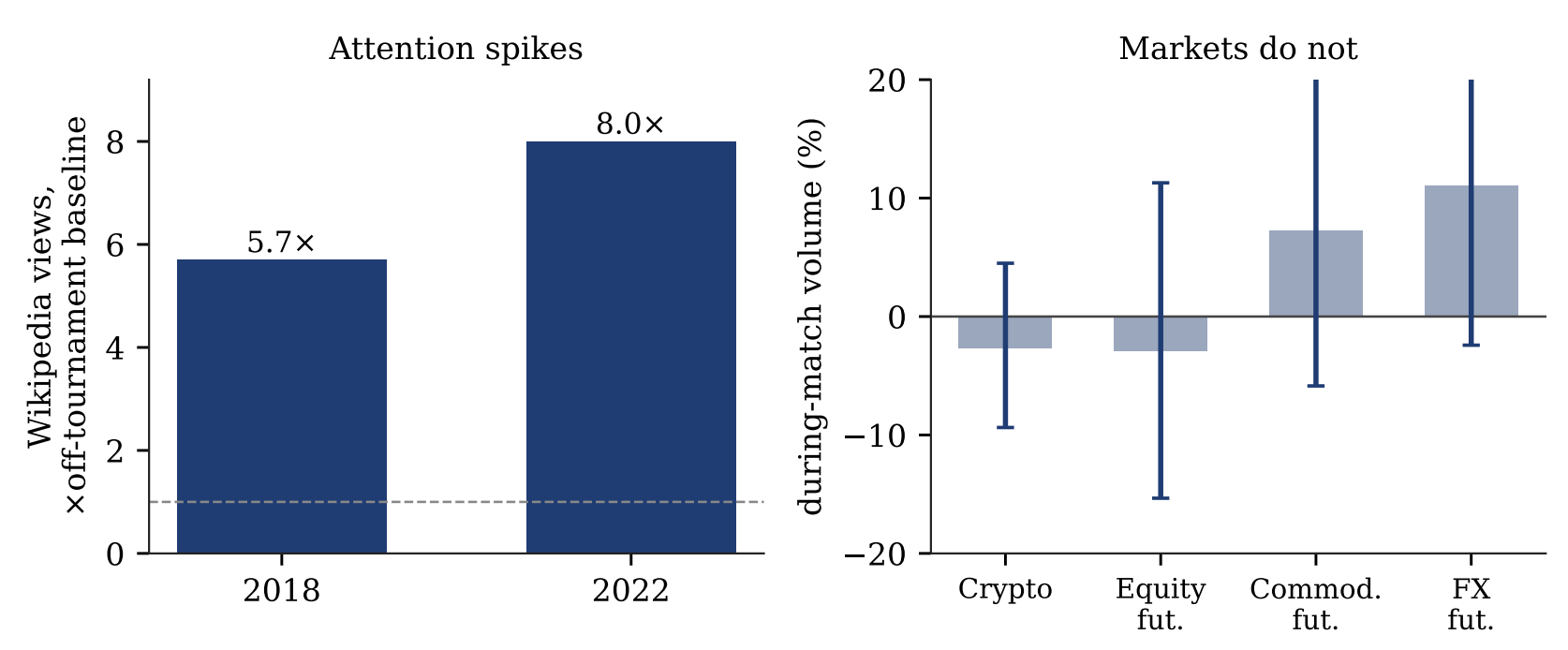

The original finding was clean: when a country's team plays, trades on that country's stock exchange drop sharply because the local trader is also the local viewer. The question now becomes whether that distraction survives in the venues that now carry most of the world's volume (crypto, index, commodity, and currency futures), where no single nation's fans matter to the price. Short answer: No. Across eleven instruments measured minute by minute, during-match trading sits flat on zero even as Wikipedia attention spikes to roughly six to eight times its baseline, and Gatto can statistically rule out declines beyond about 6 to 9 percent in the deepest markets, real nulls rather than weak tests.

Figure 1: World Cup attention jumps several-fold, but trading volume across global markets doesn't budge.

More useful for any data-driven investor is the warning underneath: two natural-looking measurements (a drop in cross-market correlation and an all-hours volume jump) reproduce the famous effect from no underlying response at all, driven purely by which instruments happen to be open. The lesson travels far beyond football: a “signal” can be an artifact of what your sample includes, and globally traded markets don't blink when any one country looks away.

Gatto, Daniel, The Reach of the World Cup Distraction Effect: Evidence from Global Trading Venues (June 16, 2026). Available at SSRN: https://ssrn.com/abstract=6955879

Measuring How Much of a Backtest's Edge Persists

A new diagnostic reveals how much of a trading strategy's “edge” actually survives once you stop fitting it to the past.

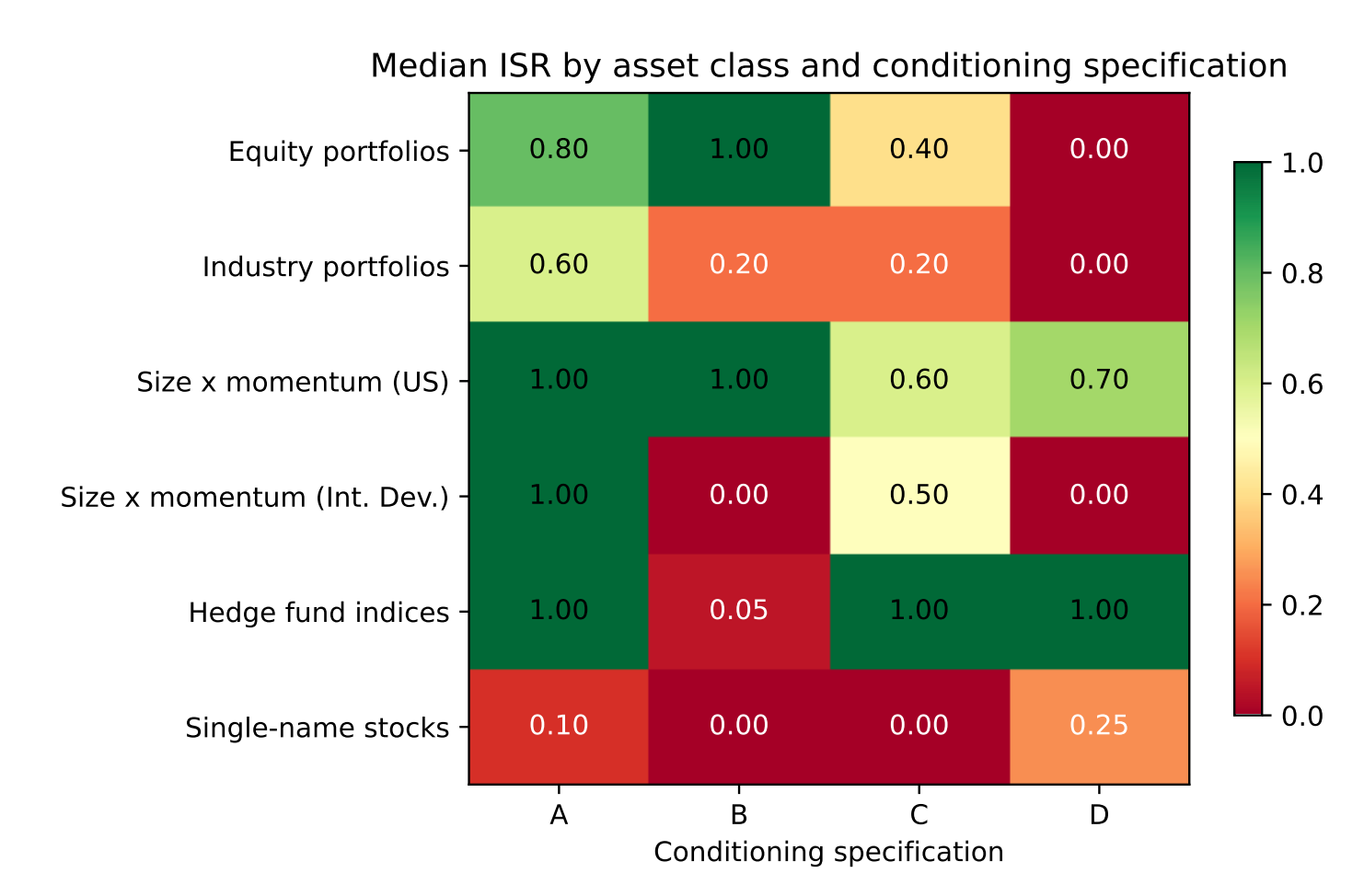

Most backtest-overfitting tools ask whether a strategy got lucky across many trials. This paper asks something different and arguably more useful: when a strategy uses market conditions (past returns, volatility, macro signals) to time its bets, how much of that conditioning information still works out-of-sample? Dominguez builds the information-survival ratio, a clean score from zero to one, where one means the in-sample edge fully carries over and zero means it collapses back to a plain unconditional benchmark.

Figure 2: Information-survival ratios across asset classes (rows) and signal types (columns). Greener cells mean more of the in-sample edge survives out-of-sample. Hedge funds retain the most, single stocks the least.

Tested across equities, industries, momentum portfolios, hedge funds, and single stocks, survival turns out to be highly uneven. Hedge fund indices retain the most conditioning power (often above 0.90), while individual stocks retain the least, drowned out by idiosyncratic noise. Crucially, no single type of signal wins everywhere: volatility works best for equities, while past returns dominate elsewhere.

For investors, the lesson is sobering and practical, a strong backtest means little if its underlying logic doesn't replicate forward, and this ratio puts a number on that risk.

Rodriguez Dominguez, Alejandro, The Information-Survival Ratio: A Within-Strategy Diagnostic of Conditioning Overfit in Walk-Forward Backtests (June 02, 2026). Available at SSRN: https://ssrn.com/abstract=6905139

How China’s Financing Shift Is Repricing Municipal Debt

When Chinese local governments swap land deals for proper bonds, the hidden safety net under their financing vehicles’ debt quietly frays, and investors notice.

For years, municipal corporate bonds (MCBs) in China have been priced cheaply not because the issuers were sound, but because everyone assumed the local government would quietly bail them out. This study tracks what happens when that assumption erodes. As provinces shift from land-sale-funded financing toward formal revenue bonds (debt explicitly backed by government credit), the implicit guarantee propping up MCBs weakens, and spreads widen.

The effect is real but not dramatic: a one-standard-deviation move toward this new model lifts issuing spreads by about 0.218 percentage points, roughly 11% of the average. Two forces drive it. Governments, leaning less on their financing vehicles, cut the subsidies and equity injections that signaled support, and the safer revenue bonds crowd out investor demand for riskier MCBs.

The pattern bites hardest where it should, on lower-rated bonds and land-dependent regions. For investors, it is a reminder that government backing, once treated as free, is being repriced in real time.

Du, Junying and Liu, Xinyang, From Land to Bonds: Local Government Financing Transformation and MCB Pricing in China. Available at SSRN: https://ssrn.com/abstract=6934485 or http://dx.doi.org/10.2139/ssrn.6934485

How Markets Learn from Sequential Geopolitical Escalations

Markets price geopolitical risk most aggressively the first time, then learn to shrug off later, broader shocks.

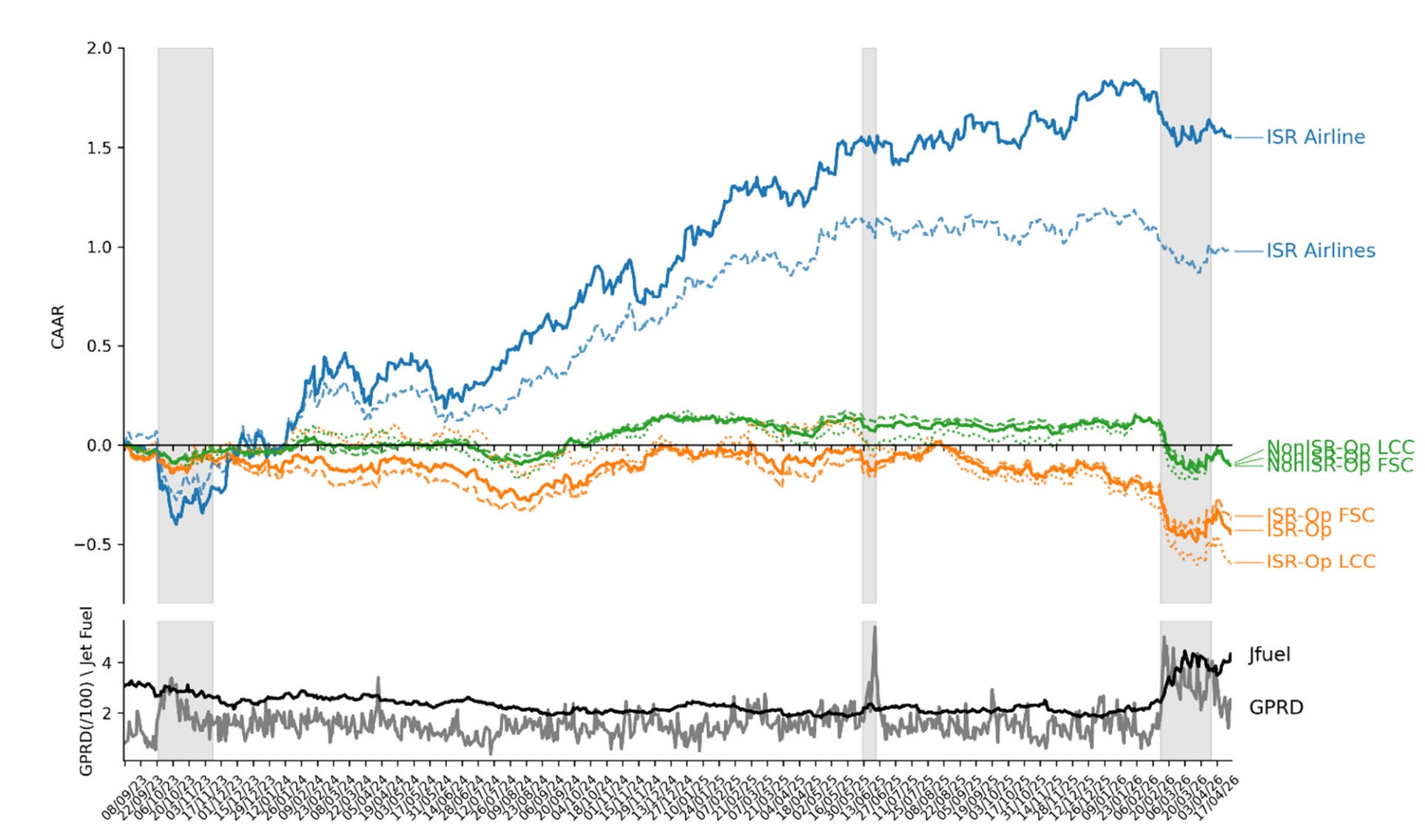

This study uses three escalations of the Israel conflict (a local attack in 2023, a regional fight with Iran in 2025, and a global episode involving the U.S. in 2026) as a natural experiment on how investors react to repeated bad news. Tracking 56 airline stocks, Kaplanski finds that the first shock was the one investors took most personally. Airlines with direct operational exposure to Israel, especially Israeli carriers and exposed low-cost airlines, got hammered hardest, while the rest of the industry was treated as relatively safe.

Figure 3: Cumulative abnormal returns for airline stocks, September 2023 to April 2026, grouped by exposure to Israel: Israeli carriers (ISR), airlines operating in Israel before the conflict (ISR-Op), and those without (NonISR-Op). Shaded bands mark the three escalation episodes. Lower panels show jet fuel prices and the geopolitical risk index.

But that exposure-based pricing didn't stick. By the regional escalation, the market barely flinched (the response was muted and short-lived despite the wider geographic scope), and by the global episode the selloff was broad and uniform, hitting everyone roughly equally rather than punishing the obviously exposed names. The paper shows that investors shifted toward “a broader reassessment of industry-wide risk.” For investors, the lesson is that the crowd's first reaction to a crisis tends to overshoot on the names that look most exposed, and that gap often reverses once the market recalibrates.

Kaplanski, Guy, Market Learning from Sequential Geopolitical Escalations: Evidence from Airline Stocks (March 05, 2026). Available at SSRN: https://ssrn.com/abstract=6847121

This week for paid subscribers

Paid subscribers are getting the full probability distribution of a European call option at expiry, derived from a 150-year-old physics equation (the Boltzmann framework) that delivers what Black-Scholes never did: not just the expected value, but the odds your option expires worthless and the range of payoffs if it doesn't. This post tracks that default probability daily as a live risk monitor, backtests its calibration across smooth and jump-prone markets (where it works, and where it systematically understates downside), and extends the result to VaR, credit models, and position sizing. Python backtest code included.

Disclaimer: The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.

The abnormal return gap between Israel exposed carriers and the broader basket seems to track GPRD spikes more than jet fuel. Cleaner signal there.