Recent Academic Research

Election shocks shift sector returns, sentiment and attention forecast volatility, ECB rate surprises ripple through Baltic labor markets

Welcome back to another issue of Recent Academic Research! What a week its been in the markets. Let’s take a moment to step away from the mayhem and cover the most interesting research papers on the markets in the past week.

Let’s get into it.

Improving Volatility Forecasts with Sentiment

This paper investigates whether sentiment and attention toward macroeconomic issues can improve forecasts of U.S. equity market volatility. While traditional volatility models often rely on historical price data, the authors incorporate textual data (news sentiment and public attention) to evaluate whether these signals add predictive value. They build on existing literature linking sentiment to returns but focus specifically on volatility forecasting, using sentiment and attention indicators based on machine learning classification and search data. Their methodology includes constructing daily measures of macroeconomic sentiment from news text and combining them with Google Trends data to capture attention. These variables are then integrated into a GARCH-MIDAS framework to assess their predictive power over various horizons.

Findings:

Including macroeconomic sentiment and attention measures significantly improves out-of-sample forecasts of equity market volatility relative to traditional models.

Sentiment about monetary policy and employment are particularly predictive of volatility changes, especially during uncertain times.

The forecasting improvement is more pronounced during high-volatility regimes, such as recessions or financial crises.

Models that account for both sentiment and attention outperform those using either one alone.

Macroeconomic sentiment leads market volatility, suggesting it contains forward-looking information not captured by historical price-based indicators.

These findings are robust across different forecast horizons and remain significant after controlling for other macro-financial predictors.

The improvement in forecasts likely stems from the fact that public sentiment and attention capture early signals of economic shifts, often before these are reflected in market behavior.

Halousková, Martina, and Štefan Lyócsa. "Forecasting US equity market volatility with attention and sentiment to the economy." arXiv preprint arXiv:2503.19767 (2025). https://arxiv.org/abs/2503.19767

Election Probabilities’ Market Impact

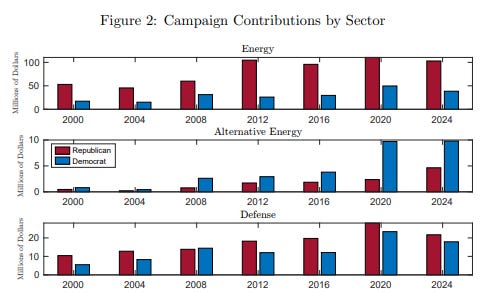

The paper investigates how unexpected election outcomes affect U.S. stock market sectors by linking shifts in sectoral stock prices to changes in political power. The authors use high-frequency stock market data around elections from 2000 to 2024 and focus on sectors that are especially sensitive to government regulation and spending (Energy, Alternative Energy, and Defense). They develop a novel event study approach that leverages betting market data to isolate unanticipated political shocks and identify causal effects. This method allows them to trace the impact of changes in expected election outcomes on sector-specific stock returns, avoiding typical post-election confounding noise.

Findings:

Energy sector stocks jump in response to increases in Republican election probabilities and fall when Democrats gain ground.

Alternative Energy stocks respond in the opposite direction, rallying on Democratic gains and falling on Republican advances.

Defense stocks perform well when Republicans are expected to win, but the effects are smaller and less persistent than in Energy.

These responses are strongest when control of the presidency or Congress is uncertain and swing elections are in play.

Campaign contributions align with market expectations: the Energy and Defense sectors predominantly support Republicans, while Alternative Energy favors Democrats.

These patterns likely arise because each party has well-known regulatory and spending priorities (Republicans support fossil fuels and defense, while Democrats back renewable energy) so markets quickly adjust to expected policy shifts when the balance of power changes.

Monetary Policy and Job Postings

This paper explores how monetary policy shocks (unexpected changes in interest rates) affect labor markets in the Baltic states (Estonia, Latvia, and Lithuania). While traditional studies use low-frequency data like employment rates, the authors innovate by using daily online job vacancy postings as a real-time proxy for labor demand. They identify monetary shocks using high-frequency changes in 6-month forward-looking OIS rates around European Central Bank policy announcements, isolating the impact of surprises rather than anticipated policy shifts. The empirical strategy employs local projections to trace the daily effects of these shocks on job postings from 2018 to 2024.

Findings:

A 1 percentage point surprise interest rate hike leads to a 2% drop in online job postings within 15 days on average across the three countries.

Conversely, an unexpected monetary easing raises job postings by a similar magnitude.

Lithuania shows the most persistent and severe response, with a 3.2% decline, followed by Estonia (2%) and Latvia (0.5%).

The negative effects in Estonia and Latvia tend to fade after about a month, while in Lithuania they remain longer-lasting.

These patterns hold even after controlling for COVID-19 policy measures and alternative measures of monetary stance like shadow rates.

The lagged and varied effects likely reflect differences in how flexible each country’s labor market is and the degree to which local economies are sensitive to ECB policy decisions.

Cevik, Serhan and Fan, Alice and Naik, Sadhna, Monetary Shocks and Labor Markets. IMF Working Paper No. 2025/058, Available at SSRN: https://ssrn.com/abstract=5201457 or http://dx.doi.org/10.5089/9798229005524.001

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.

Hmmmm. Interesting. Thank you.

Re: Monetary policy & Baltic Labor Markets. Interesting piece. Do the authors offer any casual or off the cuff empirical arguments that would explain the differences by country. Are there labor rigidities in one country not shared by the others? Are there institutional issues around postings for example and the speed with which they are changed. It would be interesting to posit such and then look for a labor market (e.g., Finland or Poland) where such did not happen in the same way as Baltics to confirm or reject. [Here's what I mean. In my past, we once verified a type of payday effect in stock prices (as opposed to a naive calendar effect) and conjectured a pay period specific mechanism. We tested the conjecture by going to a country with a different pay period that did not line up in the same way with the calendar. We found a similar payday phenomenon. Anecdotally then, we confirmed the stock price effect was likely due to the pay period rather than the calendar.]. Such would be interesting here especially if the rationale exposes an institutional rigidity or practice. Fun piece.