Recent Academic Research

The predictability of monetary policy surprises, turn-of-the-month in ETF spreads, the mathematical case for US market concentration, and optimal hedging for the 60/40 portfolio

Welcome back to another issue of Recent Academic Research! Let’s get into it.

Turn-Of-The-Month in ETFs

The most robust anomaly that Alpha in Academia has discovered, with applications across asset classes.

Vojtko and Dujava dig into the mechanics of month-end flows, uncovering a structural “liquidity premium” that arises from institutional rebalancing and liquidity constraints. Massive flows from pension funds and endowments create dislocations in the bond market, which propagate into rate-sensitive equity sectors like Real Estate and Value stocks. This pressure forces them to temporarily dislocate from the broader market, creating an exploitable spread between Real Estate (IYR) and the S&P 500 (SPY), as well as Value (IVE) versus Growth (IVW).

The resulting strategy involves entering these spreads during the final three trading days of the month to capture a predictable “spike-and-revert” profile. It is a trade on market plumbing, and these calendar-based distortions are “statistically and economically significant.”

Vojtko, Radovan and Dujava, Cyril, The End-Of-Month Effect in Value-Growth and Real-Estate-Equity Spreads ⋆ (October 20, 2025). Available at SSRN: https://ssrn.com/abstract=5631030 or http://dx.doi.org/10.2139/ssrn.5631030

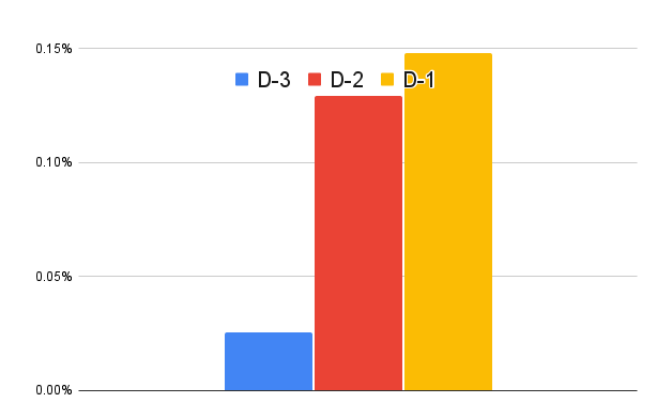

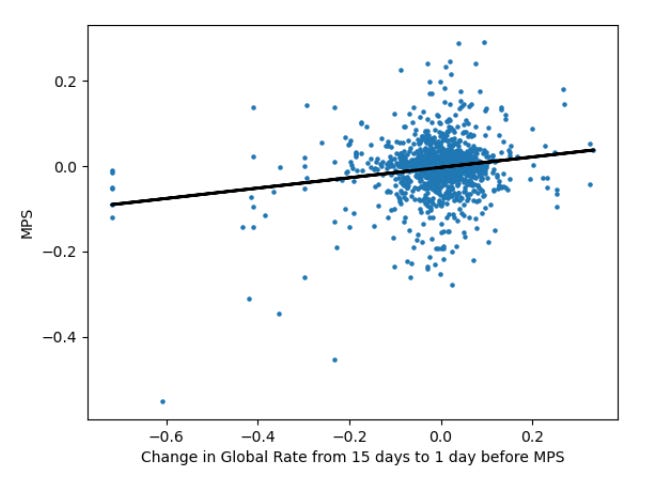

Monetary Surprises

It turns out financial markets are surprisingly bad at pricing interest rate decisions even when the clues are hiding in plain sight.

Christopher Cotton’s research exposes a persistent inefficiency where markets systematically misprice interest rate changes around central bank announcements. The predictor lies in global interest rates. Specifically, a rise in global short-term rates over the preceding 15 days reliably signals a “surprise” increase at the next central bank meeting.

This happens because investors seem to have a blind spot for the global interest rate cycle, consistently underreacting to how interconnected monetary policies actually are. The data suggests that markets treat these signals with too little faith, failing to adjust expectations until the announcement forces their hand.

Cotton, Christopher D. and Cotton, Christopher D., The Predictability of Global Monetary Policy Surprises (November, 2025). FRB of Boston Working Paper No. 25-14, Available at SSRN: https://ssrn.com/abstract=5843464 or http://dx.doi.org/10.29412/res.wp.2025.14

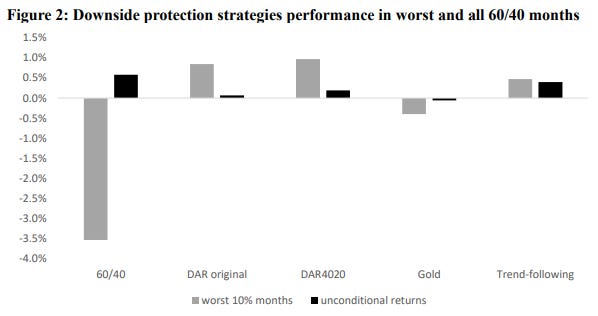

Optimal Hedging

After reviewing two hundred years of financial history, it appears that gold and put options are terrible ways to protect the 60/40 portfolio.

Baltussen et al. take a massive dataset spanning back to 1800 to find what actually works when the traditional 60/40 portfolio collapses. The results are a bit of an indictment on traditional safe havens, as gold proves unreliable and put options are simply too expensive to hold structurally. The real winners in downside protection turn out to be trend-following strategies and a “Defensive Absolute Return” approach that goes long factors with negative correlation to the market and short those with positive correlation.

The magic happens when combining them, as the defensive factor strategy reacts immediately to crashes while trend-following takes a moment to align but catches the sustained moves. For investors, this highlights that true diversification requires “robust defensive mechanisms” rather than just hoping precious metals will shine when stocks fall.

Baltussen, Guido and Martens, Martin and van der Linden, Lodewijk, The Best Defensive Strategies: Two Centuries of Evidence (November 25, 2025). Available at SSRN: https://ssrn.com/abstract=5815464 or http://dx.doi.org/10.2139/ssrn.5815464

A Pitch for U.S. Equities

Despite the constant hand-wringing over high valuations, holding sixty percent of your portfolio in US stocks might actually be the rational mathematical choice.

HSBC Asset Management tackles the anxiety surrounding the dominance of US equities in global indices, which currently sit above 60 percent of the MSCI All Country World Index. While a P/E ratio of 26 looks expensive compared to Europe or Japan, simply looking at valuation ignores the risk side of the equation.

By reverse engineering the expected returns required to justify current market caps, the authors find that US equities do not actually need heroic growth assumptions to make sense. Because the US market historically displays lower volatility and lower correlation to other regions, the optimizer naturally craves more of it.

Even when plugging in identical return assumptions for every country, the math still demands a US weight near 60 percent. It suggests that concentration risk is perhaps less dangerous than the risk of underweighting the world’s most efficient volatility dampener.

Battistella, Arnaud and McLoughlin, Nicholas, How much is too much? Part 1: Why 60% in US equities isn’t as crazy as it might sound (June 12, 2025). Available at SSRN: https://ssrn.com/abstract=5291789 or http://dx.doi.org/10.2139/ssrn.5291789

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.

Fantastic curation here! The turn-of-the-month ETF anomaly is particularly compelling because it ties directly to structural market plumbing rather than behavioral biases. What's intresting is how these institutional rebalancing flows create predictable dislocations that persist despite being well-documented. The fact that it works across Real Estate and Value sectors suggests the liquidity premium isn't arbitraged away easily, probably because the timing constraints are real and unavoidable for large fund managers.