Recent Academic Research

When markets stop behaving the way we assume: gold's hedge quietly failed, bond futures spreads hide real costs, stock prices are flashing a crisis signal, and sanctions slowed arbitrage.

Welcome back to another issue of Recent Academic Research!

Let’s get into it.

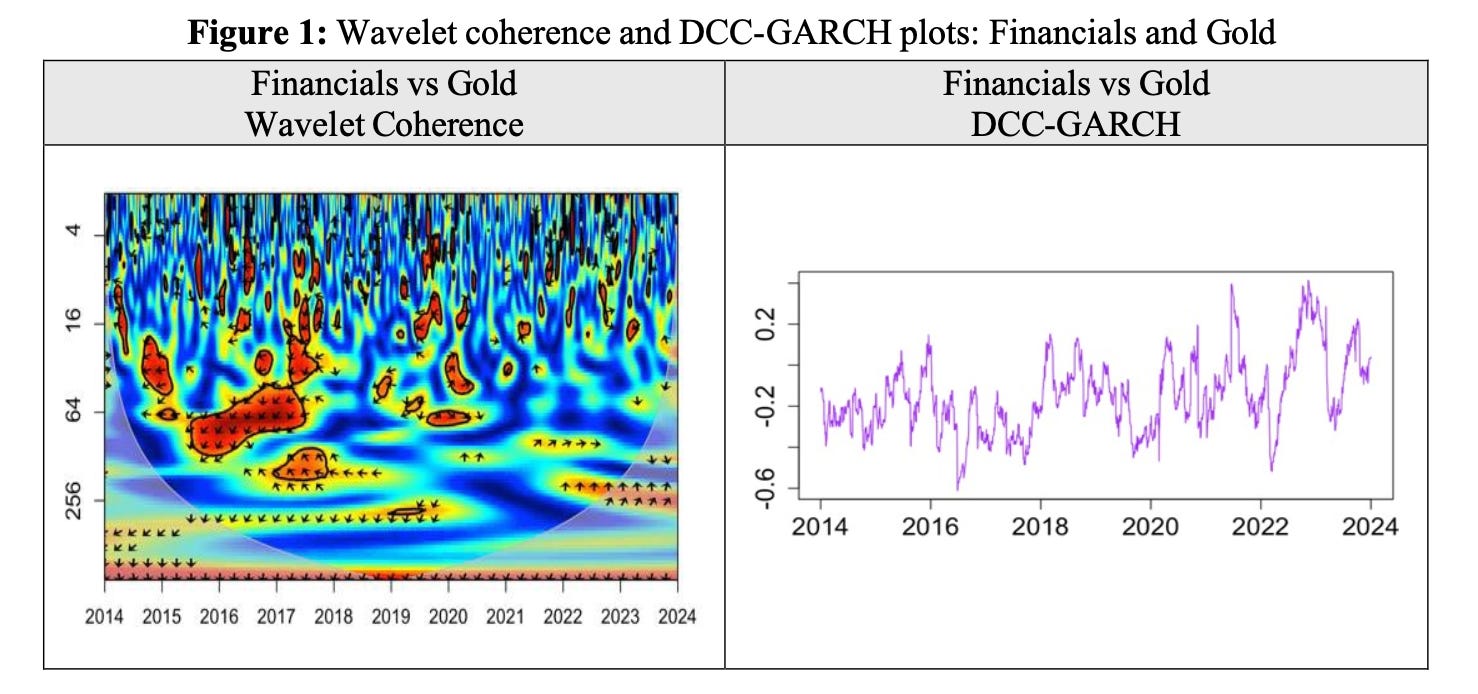

Gold's Hedge Is Cracking

Gold’s decades-old reputation as the market’s default safe haven quietly broke down after COVID, while unglamorous soft commodities like corn and wheat became meaningfully better portfolio diversifiers.

Researchers at the University of Cape Town and Stellenbosch tracked how seven commodities, three “hard” (gold, silver, platinum) and four “soft” (corn, soybeans, wheat, livestock), moved alongside eleven US equity sectors from 2014 to 2024, using wavelet coherence and DCC-GARCH models to capture how correlations shift across both time and investment horizon. The headline result: gold, long treated as the default flight-to-safety trade, went from negatively correlated with sectors like financials and industrials before the pandemic to increasingly positively correlated after it, stripping away the protection investors assumed was there.

Silver and platinum told a similar story, drifting toward stronger positive co-movement with cyclical sectors like materials and energy. Soft commodities never became strong safe havens either, but corn and wheat held up better, with optimal portfolio weights rising across every sector during COVID. As the authors put it, gold’s “traditional role as a strong safe haven and hedge asset deteriorated after the COVID-19 pandemic.” Anyone still parking risk in gold out of habit might want to check whether that hedge is actually still there.

Grant, Mark and Moodliar, Bhavaniya and Rissik, Luke and Huang, Chun-Sung, On the Hedge and Safe Haven Properties of Soft and Hard Commodities: Evidence from the United States GICS-Sectors (March 01, 2025). Available at SSRN: https://ssrn.com/abstract=7046078 or http://dx.doi.org/10.2139/ssrn.7046078

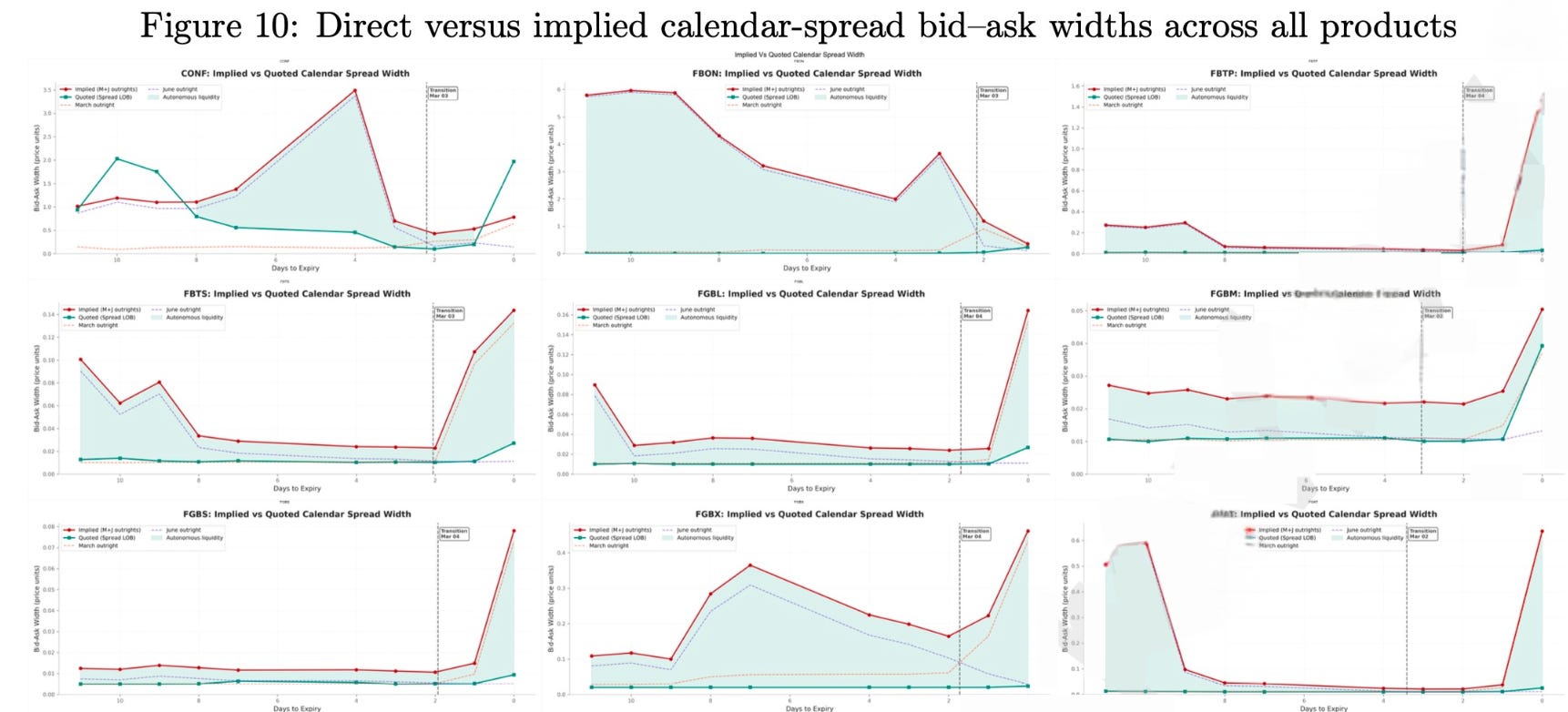

Bond Futures Spreads That Trade Like Their Own Market

European government bond futures calendar spreads aren’t just a synthetic byproduct of two expiring contracts, they behave like an independent liquidity venue precisely when rollover pressure peaks.

Using 127 million order book updates from nine EUREX bond futures (Bund, Bobl, Schatz, BTP, OAT, and others), this paper tracks what happens in the ten days before contract expiry across three linked markets: the expiring contract, the new contract, and the calendar spread connecting them. The expected story plays out late, trading activity and tighter quotes migrate from the old contract to the new one mostly in the final two or three days. But the spread book gets interesting earlier. It builds up meaningful resting depth well before that late migration, and for eight of nine products, buying the spread directly is consistently cheaper than manually legging into both contracts separately, sometimes dramatically so in less liquid names like the Spanish BONO future.

The authors put it plainly: calendar spreads play an active and economically meaningful role within the rollover process. For anyone rolling futures positions near expiry, that’s a real, quantifiable execution cost sitting on the table if you’re not checking the spread book first.

Uzun, Illia and Stenfors, Alexis, Calendar Spreads as Autonomous Liquidity Pools: Evidence from Triangular Rollover Dynamics in Bond Futures Markets. Available at SSRN: https://ssrn.com/abstract=6999365 or http://dx.doi.org/10.2139/ssrn.6999365

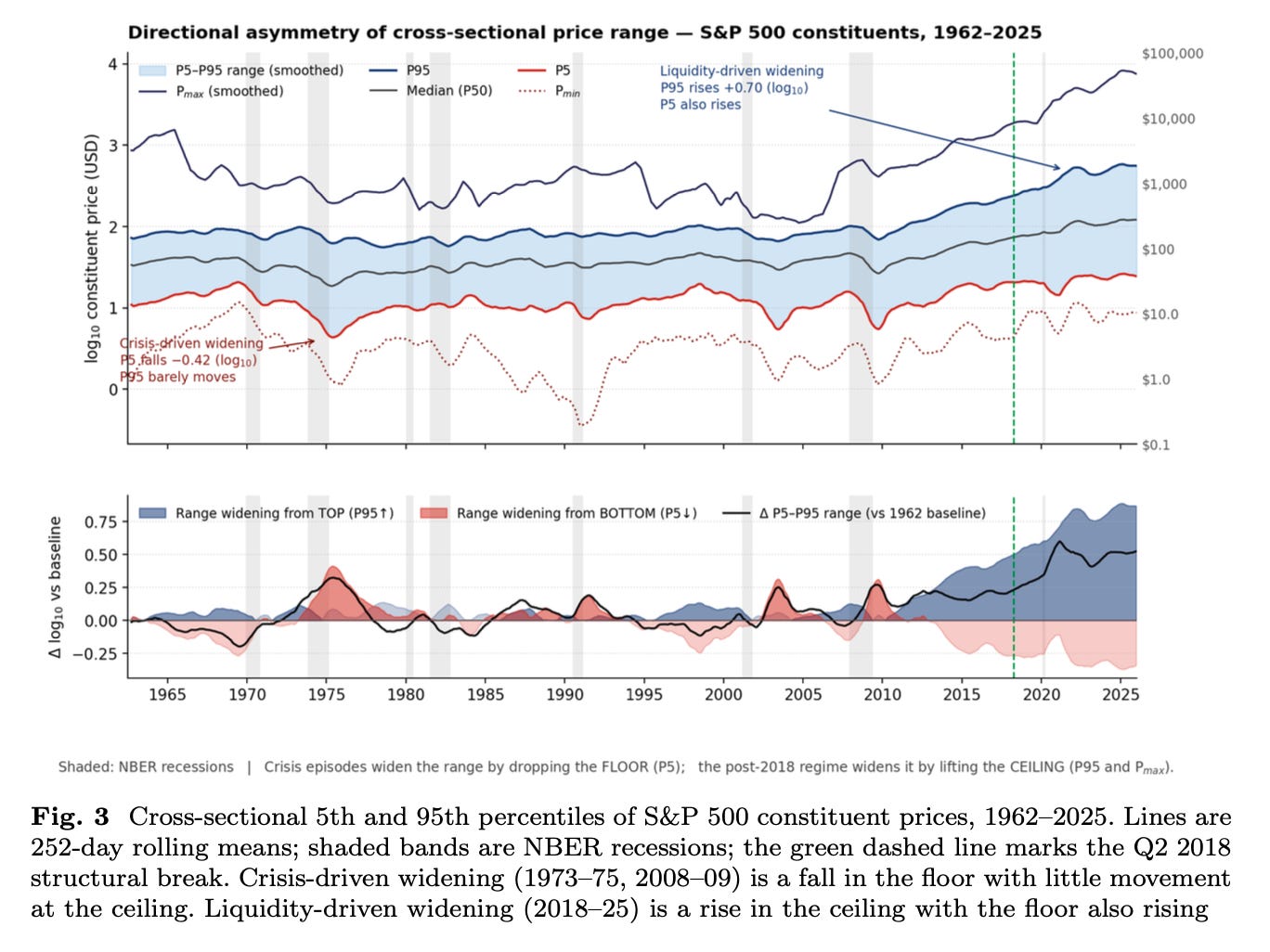

A Number Theory Trick Just Flagged Something Weird About This Bull Market

Since 2018, S&P 500 stock prices have started obeying Benford’s Law (the odd rule that natural datasets favor digit 1 over digit 9) more strongly than at any point in 64 years, and historically that pattern only ever showed up during a crisis.

Here’s the setup. Benford compliance in stock prices, it turns out, isn’t some mysterious market-efficiency signal, it’s almost entirely explained by how spread out prices are across the S&P 500 (one variable alone explains 82% of it). For 60 years, the only thing that stretched prices out enough to trigger strong compliance was a recession, and specifically a recession that crushed cheap stocks while expensive ones barely moved. Every time that happened (1970s oil crisis, 2008 crash), the pattern reverted within months once the economy recovered. But since 2018, the same statistical fingerprint has shown up for seven straight years with no recession attached, and it’s happening for the opposite reason: expensive stocks are rising fast while cheap stocks barely budge, not falling.

The paper ties this directly to M2 growth, and the authors frame it plainly, calling it the statistical configuration of crisis without its macroeconomic expression. If the plumbing that normally corrects stretched valuations (bankruptcies, recessions, deleveraging) has been sitting dormant this whole time, that’s worth knowing before you assume “no recession” means “no fragility.”

Mateos Sanchez, Carlos and Alcaraz Carrillo de Albornoz, Vicente and Farkas, Walter, The Signal beneath the Calm: Benford's Law and the Latent Fragility of Liquidity-Driven Financial Markets (June 17, 2026). Available at SSRN: https://ssrn.com/abstract=6962319

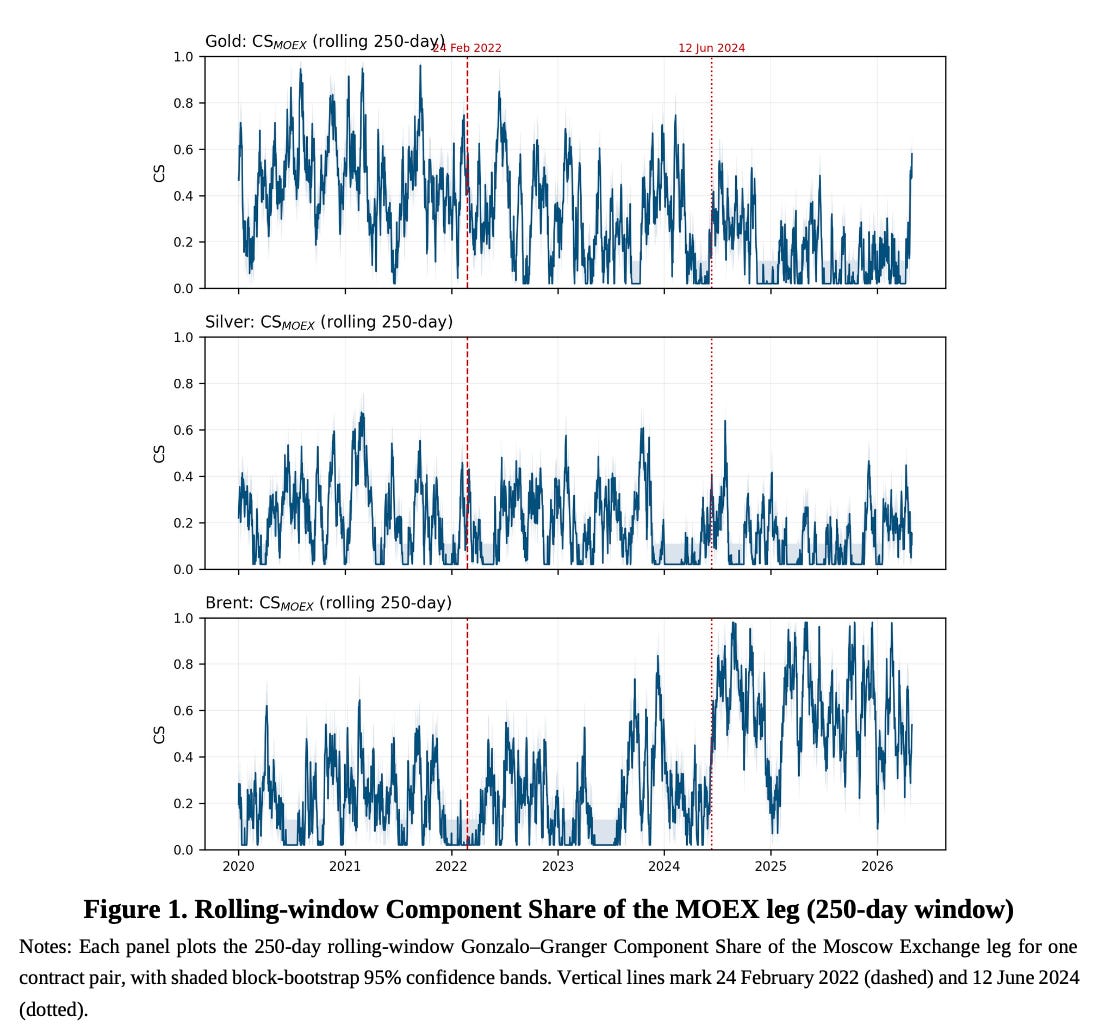

Sanctions Didn't Kill the Gold Arbitrage, They Just Slowed It Down (And Flipped Brent Entirely)

After Russia’s 2022 clearing and settlement infrastructure was severed from the West, gold and silver prices on the Moscow Exchange kept tracking their Chicago counterparts almost perfectly in the long run, but the market lost its ability to correct short-term price gaps quickly, while Brent crude oddly became more important to price discovery, not less.

Researchers compared Moscow Exchange futures on gold, silver, and Brent crude to their Chicago and ICE equivalents from 2019 through early 2026, using the kind of statistical toolkit normally applied to cross-listed stocks or ETFs tracking the same asset. The long-run one-to-one price relationship never broke, even after sanctions cut off Russian banks and brokers from global clearing. What changed was speed: it used to take one or two trading days for a price gap between Moscow and Chicago gold to close, and now it takes up to five.

Gold’s informational role on the Moscow exchange nearly vanished, but Brent’s grew, likely because the contract increasingly reflects discounted Russian crude rather than the global benchmark. As the authors put it, “the relation survives, but the mechanism that enforces it is impaired.” For anyone modeling cross-border arbitrage or basis risk, that’s a useful, quantifiable lesson in how sanctions actually degrade a market.

Belanov, Aleksandr and Mischhenko, Viatcheslav, Price Discovery and Arbitrage Efficiency under Infrastructure Severance: Evidence from MOEX-CME Derivative Pairs, 2019-2026 (June 07, 2026). Available at SSRN: https://ssrn.com/abstract=6915859

Disclaimer: The content provided in this newsletter, “Alpha in Academia,” is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.