Recent Academic Research

Adverse selection break-even traps, content-specific investor disagreement, bond ETF redemption fragility, and inherited regional risk appetite

Welcome back to another issue of Recent Academic Research!

Let’s get into it.

Adverse Selection Eats the Spread

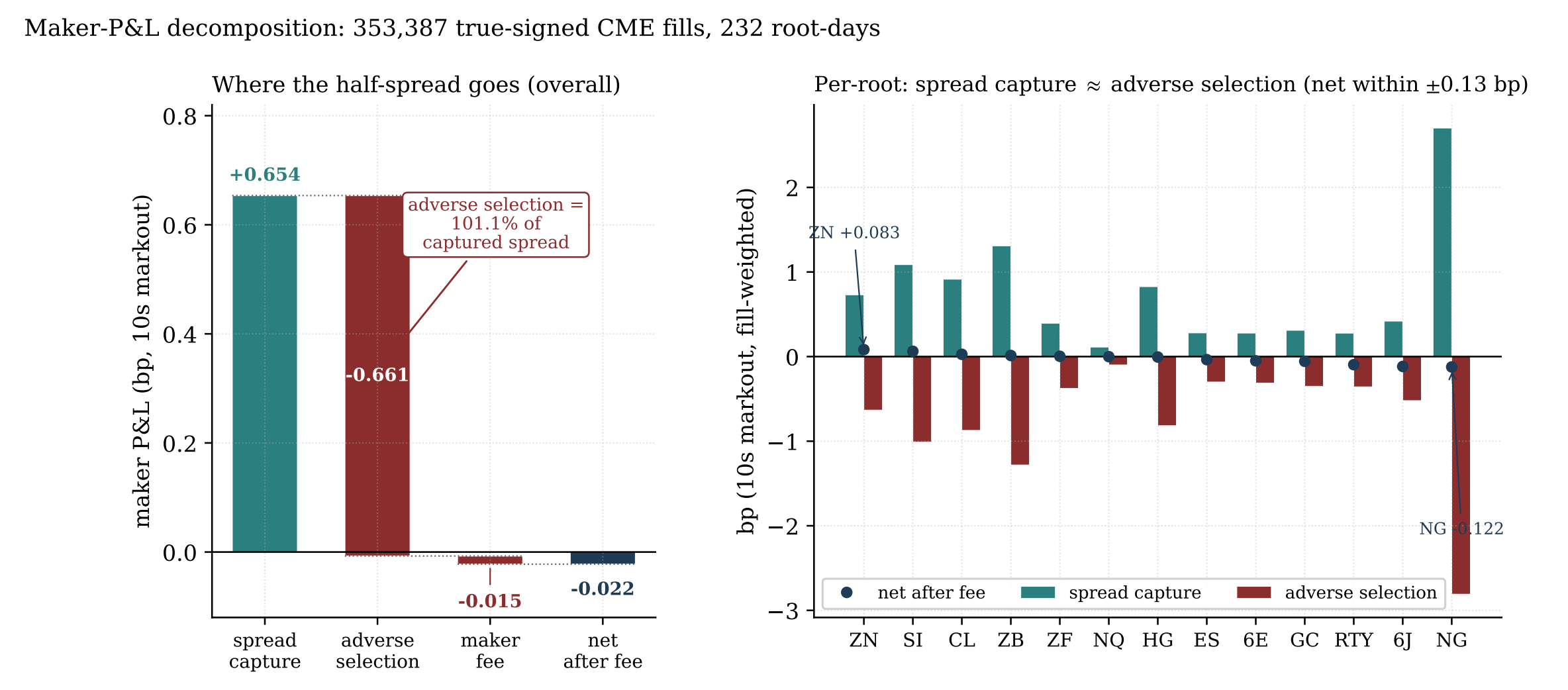

On a diverse basket of CME futures, the spread a market maker earns is almost perfectly cancelled out by the losses it pays to better-informed traders, leaving profit indistinguishable from zero.

When a market maker posts a passive quote, it collects a small spread but pays a hidden cost every time a smarter trader picks off that quote just before the price moves. Using rare data that carries the true buyer-or-seller sign on every trade across 13 CME futures (from crude oil to the S&P 500), Gatto measures both sides of that trade fill by fill and finds they essentially offset: the maker captures a sliver of spread and gives back almost exactly the same amount as prices drift against it, on every single contract.

Figure 1: Left: the half-spread a maker captures is consumed almost entirely by adverse selection, netting near zero. Right: the same near-cancellation holds on all 13 contracts.

In the author's words, “adverse selection consumes essentially the whole captured half-spread,” leaving profit statistically indistinguishable from zero. But under stress (the SVB scare, a hot FOMC week, the COVID crash) the losses actually exceed the spread, and the maker bleeds more as volatility rises. Standard clever quoting tricks and order-flow signals fail to fix it once real trading costs are charged. For investors, the takeaway is sobering, knowing that in these venues, passively supplying liquidity is structurally a break-even-at-best business, and the edge everyone chases mostly is not there.

Gatto, Daniel, Adverse Selection Consumes the Touch: A True-Aggressor-Signed Maker-P&L Decomposition Across 13 CME Futures (June 20, 2026). Available at SSRN: https://ssrn.com/abstract=7022599

What Investors Disagree About

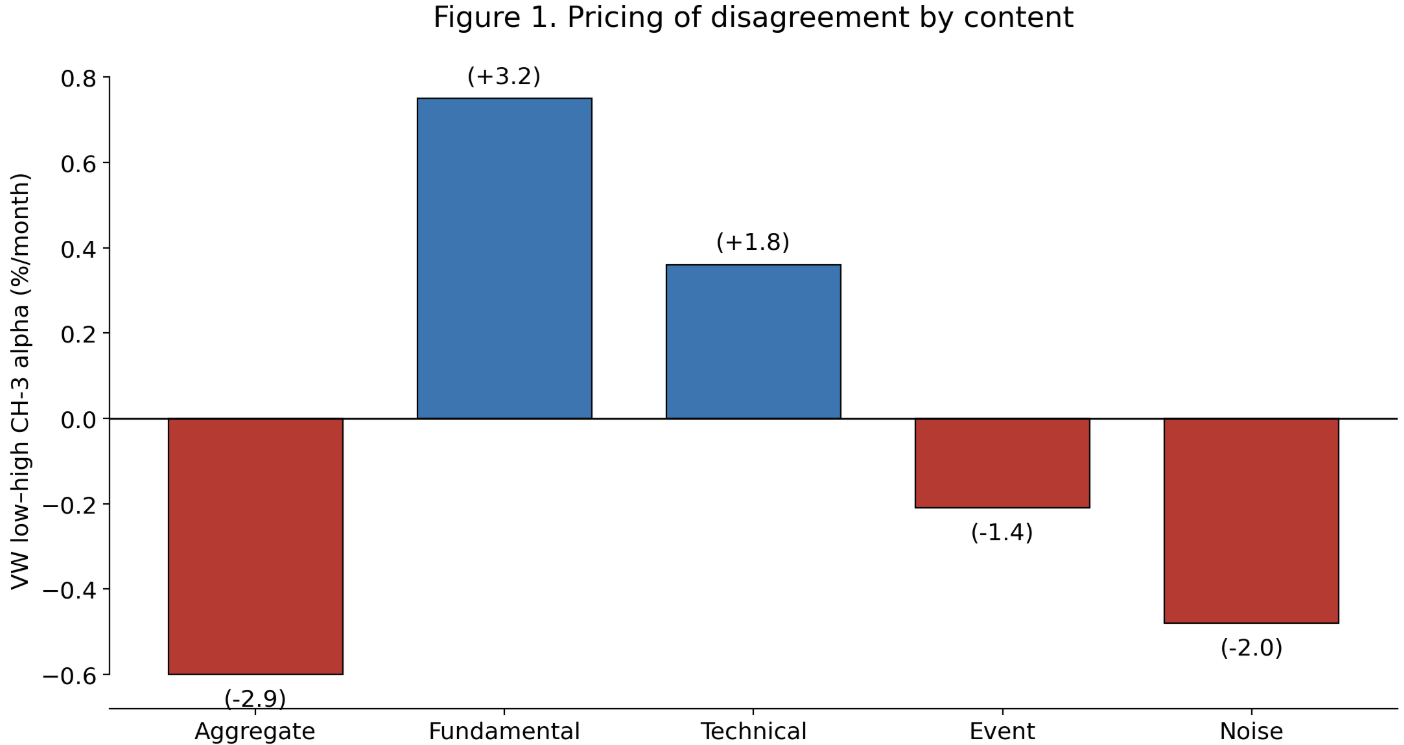

When investors argue about a company's actual fundamentals, that disagreement predicts lower future returns, but the same fights over noise and chatter predict nothing.

Most research treats investor disagreement as a single number, a measure of how much people argue without asking what they argue about. This paper ran a large language model over 220 million posts on China's biggest stock forum and split the arguing into categories. The result is that content is everything. Disagreement about fundamentals (earnings, valuation, prospects) predicts lower returns of roughly 0.7% per month, the classic pattern where optimists dominate prices when shorting is hard and overvaluation later unwinds. Disagreement classified as noise predicts nothing, and the popular aggregate measure actually points the wrong way because it is really just tracking sentiment (the two move together at 0.81).

Figure 2: Risk-adjusted monthly returns by disagreement type. Recreated from Figure 1 of the original paper.

Tellingly, the effect shows up right when earnings get announced and the arguing gets resolved, and it survives once you account for whether earnings actually surprised. The authors put it plainly, that investor disagreement “is not one thing.” For anyone using crowd sentiment or forum buzz as a signal, the lesson is that the crude aggregate can quietly reverse the sign of what you think you're measuring.

Yi, Kefu and Wu, Feng, What Investors Disagree About: LLM-Decomposed Retail Disagreement and the Cross-Section of Stock Returns. Available at SSRN: https://ssrn.com/abstract=7027983 or http://dx.doi.org/10.2139/ssrn.7027983

Instant Liquidity, Latent Risk: When Bond ETFs Break

Bond ETFs break not because investors flee, but because the plumbing that keeps their prices honest quietly seizes up.

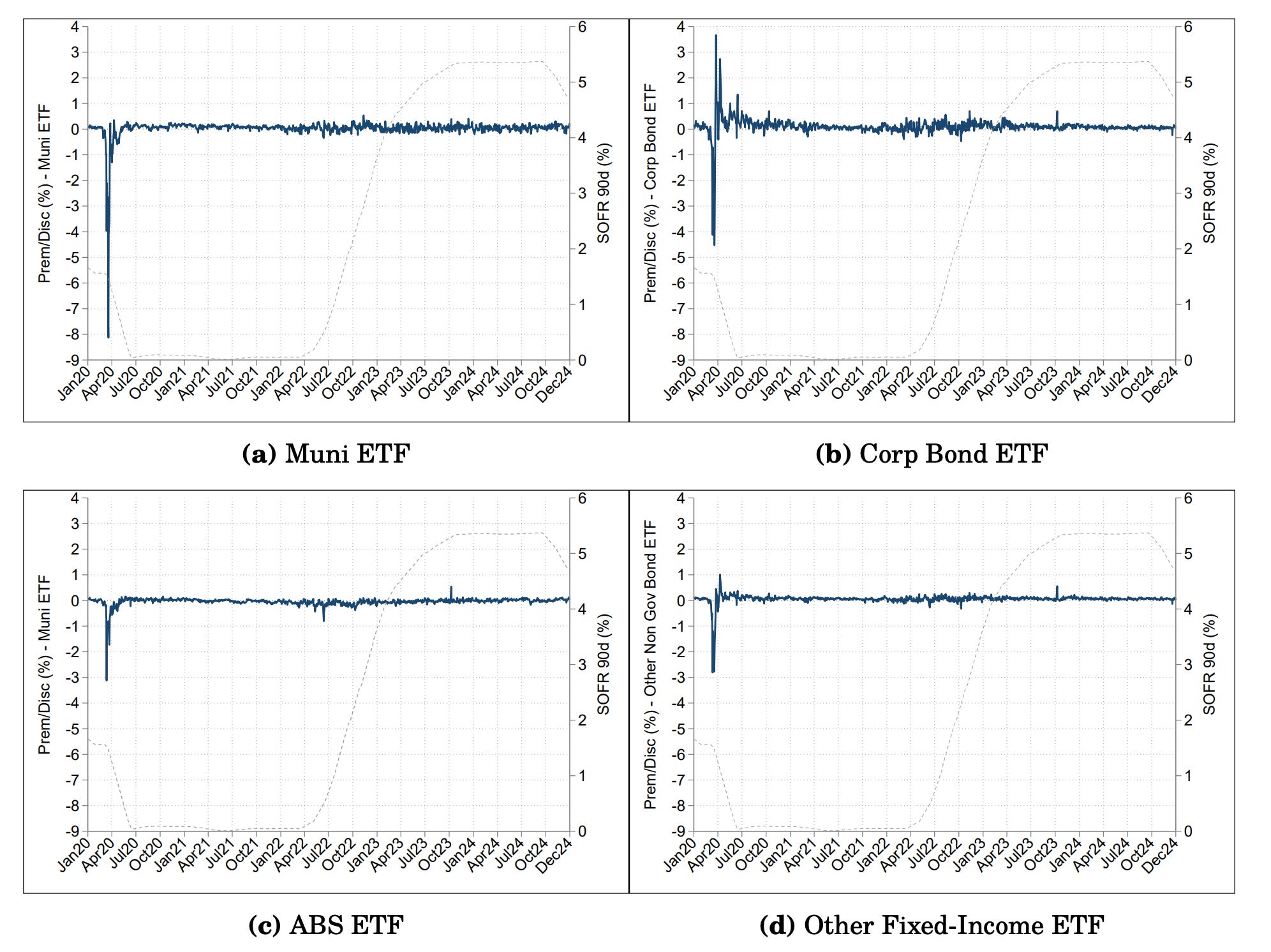

Melin and Rouxelin build a continuous-time model of two connected markets, a slow over-the-counter world where the actual bonds trade and a fast exchange where the ETF shares trade, linked by the authorized participants who shuttle assets between them.

The surprising result is that ETF fragility runs through prices, not redemptions. During March 2020, bond ETFs saw smaller outflows than mutual funds yet dislocated far more sharply from their net asset value, with the deepest discounts landing in the safer, more liquid segments rather than the riskiest ones. Their model explains this safety inversion, that when redemption baskets are costly for intermediaries to absorb, those middlemen demand a wider discount to play along, and once a single redemption looks doubtful, every share reprices as if none can be redeemed.

Figure 3: Premium or discount to NAV across four bond ETF categories, 2020 to 2024, with 90-day SOFR overlaid. Dislocations cluster in March 2020, deepest for municipals (near 8 percent), showing how stress hits some segments far harder than others.

For investors, the lesson is that a calm-looking ETF can mask a redemption mechanism that fails precisely when you need liquidity most, and those crisis discounts are structural signals, not free money.

Rouxelin, Florent and Melin, Lionel, Instant Liquidity, Latent Risk (July 01, 2026). Available at SSRN: https://ssrn.com/abstract=5304325 or http://dx.doi.org/10.2139/ssrn.5304325

The Enduring Influence of Openness on Risk-Taking

Cities forced open to foreign trade in 19th-century China still breed bolder investors today, 170 years later.

When the Qing dynasty was compelled to open a set of “Treaty Ports” to Western trade after 1842, those cities absorbed more than goods and factories. They picked up a taste for risk that never left. Lin and Tang trace this through three very different windows: commercial newspaper ads from 1850 to 1950 (Treaty Ports ran far more, especially in volatile industries like finance and real estate), state-controlled economic news from 1949 to 1988, and modern mutual fund accounts from Alipay.

The through-line is striking, because the formal institutions that created the advantage (foreign consulates, concessions, customs houses) were all dismantled after 1949, yet the behavior survived. Tellingly, the effect shows up only among long-rooted locals, not immigrants, pointing to culture passed down through families rather than current economics. For investors, it is a reminder that regional risk appetite is partly inherited, and that where money comes from can shape how boldly it gets deployed.

Lin, Tse-Chun and Tang, He, Enduring Influences of Openness on Risk-Taking Behaviors: Evidence from 170 Years of Ads, News, and Retail Investments. Available at SSRN: https://ssrn.com/abstract=7030024 or http://dx.doi.org/10.2139/ssrn.7030024

This week for paid subscribers

Paid subscribers are getting a look at whether tomorrow's stock direction is actually predictable, using a nonparametric sign-prediction rule that strips out the mechanical edge created by a stock's own upward drift before testing what real forecasting power remains. The post digs into why small-caps show a genuine 2.8 percentage point accuracy edge while large-caps mostly do not, why the drift adjustment quietly separates real signal from data artifact, and why mean-reverting names like a certain Arkansas community bank can turn a buy-and-hold loser into a tradable winner. Python backtest code included.

Disclaimer: The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.