Recent Academic Research

Algorithmic retail distortions, fiscal communication premiums, global attention saturation boundaries, and large language model predictive biases

Welcome back to another issue of Recent Academic Research!

Let’s get into it.

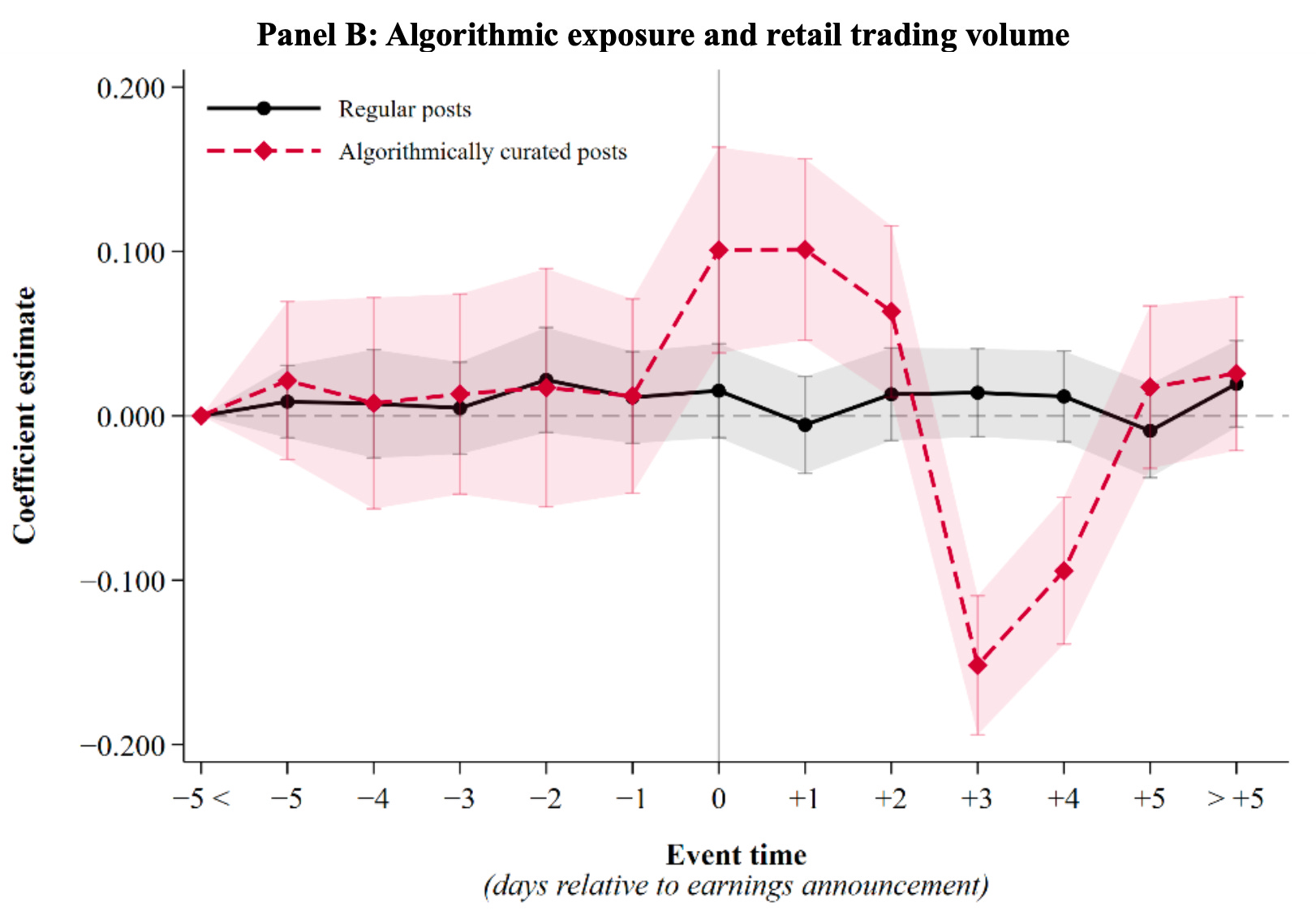

Social Media Is Quietly Costing Retail Investors

Financial recommendation algorithms on social media platforms systematically shift retail attention toward speculative, hype-driven stocks, inducing uninformed trading that ultimately reduces investor welfare and erodes market quality.

Digital platforms typically are not passive conduits of user opinions as they actively filter, rank, and personalize information to maximize user engagement opposed to content accuracy. By analyzing granular user feeds on StockTwits, this study demonstrates how algorithmic curation shapes investor behavior. When a platform algorithmically boosts specific contributors, it creates a localized attention shock. Investors predictably crowd into these promoted tickers, significantly boosting retail trading volumes while completely tuning out non-curated alternatives.

Crucially, this customized content appears to actively harm retail portfolios. As the paper warns, “investor behavior and market outcomes will reflect platform-level design choices,” meaning retail order flows become significantly less informed under heavy algorithmic exposure. Individuals are frequently lured into trading in the wrong direction, buying stocks right before they decline and selling right before they appreciate. This effect is particularly severe around chaotic earnings announcements when cognitive constraints are high.

For market participants, the takeaway is clear in that relying on customized social media feeds as an informational shorthand is an easy way to get trapped in short-term return reversals, proving that engagement-maximizing design choices carry substantial hidden economic costs.

Drake, Michael S. and Koenraadt, Jeroen and Thornock, Jacob and Twedt, Brady J., Social Media Algorithms as Information Intermediaries (May 07, 2026). Available at SSRN: https://ssrn.com/abstract=6731603 or http://dx.doi.org/10.2139/ssrn.6731603

The Real Cost of U.S. Fiscal Confusion

Erratic and confusing communication from the U.S. Treasury acts as a direct driver of sovereign bond market instability and inflation, with its economic penalty shifting radically depending on the nation’s debt burden.

Macroeconomic researchers traditionally treat Treasury press releases as mere political noise, but analyzing three decades of official communication reveals that institutional signaling has a powerful, tangible footprint on asset pricing. During periods of low inflation, policy confusion primarily acted as a real-economy drag, depressing industrial production as businesses paused hiring. However, in our current high-debt era, this transmission mechanism has fundamentally fractured. Treasury erraticism now bypasses the real economy entirely, transmitting directly into severe price inflation and violent shifts in the sovereign bond market.

When high-frequency messaging oscillates unpredictably, anxious bond investors instantly demand a premium to absorb long-term American debt, heavily distorting the long end of the yield curve. For investors, these findings are a wake-up call that the forward guidance paradigm is no longer the exclusive sandbox of the Federal Reserve. In a structurally leveraged economic regime, a chaotic fiscal authority compromises bond market liquidity and unanchors long-run inflation pricing, proving that “the forward guidance paradigm is no longer the exclusive domain of monetary policy.”

Guo, Yiting and Zhu, Zeju, The Price of Fiscal Confusion: Evidence from U.S. Treasury Communication. Available at SSRN: https://ssrn.com/abstract=6804466 or http://dx.doi.org/10.2139/ssrn.6804466

The Global Attention Saturation Threshold

When global investor attention concentrates past a critical threshold, the market mechanism abruptly switches from aggregating diverse private insights to synchronizing around a single public narrative, triggering severe liquidity drops and explosive systemic volatility.

Markets are highly efficient information processors until everyone starts looking at the exact same thing. This study uncovers a distinct behavioral boundary, known as the Attention Saturation Threshold, across 22 global equity indices. Below this point, standard linear asset pricing models work beautifully, but crossing it flips a switch.

Interestingly, as the authors observe, “the most dangerous regime transition arrives when standard indicators are quiet,” meaning the hours immediately preceding a breach are characterized by an eerie, suppressed calm as investors quietly abandon private data to anchor on a single shared storyline.

Once the threshold is breached, market makers face a highly synchronized, one-sided stampede of order flow. Fearing inventory risks, they swiftly pull back their quote depth, causing transaction costs to skyrocket and forcing returns to consolidate into a single global factor.

Balaji, Aditya and Goyani, Priyam and Malkan, Vevaan and Panchal, Aarnav and Balaji, Krishna, The Attention Saturation Threshold: A Real-Time Coordination Stress Monitor for Global Equity Markets. Available at SSRN: https://ssrn.com/abstract=6806933 or http://dx.doi.org/10.2139/ssrn.6806933

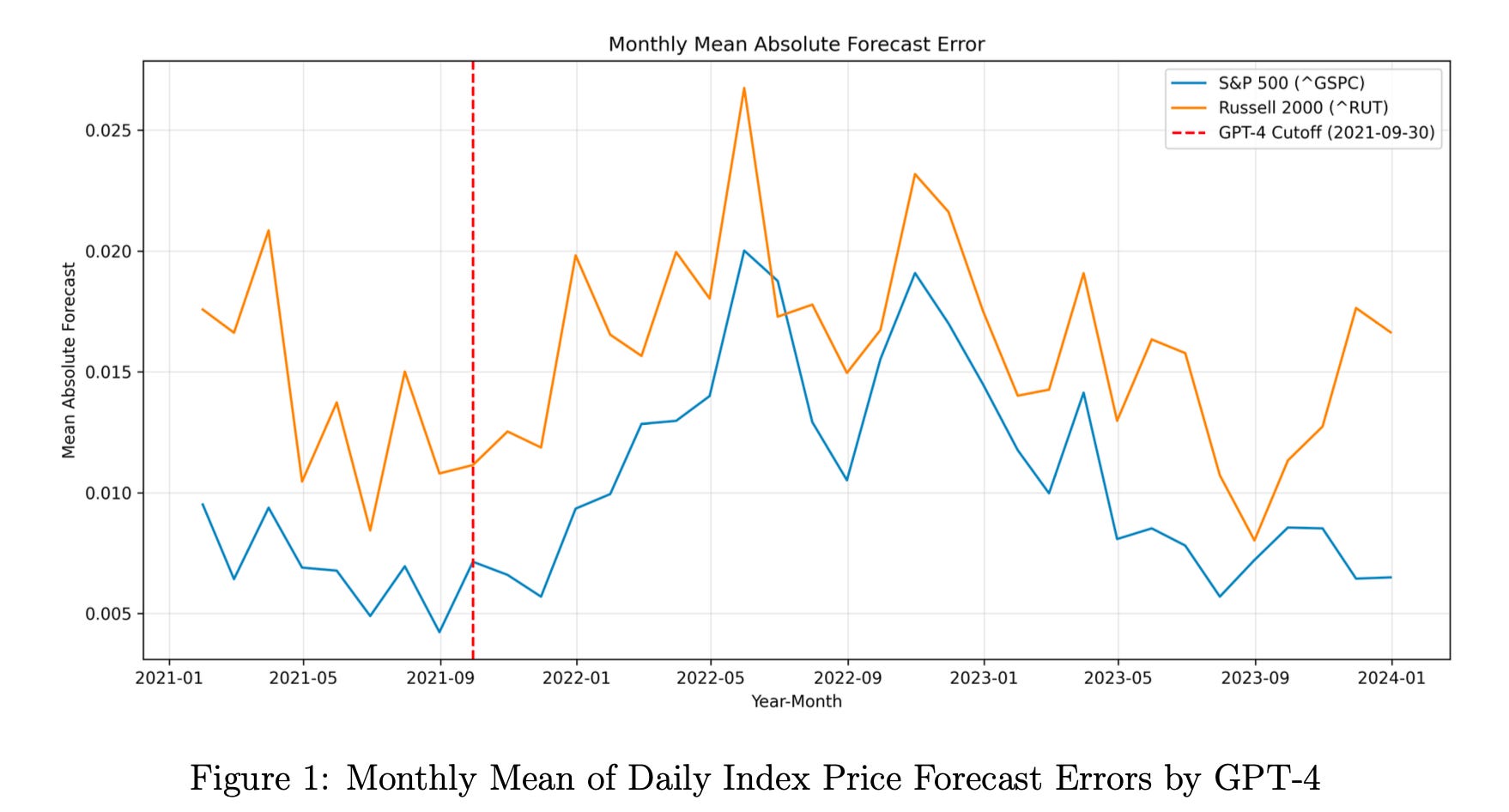

The Look-Ahead Trap in LLM Market Forecasts

Pretrained large language models exhibit a statistically and economically meaningful look-ahead bias in financial forecasting because their training data contains historical market outcomes, artificially inflating their pre-cutoff performance.

When evaluating how well artificial intelligence forecasts financial markets, it is easy to mistake a model's memory for actual predictive skill. By comparing predictions made before and after a major large language model's training cutoff date, this research uncovers a significant hidden advantage.

In the pre-cutoff window, the model's daily index forecast errors are roughly 18% lower, a performance boost that is heavily concentrated in the highly covered S&P 500. A similar patterns emerges for individual stock prices and quarterly earnings, proving that the network routinely supplements sparse prompt information with realized market facts embedded deep within its parameters.

Crucially, this look-ahead contamination drastically compresses the accuracy gap between the artificial intelligence and professional Wall Street analysts, particularly during highly volatile quarters when genuine forward-looking forecasting is at its absolute hardest. For investors and researchers, these findings matter because they show that checking an AI's performance using data from within its training window can be “misleading in the environments where accurate earnings expectations matter most.”

Liang, Chuan, Look-Ahead Bias in Financial Forecasts Generated by Large Language Models (September 01, 2024). Available at SSRN: https://ssrn.com/abstract=6772819 or http://dx.doi.org/10.2139/ssrn.6772819

This week for paid subscribers

Paid subscribers are getting a look into optimizing trade execution by dismantling the textbook U-shaped volume curve to eliminate slippage. This post explores the SPAR model to treat time-of-day periodicity as a fixed effect, benchmarks it against state-space models, and updates VWAP weights to slash tracking error. Python backtest code included.

Disclaimer: The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.

Paper three is the one with the widest implications. The attention saturation threshold formalises something traders have felt intuitively for years: the market processes diverse information efficiently until everyone starts watching the same thing, then it stops being a market and becomes a crowd. "The most dangerous regime transition arrives when standard indicators are quiet" maps directly onto the sandpile literature. the eerie calm before the threshold breach is the system loading energy into a single correlated position.

Paper two connects to this. Erratic Treasury communication acts as an attention synchroniser, forcing every bond investor to watch the same signal simultaneously. When high-debt fiscal policy becomes the single shared narrative that paper three describes, the yield curve becomes the sandpile. Both papers are really about the same phenomenon, the point where information diversity collapses into narrative monoculture and the market mechanism fails.