Recent Academic Research

Inflation coverage by news sources, prediction markets, bond ETF value around FOMC announcements, and the yield curve's implications on GDP growth

Welcome back to another issue of Recent Academic Research! After taking some time off, I will be resuming the weekly posts. Let me know if there’s any papers that you wish to see covered in the near future. Let’s get into it.

Inflation News and Expectations

More inflation coverage leads to higher inflation expectations.

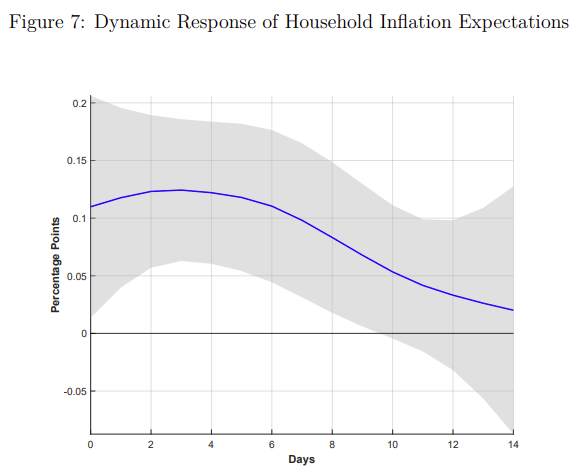

Households raise their inflation expectations when they see more media coverage of inflation, but only in response to inflationary surprises. The authors combine daily inflation expectation data with a novel instrument: the number of seconds that “inflation” is spoken on CNN, Fox, or MSNBC, using CPI release dates and surprises to isolate exogenous variation in coverage. A one standard deviation increase in news coverage (about 112 seconds) raises household expectations by around 0.12 percentage points at its peak, with effects fading after ten days.

The response follows a hump-shaped pattern, peaking four days after the news shock before gradually returning to baseline. Interestingly, only positive inflation surprises drive this effect. Negative surprises generate little to no reaction in expectations, even though media coverage also increases in those cases. This asymmetry appears to reflect how households interpret the news: when inflation is unexpectedly low, coverage may still signal concern, prompting conflicting interpretations.

The authors also show that Fox News disproportionately emphasizes positive surprises, and this contributes meaningfully to higher inflation expectations among Republican-leaning audiences. The analysis suggests that roughly 8 to 12 percent of the peak increase in inflation expectations in mid-2022 can be attributed to news coverage. In states that primarily watch Fox rather than CNN, this differential coverage accounts for about 14 percent of the partisan gap in expectations.

Binder, Carola and Frank, Pascal and Ryngaert, Jane, The Causal Effect of News on Inflation Expectations (August 2025). NBER Working Paper No. w34088, Available at SSRN: https://ssrn.com/abstract=5377995 or http://dx.doi.org/10.2139/ssrn.5377995

Arbitrage and Whales in Prediction Markets

Prediction markets aren’t always efficient, especially when arbitrage is blocked by real-world frictions.

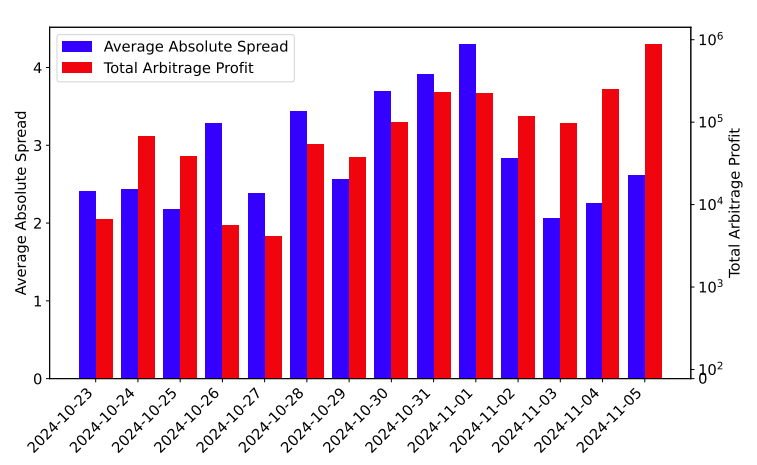

This paper investigates pricing discrepancies between Polymarket and Kalshi, two leading prediction markets, during the 2024 U.S. presidential election cycle. Despite trading on identical binary events, prices across the platforms often diverge significantly, creating persistent arbitrage opportunities. The authors show that these price gaps are not quickly eliminated by traders, largely due to institutional and regulatory barriers. Polymarket prohibits U.S. users, while Kalshi requires KYC and only supports USD deposits, making it difficult for traders to operate across both venues at scale.

The chart illustrates the relationship between average daily price gaps and total arbitrage profit across the two markets over a two-week period. Notably, high profit days tend to coincide with large absolute spreads, suggesting exploitable inefficiencies. However, these opportunities persist because traders face obstacles like transfer delays, capital constraints, and account limits.

Beyond arbitrage, the paper also analyzes whale trades (large, sudden shifts in market prices) and finds they are significantly more predictive of election outcomes than smaller trades. These large trades often come from a handful of well-capitalized accounts and consistently move prices in the correct direction.

Ng, Hunter and Peng, Lin and Tao, Yubo and Zhou, Dexin, Price Discovery and Trading in Prediction Markets (June 30, 2025). Available at SSRN: https://ssrn.com/abstract=5331995 or http://dx.doi.org/10.2139/ssrn.5331995

Mispricing of Bond ETFs

FOMC meetings can cause U.S. bond ETFs to trade significantly out of line with the value of their underlying securities.

This paper examines how U.S. fixed income ETFs, particularly those holding Treasuries and agency bonds, diverge from their net asset values (NAVs) around Federal Open Market Committee announcements. The authors document that on FOMC days, especially in the hours immediately after a statement is released, these ETFs trade at larger and more persistent premiums or discounts to NAV compared to normal days. This mispricing is not due to stale pricing or illiquid bonds but seems tied to heightened volatility, trading volume, and uncertainty in the Treasury market.

The figure shows that FOMC announcement days generate outsized NAV deviations in both directions, especially for ETFs holding less liquid securities. This divergence often begins within 30 minutes of the release and persists for several hours, peaking before returning toward normal levels. The paper also finds that mispricings are larger when uncertainty is high, such as during periods of elevated VIX or surprise Fed decisions. These results suggest that in times of intense monetary policy focus, bond ETFs may temporarily reflect sentiment and liquidity stress more than fundamental value, raising questions about price discovery and the ability of ETFs to serve as precise real-time indicators of the bond market.

Siregar, Dona and Hurwitz, Catalina and Farooq, Omar, The Mispricing of Bond Etfs in Relation to FOMC Announcements. Available at SSRN: https://ssrn.com/abstract=5385223 or http://dx.doi.org/10.2139/ssrn.5385223

Yield Curve and GDP Growth

The term premium drives the yield curve’s power to forecast GDP growth by influencing how banks manage risk and supply credit.

This paper examines why the slope of the yield curve predicts future economic activity and argues that the channel runs through banks’ exposure to interest rate risk. Specifically, when the term premium declines, the compensation banks earn for holding long-term assets relative to their short-term liabilities compresses, reducing their incentive to supply credit. The authors construct and estimate a structural model of bank behavior using detailed U.S. bank balance sheet data from 1997 to 2022. In the model, banks choose how much credit to supply, how much duration risk to bear, and how to manage capital in response to interest rate conditions.

The analysis shows that variation in the term premium, rather than expectations about short rates, explains the predictive power of the yield curve. When the term premium falls, banks with greater maturity mismatch reduce their lending more sharply, especially in longer-duration or riskier credit. These credit contractions then propagate into lower GDP growth. In counterfactual simulations where banks do not perform maturity transformation, the term premium loses its predictive content. The findings suggest that the slope of the yield curve forecasts the economy not because of what markets expect, but because of how banks react to changes in the term structure of interest rates.

Minoiu, Camelia and Schneider, Andres and Wei, Min, Why Does the Yield Curve Predict GDP Growth? The Role of Banks (July 09, 2025). Available at SSRN: https://ssrn.com/abstract=4493101 or http://dx.doi.org/10.2139/ssrn.4493101

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.

Welcome back! You were missed. Insightful work once again. Thank you.