Recent Academic Research

This week’s best academic research on the financial markets

Welcome back to another issue of Recent Academic Research! Let’s get into it.

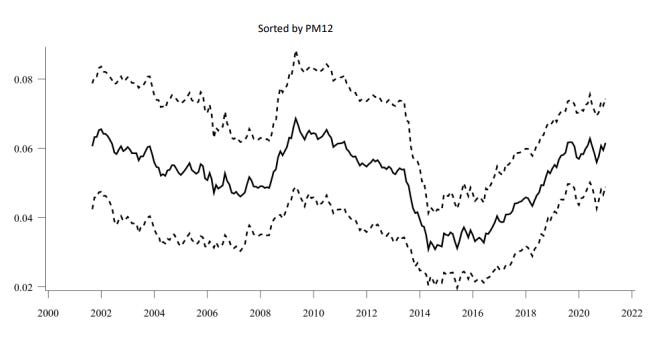

Option Momentum Among Peers

Can the failure of investors to pay attention to a competitor’s stock volatility unlock massive, risk-adjusted profits in the options market?

The stock market, already proven to exhibit powerful momentum effects, harbors another alpha source: peer option momentum. This strategy exploits the market’s tendency to underreact when a firm’s expected price swings (implied volatility) fail to fully incorporate volatility information stemming from economically linked companies (peers).

Researchers define these connections primarily through shared sell-side analysts, leveraging the idea that analysts often cover groups of firms with fundamental linkages. By tracking the past returns of option portfolios (specifically, delta-hedged straddles that hedge against stock movement) among these peer groups, an investor can reliably predict future options returns for the focal firm.

The predictive power is exceptional, with the benchmark strategy, which relies on a one-year formation period, yielding an annualized Sharpe ratio around 2.9, coupled with positive skewness and unexceptional tail risk. This peer effect remains robust even after controlling for traditional options momentum and other volatility predictors.

This mispricing is strongest when the focal firm receives low investor attention, notably those with low Google search volume, or when it has lower analyst coverage. This demonstrates a pervasive source of alpha that capitalizes on a persistent behavioral blind spot in market pricing.

Jones, Christopher S. and Khorram, Mehdi and Khorram, Mehdi and Li, Shuaiqi and Mo, Haitao and Yang, Lihai and Zhang, Yuanyi, Peer Option Momentum (September 02, 2025). Available at SSRN: https://ssrn.com/abstract=5542358 or http://dx.doi.org/10.2139/ssrn.5542358

The Dividend Capture Strategy

Is the decades-old trick of ‘dividend capture’ still profitable, or has the age of zero-commission trading finally arbitraged it away?

Dividend capture is a trading maneuver where an investor buys a stock immediately before its ex-dividend date, collects the payout, and then sells the shares, hoping the resulting price drop is less than the dividend amount.

Analyzing 35 years (1990–2025) of data on large-cap stocks, the study confirms that, on average, this strategy has remained viable for retail investors (who benefit from small trade sizes and tax-advantaged accounts). The mean expected return across the entire period was a positive 0.230% profit per dividend issuance using the minimal-risk “CloseOpen” trading approach (buying at close, selling at next day’s open).

However, market efficiency is rapidly closing this opportunity; the average profit plummeted to just 0.114% in the 2020–2025 zero-commission era, suggesting “this window of opportunity appears to be closing quickly”.

Certain sectors, including Finance, Consumer Discretionary, and Real Estate, consistently displayed significant positive effects on returns, possibly because their higher volatility dissuades more cautious investors.Despite the decay in profitability, retail investors still had access to an average of 241.5 unique opportunities annually in the most recent five years.

Ma, Kaden and Ma, Kaden, Dividend Capture Returns and Their Drivers: A Bayesian Analysis of Large-Cap Stocks Over 35 Years (August 20, 2025). Available at SSRN: https://ssrn.com/abstract=5473306 or http://dx.doi.org/10.2139/ssrn.5473306

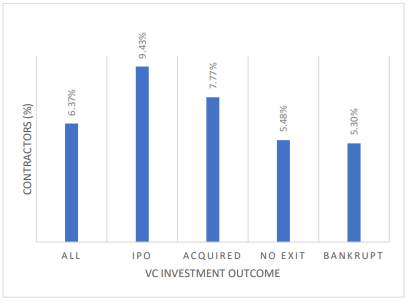

Systematic Venture Investing

Can getting Uncle Sam as a customer immediately boost a startup’s chances of hitting that coveted IPO jackpot?

Venture Capital (VC) firms invest in young companies inherently characterized by high uncertainty. This research shows that when a VC-backed company wins U.S. government contracts after receiving its investment, it acts as a powerful validation, significantly improving the outcome of that VC investment.

These contracts increase the probability of a successful IPO exit by 1.4 percentage points and an acquisition by 4.9 percentage points (relative to the sample mean), while reducing the likelihood of liquidation by 40%. These benefits accrue because government customers offer stability (lower demand uncertainty) and require stringent compliance, meaning that “government customers positively affect contractors’ operating performance and information quality”.

This highlights a new value-added role for VCs in guiding their portfolio companies through complex public sector sales.

Suleymanov, Masim and Cumming, Douglas J. and Javakhadze, David, Government Contracting and Venture Capital Exit Outcomes (April 04, 2025). Available at SSRN: https://ssrn.com/abstract=5530678 or http://dx.doi.org/10.2139/ssrn.5530678

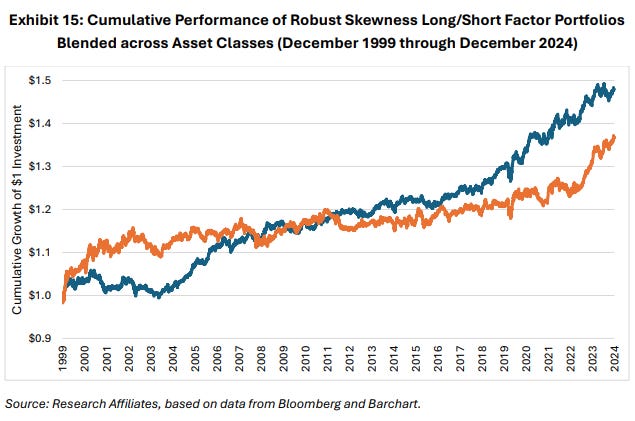

Profits through Selling Skew

Why are investors compensated handsomely for buying assets that are statistically wired for potential disaster?

Skewness fundamentally describes the asymmetry in an asset’s return distribution, revealing whether small, frequent moves are punctuated by rare, large outcomes, such as sudden market collapses (negative skewness) or massive, lottery-like gains (positive skewness).

This concept reflects deep investor behavior: humans detest the chance of abrupt, catastrophic losses, leading them to pay a premium (or essentially buy insurance) to hold assets with lottery characteristics. This enduring preference creates a powerful, persistent inefficiency called the total skewness risk premium, which rewards the contrarian who is willing to accept the risk of occasional blow-ups.

Analyzing a vast selection of investments, from multi-asset forwards to the entire equity factor zoo, researchers confirm that consistently buying negatively skewed assets and selling positively skewed assets delivers positive expected returns.

Suvak, Colin and Masturzo, Jim and Masturzo, Jim, A Tail of Five Skews (August 25, 2025). Available at SSRN: https://ssrn.com/abstract=5554621 or http://dx.doi.org/10.2139/ssrn.5554621

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.

options momentum has become a popular research topic.