Recent Academic Research

Company disclosures impact returns, portfolio weighting in trend following, prediction markets as an indicator for crypto volatility, and stock mispricings from regulations

Welcome back to another issue of Recent Academic Research!

Let’s get into it.

Company Disclosures and Returns

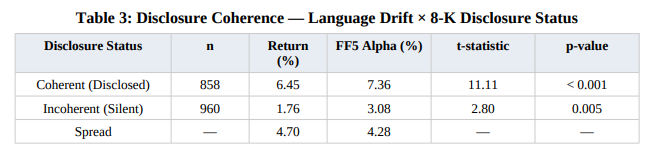

Subtle linguistic shifts in regulatory filings reliably predict future stock returns.

Researchers developed a disclosure drift signal that measures how much a company alters its vocabulary regarding risks and uncertainties from one regulatory document to the next. They discovered that these shifts in language consistently forecast abnormal equity returns over the following two months.

The predictive power becomes significantly stronger when a firm exhibits this linguistic drift while simultaneously releasing a formal explanation of material events. The authors call this phenomenon disclosure coherence. When a company changes its narrative but stays silent about the underlying reasons, the subsequent returns are considerably weaker.

This suggests that investors place a premium on transparent communication and that “the market effectively distinguishes between companies that transparently communicate evolving risks” to their shareholders.

Rigel, Sebastian, Disclosure Drift as a Predictive Signal for Equity Returns (April 01, 2026). Available at SSRN: https://ssrn.com/abstract=6444659 or http://dx.doi.org/10.2139/ssrn.6444659

Improved Trend Following

Trend following strategies generate substantially higher returns when investors optimize their risk exposure based on the current market environment.

Traditional trend following strategies operate on a simple binary rule of taking a maximum long position in rising markets and a maximum short position in falling markets. The author proposes a sophisticated new framework that calculates the exact optimal portfolio weight for any given market condition by maximizing the expected risk adjusted return.

This optimized approach reveals that taking a full short position during a bear market is almost always a mistake. Instead, the math dictates that investors should drastically reduce their exposure or sit in cash during severe downturns.

The dynamically optimized strategy comfortably beats both classic momentum models and newer adaptive models across United States and international equities. The author notes that “the performance gains are economically meaningful” and remarkably uniform across different markets.

Zakamulin, Valeriy, Rethinking Trend Following: Optimal Regime-Dependent Allocation (March 09, 2026). Available at SSRN: https://ssrn.com/abstract=6376479 or http://dx.doi.org/10.2139/ssrn.6376479

Prediction Markets and Crypto Volatility

Daily price changes in regulated macroeconomic prediction markets reliably forecast the future volatility of major cryptocurrencies.

Platforms like Kalshi allow participants to place binary bets on economic outcomes like Federal Reserve rate decisions or inflation data. The researchers discovered that the daily shifting probabilities in these event contracts are a leading indicator for cryptocurrency volatility.

Interestingly, different digital assets react to completely different macroeconomic channels. Bitcoin volatility is highly sensitive to shifting expectations about monetary policy, particularly during active rate cutting cycles. Conversely, smaller alternative tokens respond much more strongly to shifting inflation expectations.

The brilliance of this approach is that it provides a continuous daily read on macroeconomic uncertainty, unlike traditional economic data releases that only happen on fixed calendar dates. The authors conclude that these event contracts contain “information about future cryptocurrency realized volatility that is not captured” by conventional financial instruments.

Mohanty, Hardhik and Bhaskar Krishnamachari. “Do Prediction Markets Forecast Cryptocurrency Volatility? Evidence from Kalshi Macro Contracts.” (2026). https://arxiv.org/abs/2604.01431

Mispricing from Regulations

Statutory diversification rules force mutual funds to prematurely sell their winning mega cap stocks, which temporarily depresses the prices of these dominant companies and creates predictable buying opportunities.

United States tax laws require regulated investment companies to keep their largest individual stock positions below 5 percent of their total portfolio. As the broad stock market has become incredibly concentrated at the top in recent years, successful large cap growth funds are increasingly hitting this regulatory ceiling.

To remain legally compliant, these portfolio managers are forced to blindly trim their largest and most volatile holdings, completely regardless of their actual investment conviction. This mechanical forced selling exerts artificial downward pressure on the prices of these massive companies.

The researchers found that these specific equities go on to experience a significant rebound as the temporary underpricing eventually corrects itself. The authors note that “stocks held disproportionately in large positions by constrained funds earn abnormally high future returns” over the following months. This is a great example of how a structural inefficiency can create a lucrative mispricing anomaly in the largest and most liquid stocks in the world.

Lubos Pastor, Taisiya Sikorskaya, and Jinrui Wang, “The Hidden Cost of Stock Market Concentration: When Funds Hit Regulatory Limits,” NBER Working Paper 35007 (2026), https://doi.org/10.3386/w35007.

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.

The disclosure drift signal is a genuinely useful finding because it operationalizes something that experienced analysts do intuitively: read between the lines of regulatory filings for tone shifts that precede actual disclosures. The idea that subtle linguistic changes in 10-K and 10-Q filings predict future returns makes sense because management teams are constrained by legal disclosure obligations that force them to flag emerging risks earlier in language than they can explicitly acknowledge in investor communications. The prediction markets as a crypto volatility indicator is the research finding here that deserves the most attention from practitioners. If prediction market positioning on regulatory or macro events provides a leading signal on crypto volatility before it shows up in options implied vol, that is a tradeable edge that very few participants are likely exploiting systematically yet. The stock mispricings from regulations angle is also worth following closely given the current legislative environment in financial services and crypto, where regulatory overhang creates systematic discounting in entire categories of stocks that may be mispricing the probability of favorable outcomes.

Ai workflow is live

https://knowledge.dotadda.io