Recent Academic Research

The inevitability of stock market bubbles, news sentiment analysis with AI, risk factors in crypto, and a new narrative factor for equities

Welcome back to another issue of Recent Academic Research! Let’s get into it.

Inevitable Stock Market Bubbles

In simple growth models where production has decreasing returns to scale, stock price bubbles are not just possible but often inevitable when wage income and dividend income grow at different rates.

Financial bubbles are usually discussed as psychological phenomena or the result of market irrationality, but this research demonstrates that they can emerge as a necessity in perfectly rational economies.

The core driver is a mismatch in growth speeds: when total wages grow faster than corporate profits, the high demand for assets from workers pushes stock prices above their fundamental value. This happens most frequently when standard economic assumptions, specifically the Inada conditions for labor, are violated. Whether an economy is rapidly expanding or even steadily contracting, a bubble can form if dividends lag behind the broader income available for investment.

This suggests that the “fundamental value” of a stock might be a poor guide for price action in economies where capital and labor income are drifting apart. It highlights that market prices can remain “irrationally” high forever.

Sorger, Gerhard, Inevitability of stock price bubbles in simple growth models. Available at SSRN: https://ssrn.com/abstract=6661356 or http://dx.doi.org/10.2139/ssrn.6661356

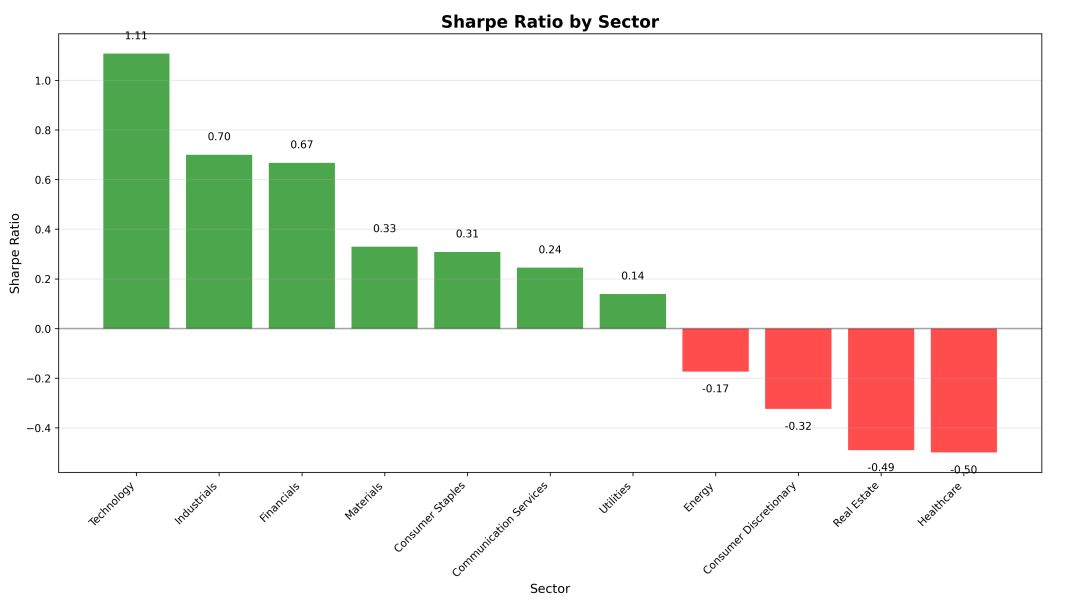

Sector Performance of News Sentiment

AI-driven sentiment analysis of news headlines can predict short-term stock price movements, but its effectiveness varies significantly by industry, with high-coverage sectors like technology showing the strongest risk-adjusted returns.

While the stock market is often moved by public sentiment, this research demonstrates that “news-driven tradability” is not uniform across all sectors.

By applying a logistic regression model to over 11,000 headlines, the author found that news sentiment acts as a reliable predictive signal primarily for sectors with heavy media coverage, such as technology and financials. In contrast, sectors like healthcare and real estate often exhibit negative Sharpe ratios when traded on news alone, likely due to sparse headlines and a higher ratio of market noise.

Interestingly, even in sectors with high trade volume, outperformance is not guaranteed; the study found that the quality and clarity of the sentiment signal matter more than the sheer number of articles.

This suggests that while AI can extract “alpha” from the media cycle, it is most effective when applied as a sector-specific tool rather than a blanket market strategy. “The sentiment signal is greatly affected by noise, but can still predict certain sectors.”

Prakash, Harshavardhan, Predicting U.S. Stock Sectors Using AI-Driven News Sentiment Analysis (April 26, 2026). Available at SSRN: https://ssrn.com/abstract=6653318 or http://dx.doi.org/10.2139/ssrn.6653318

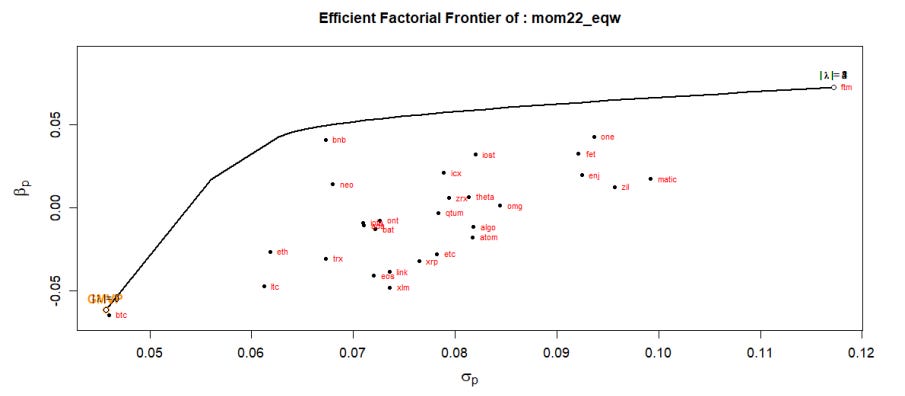

Crypto Risk Factors

Excess returns in the cryptocurrency market are driven by systematic risk factors beyond simple price trends, creating significant mispricing that “smart money” can exploit through disciplined factor tilting.

While the crypto market is often viewed as a lawless frontier of sentiment and speculation, this research identifies a clear underlying structure of systematic risks that dictate price movements.

By analyzing 29 major cryptocurrencies, the authors found that standard models like the CAPM fail to explain why coins with similar risk profiles deliver vastly different returns. Instead, return dispersion is driven by eight core factors, including global financial stress, DeFi risk-taking, and macroeconomic confidence. The study demonstrates that investors can harvest “alpha” by using a factor-tilting strategy, by essentially overweighting coins aligned with factors that are currently being rewarded, such as global volatility during market distress.

This approach moves beyond the “buy and hold” mentality, suggesting that the most efficient path to profits lies in navigating an “Efficient Factorial Frontier” where risks are actively managed rather than just accepted.

The authors summarize the potential of this disciplined approach by noting that “disciplined exposure to risk premia may offer a promising avenue in emotionally driven cryptomarkets”.

Jamhamed, Fayssal and Martin, Franck and Rondeau, Fabien and Thélissaint, Josué and Tufféry, Stéphane, On Risk Pricing and Arbitrage in the Cryptomarket: Anomalies and Factor Tilts (October 29, 2025). Available at SSRN: https://ssrn.com/abstract=6690098

The Narrative Factor

The “Narrative Factor” serves as a powerful cross-sectional return predictor that significantly outperforms traditional momentum strategies while maintaining a remarkably low correlation to established style factors.

Equity markets are often dictated by viral stories (from pandemic fears to AI booms), yet most systematic models remain anchored to backward-looking financial metrics. This research introduces a way to quantify these public discourse shifts by measuring how much a topic is being discussed and mapping that attention to specific company exposures.

The narrative factor produces risk-adjusted returns that are roughly three times stronger than a standard momentum strategy. Even when stripped of any overlap with common traits like value or quality, the signal remains a robust predictor of where prices are headed next. This suggests that public narratives are a quantifiable force that shapes market expectations before they fully reflect in stock prices.

As the author notes in the conclusion, “public discourse, systematically measured, contains meaningful cross-sectional pricing information not captured by traditional equity factors”.

Reese, Charlie, The Narrative Factor: A Systematic Approach to Capturing Narrative Alpha from Public Discourse (April 30, 2026). Available at SSRN: https://ssrn.com/abstract=6685058 or http://dx.doi.org/10.2139/ssrn.6685058

This week for paid subscribers

Our second paid post of the week focuses on examining the mean-reverting and trending properties of butterfly trades in the Treasury market.

Disclaimer: The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.