Recent Academic Research

Estimated impact on inflation from tariffs, aging populations and secular stagnation, and forecasting JOLTS data

Welcome back to another issue of Recent Academic Research! This week, I am highlighting a few more economic papers by the Federal Reserve.

This post is heavily focused on economic data and stagflation, which is relevant given current market events.

Let’s get into it.

Fed’s Tariff Impact Estimates

The authors assess the consumer price impacts of newly proposed U.S. tariffs using a novel dataset that links firm-level import records with household consumption data. By applying a first-order approximation framework, they estimate how tariffs on imports from China, Mexico, Canada, and the rest of the world could affect retail prices in the U.S. The analysis focuses on everyday retail goods like food, beverages, and general merchandise—about 25% of the total consumption basket. Compared to the 2018–2019 U.S.-China trade war, today’s tariff proposals are broader in scope, and the study considers both complete and partial pass-through of tariffs to consumer prices.

Findings:

Consumer prices on retail goods could rise by 0.81% to 1.63%, depending on whether firms pass on half or all of the tariff costs to consumers.

The most significant price effects come from tariffs on Canada and Mexico, which account for approximately 45% of the total projected increase due to their high trade volumes and the steep 25% tariff rate.

Additional tariffs on Chinese goods would add only about 8% to the total price effect, reflecting the reduced U.S. dependence on Chinese imports since 2018.

The rest of the world (excluding China, Canada, and Mexico) accounts for 47% of the projected increase under the full-tariff scenario.

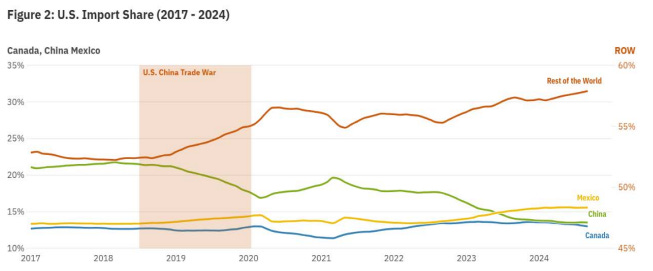

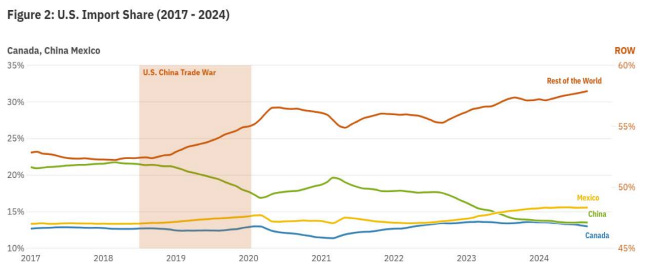

Import exposure has shifted notably—U.S. import share from China fell from over 20% in 2018 to under 15% in 2024, while Mexico’s share rose, as shown below

ROW: All countries from which the U.S. imports excluding China, Canada, and Mexico. Import shares are measured as the 12 month moving average of the total value of imports from a country divided by the total value of all imports in a given month. Source: U.S. Census Bureau (USA Trade Online), authors own calculations Consumer spending on firms importing from China also dropped by ~11% since 2018, largely driven by firms changing sourcing strategies rather than shifts in consumer preferences.

There is little evidence that recent inflation would significantly limit further price increases from tariffs; sectors with high import intensity have not experienced disproportionate inflation, suggesting room for price pass-through.

Because U.S. firms have diversified away from China but deepened ties with Mexico and others, the impact of new tariffs may be more widely distributed—and potentially more inflationary—than during the last trade war.

Baslandze, Salome and Fuchs, Simon and Pringle, KC and Sparks, Michael Dwight, Tariffs and Consumer Prices: Insights from Newly Matched Consumption-Trade Micro Data (February 01, 2025). FRB Atlanta Policy Hub Paper No. 2025-01, https://doi.org/10.29338/ph2025-01 , Available at SSRN: https://ssrn.com/abstract=5194582 or http://dx.doi.org/10.2139/ssrn.5194582

Effects of Aging Populations

In the years leading up to the COVID pandemic, many industrialized economies experienced a puzzling combination: low inflation, low real interest rates, and weak GDP growth—all despite aggressive fiscal and monetary stimulus. This paper argues that population aging is a key structural force behind this phenomenon. Using a dynamic model of household saving behavior and government policy, the authors explore how demographic shifts influence inflation and economic activity over time.

Findings:

Aging populations increase demand for savings, especially liquid assets like bank deposits, which drives down inflation and interest rates.

In Japan’s case, aging alone lowered the inflation rate by 1.1 percentage points, real interest rates by 2.0 points, and output by 3.1 percentage points over a 17-year horizon.

Aging reduces labor input as birth rates fall and older workers retire, which lowers output and productivity growth.

Older households save more but consume less, especially when real returns are low—amplifying secular stagnation effects.

Monetary easing can’t fully offset these trends: lower rates actually discourage consumption among older savers.

While the U.S. is aging more slowly than Europe or Asia, foreign capital inflows driven by aging abroad may still suppress U.S. inflation and interest rates.

Braun, R., Aging, Deflation, and Secular Stagnation (October 01, 2022). FRB Atlanta Policy Hub Paper No. 2022-13, https://doi.org/10.29338/ph2022-13 , Available at SSRN: https://ssrn.com/abstract=5191045 or http://dx.doi.org/10.2139/ssrn.5191045

JOLTS Job Data Forecasting

The authors aim to improve forecasts of U.S. labor demand, specifically the number of job openings reported in the JOLTS (Job Openings and Labor Turnover Survey), using machine learning models. Traditional econometric approaches often struggle with labor market data due to its complexity and noise. To address this, the paper builds a forecasting model that integrates a wide range of macroeconomic variables, including employment data, market indices, and leading indicators. They employ a Long Short-Term Memory (LSTM) neural network—a deep learning model well-suited for time-series forecasting due to its ability to capture long-range dependencies and nonlinear relationships. The model is trained on monthly data from January 2001 through August 2023.

Findings:

The LSTM model consistently outperforms a baseline AR(1) model in predicting job openings across various forecast horizons, from one to six months ahead.

LSTM predictions track actual JOLTS openings more closely during periods of labor market volatility, such as the COVID-19 shock and the 2022-2023 economic slowdown.

The performance edge of the LSTM model increases with longer forecasting horizons—suggesting it captures structural dynamics that simpler models miss.

A “top variables” analysis reveals that equity market indicators (e.g., S&P 500 returns) and consumer sentiment are highly influential in predicting job openings, alongside traditional labor metrics like initial jobless claims and payrolls.

The model remains robust even when some macro variables are excluded, indicating it is not overly dependent on any single input.

These results highlight the power of deep learning models to capture complex, nonlinear interactions in labor market data that are often missed by traditional approaches.

Kim, Kyungsu. "Forecasting Labor Demand: Predicting JOLT Job Openings using Deep Learning Model." arXiv preprint arXiv:2503.19048 (2025).

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.

On aging, I was expecting a paper with some econometrics attempting to measure aging effects directly. So I was a bit surprised that it was simply a qualitative story, a not implausible story mind you, but a story nonetheless. I was left wondering what would have happened had the author chosen an econometric route. I noted form the references and text that Cochrane's Fiscal Theory of the Price Level is not directly considered if at all as an explanation of how inflation evolves. In a simple economic growth model, output growth usually boils down to population growth plus the rate of factor augmentation. And in a super simple monetary model, inflation is simply monetary expansion less the rate of output growth. Simplistically then, aging would lead to inflation unless monetary policy adjusts. Exploring these connections would seem to require taking some measurements and looking for more complex mechanisms. This is not a criticism of your review but rather the lack of breadth and ambition of the original paper. This seems to me to be an area worth some serious research.

Has anyone really studied with a real anthropologist in Florida whether or not this is true - especially when the PERCEPTION of real returns is very high? Dr T is pretty much right. I can tell you having lived here in Florida. It is absolutely, without a shadow of a doubt, full stop, not true that old folks spend less money. Driving force of inflation right now involves the longer life expectancies from boomers associated with fat shots and government subsidized healthcare (e.g. no one wants to touch the "third rail" of Medicare and social security for existing recipients). All of that kicks in after you get old. Even if you have a job barely getting by, you can achieve significant wealth gains after 65 once you go on Social Security due to the pension like nature of the payments (e.g. you would be able to take on a new car loan because you knew the payment would cover it forever as opposed to never being able to take on debt if you had a very shaky job situation in retail at Home Depot). Look at the demographics for who is buying cars now and you see this effect. Combine that with continued sustained, voter approved tax cuts in these areas + migration to no tax red states from blue states and you don't peak with this rent-seeking behavior for a year or two longer due to demographics - then the tide goes out demographically.

"Older households save more but consume less, especially when real returns are low—amplifying secular stagnation effects."