Recent Academic Research

This week’s best academic research on financial markets

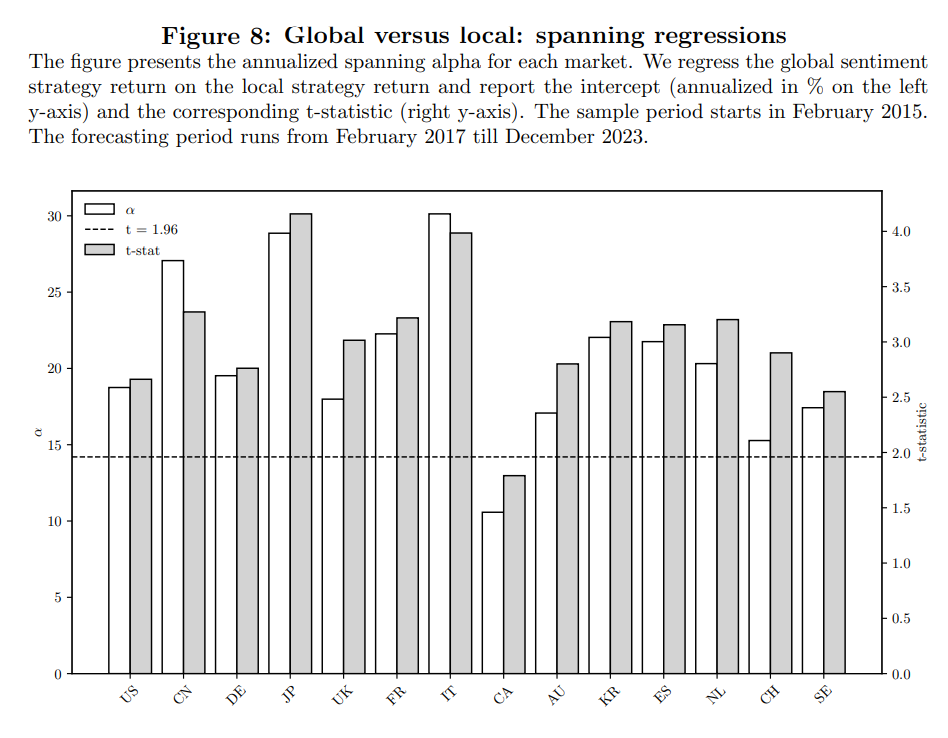

Global News and Equity Returns

Global news sentiment forms an information network that predicts next day equity returns and adds information that local news alone misses.

This paper explores how news-based sentiment impacts international stock market returns, using a vast collection of global news articles. The authors analyzed over 520 million articles from 14 developed countries to create detailed sentiment measures, showing how media in one country reports on another across many topics. Using advanced machine learning, they developed strategies to predict market movements based on both local and global sentiment. The study reveals that a country's own local news sentiment is a strong predictor of its stock market returns, often outperforming basic investment strategies and reducing risk.

Additionally, global sentiment (news flowing between countries) provides unique and valuable insights that significantly improve market predictions beyond just local news. The research maps a global news network, identifying the United States as a central hub with widespread influence on global markets, alongside other key regional players. This demonstrates how international stock markets are connected through shared news and sentiment.

Freire, Gustavo and Moin, Ali and Moin, Ali and Quaini, Alberto and Soebhag, Amar, Global News Networks and Return Predictability (August 30, 2025). Available at SSRN: https://ssrn.com/abstract=5421496 or http://dx.doi.org/10.2139/ssrn.5421496

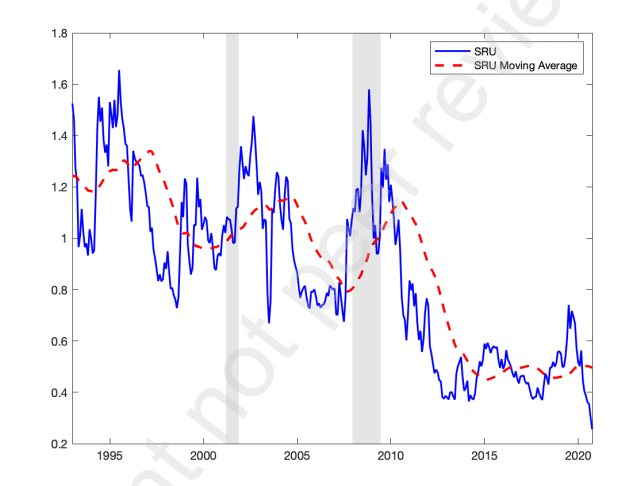

Cyclicality of Short Rate Uncertainty

Short-rate uncertainty’s cyclical swings predict the stock market, and the effect runs through cash flows.

This paper establishes that a specific type of market-based short-term interest rate uncertainty (SRU) can reliably predict overall stock market returns. The key finding is that only the cyclical component of SRU (SRU(c)) has predictive power, while its slow-moving, long-term trend component (SRU(s)) does not (shown below).

SRU(c) captures quick changes related to economic news or policy shifts. The study shows that higher SRU(c) predicts lower future stock returns, as increased uncertainty often leads to higher borrowing costs and reduced investment. In practical terms, SRU(c) significantly outperforms other common predictors in real-time forecasting, achieving an out-of-sample R2 of up to 14.22% and offering substantial economic benefits for investors by enhancing utility gains and Sharpe ratios. The paper also suggests that SRU(c)'s predictive power primarily comes from its ability to forecast future cash flows rather than discount rates.

Yu, Deshui and Huang, Difang and Yin, Ximing, Market-Based Short-Rate Uncertainty and Time-Varying Expected Returns. Available at SSRN: https://ssrn.com/abstract=5421037 or http://dx.doi.org/10.2139/ssrn.5421037

Currency Demand and Crises

Crises cause a flight to “safe-haven” currencies, however the type of crises affects which currencies are demanded.

This paper explores how global institutional investors shift their money between "safe-haven" currencies and "funding" currencies (used in carry trades) during times of market stress. By analyzing actual currency and bond flows from a major bank, the study distinguishes between different types of financial crises.

It finds that during broad economic crises, like the 2008 Global Financial Crisis or the COVID-19 pandemic, investors tend to pour money into the U.S. Dollar (USD), seeing it as a reliable safe haven. However, in situations where carry trades (borrowing in low-interest currencies to invest in high-interest ones) unwind, such as the 2024 "carry crash" or "Liberation Day" in 2025, currencies like the Japanese Yen (JPY) and Swiss Franc (CHF) receive significant inflows.

The research highlights that the USD maintains its safe-haven appeal even when its interest rates are higher than other funding currencies, proving these roles are distinct and important for understanding global currency movements.

Cheema-Fox, Alexander and Cuipa III, Edward S. and Greenwood, Robin M., Flight to Safety or Flight from Carry? (August 13, 2025). Available at SSRN: https://ssrn.com/abstract=5410363 or http://dx.doi.org/10.2139/ssrn.5410363

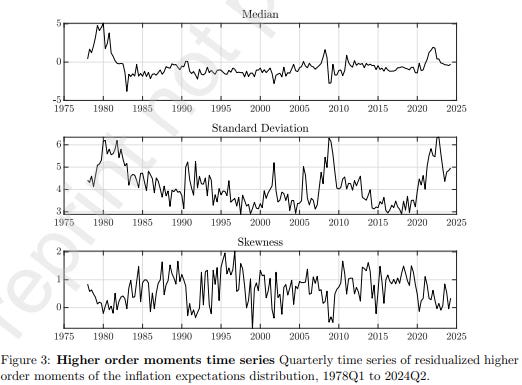

Distribution of Inflation Expectations

While median inflation expectations can affect future inflation rates, the distribution itself also plays a role.

This paper investigates how the entire range of inflation expectations, not just the average, influences actual inflation rates. Using a specialized statistical model, the study shows that a sudden increase in the typical (median) inflation expectation can raise the overall inflation rate for up to three years. More significantly, these shocks create a persistent risk of much higher inflation that can last for over six years, particularly affecting the upper extremes of the inflation distribution.

The research also examines how disagreements among people about future inflation, measured by the spread (standard deviation) and shape (skewness) of their expectations, impact real inflation. Increased disagreement leads to greater risks of high inflation, while a specific shift in the shape of expectations can temporarily push inflation rates higher. The key takeaway is that understanding the full distribution of inflation expectations is crucial for policymakers to maintain stable prices.

Barrales-Ruiz, Jose and Islam, Azharul and Mohammed, Mikidadu and Panovska, Irina, From Beliefs to Prices: Analyzing How Inflation Expectations Affect the Inflation Distribution. Available at SSRN: https://ssrn.com/abstract=5428432 or http://dx.doi.org/10.2139/ssrn.5428432

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.