Recent Academic Research

The most interesting academic research on the financial markets over the past week

Welcome back to another issue of Recent Academic Research! Let’s get into it.

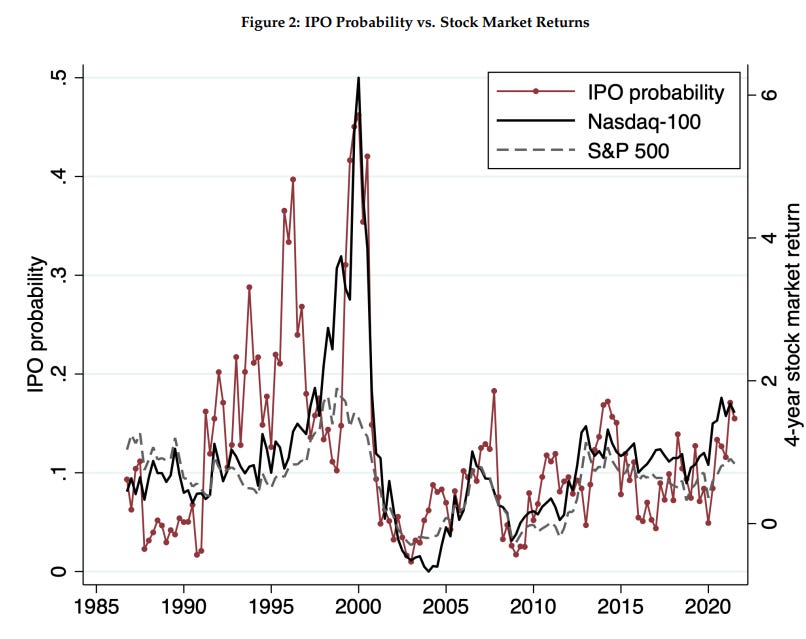

Replicating VC Returns

What if a diversified VC portfolio behaves like a levered tech index?

Using a compound-option model for staged startup financing, the authors show that VC payoffs move with the Nasdaq-100 and that a simple levered Nasdaq position can closely track vintage-level VC returns.

A large majority of VC-backed IPOs list on Nasdaq, which makes Nasdaq the relevant market exposure for exits, not the broad market. Newly public VC-backed firms exhibit high volatility and a Nasdaq beta around 1.4, which anchors the model’s stage-specific betas and the replicating strategy. The model, calibrated only to unconditional liquidation and IPO rates, still captures rich conditional dynamics: it explains about 39 percent of the variation in quarterly IPO activity and 92 percent of the variation in vintage returns.

Implementing the replication is straightforward: scale Nasdaq-100 exposure by the model’s stage betas and roll exposure as the portfolio matures. This levered-NDX benchmark matches vintage returns closely and reveals a stark pattern, with pre-2000 vintages roughly keeping pace and all post-2000 vintages lagging the benchmark. As the authors put it, “VC returns are largely explained by market-driven optionality and concentrated Nasdaq exposure.”

Hillenbrand, Sebastian and Stafford, Erik, Venture Capital as Portfolios of Compound Options (August 12, 2025). Available at SSRN: https://ssrn.com/abstract=5388676 or http://dx.doi.org/10.2139/ssrn.5388676

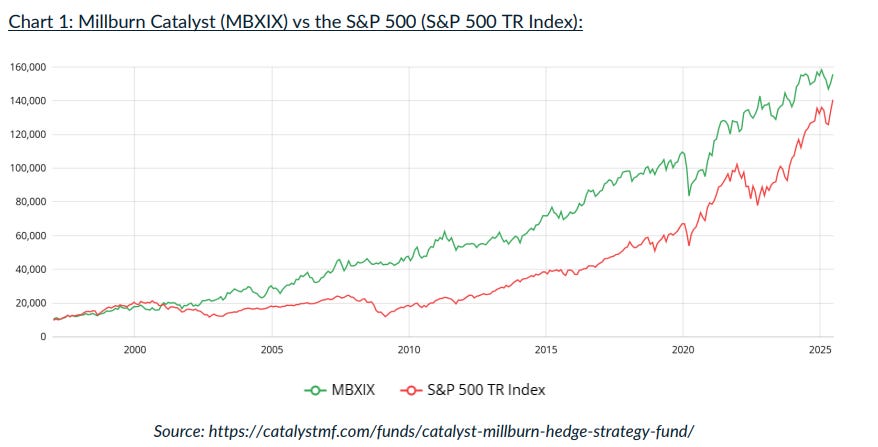

The History of Return Stacking

Can you keep core equity exposure and still add a diversifier on top?

The authors argue yes. They frame return stacking as the practical, investor friendly evolution of portable alpha, where investors hold full market exposure and overlay a second, low correlation return stream such as a CTA.

The paper mixes history with live examples. It highlights PIMCO StocksPLUS as a long running blueprint, with the PSLDX fund compounding 12.38 percent a year from August 2007 to May 2025 versus 10.34 percent for the S&P 500 total return over the same window. It also reviews the Catalyst Millburn fund and notes that equity selloffs were often shallower for the overlay, including a smaller pullback year to date through June 2025.

The guide then shows how stacking can be implemented with public building blocks using futures or capital efficient funds, and why conditional correlations matter more than long run averages. The simplest illustration is an equity index plus a trend following CTA, each targeted at 100 percent exposure and rebalanced quarterly. The figure below shows the stacked mix versus the standalone equity index from 2000 to mid 2025 and why the combined profile can raise return while smoothing the ride.

The authors stress the usual trade offs around leverage, style concentration, and funding choices. “Return stacking represents a powerful evolution in portfolio construction.” Their bottom line is careful and practical, especially after the choppy trends of 2025.

Basnicki, Brennan and Pickering, Tim, Return Stacking and Portable Alpha, an Investor's Guide (August 07, 2025). Available at SSRN: https://ssrn.com/abstract=5382795 or http://dx.doi.org/10.2139/ssrn.5382795

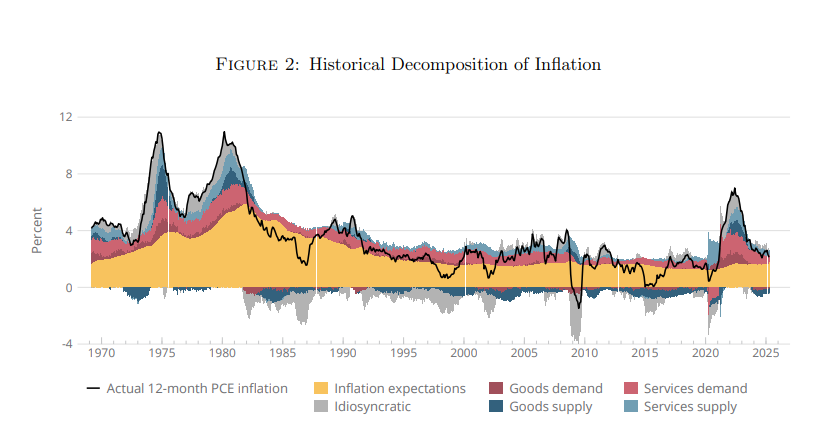

Inflation Factors and Forecasting

Splitting inflation into goods versus services and supply versus demand helps explain the pandemic surge and the swift disinflation, and it improves medium-term forecasts.

The authors build a sign restricted dynamic factor model that uses prices and quantities from PCE categories to extract common supply and demand factors for goods and services, plus an expectations and an idiosyncratic component.

Distinguishing goods from services matters. During early 2020, common demand and supply collapsed and roughly offset each other; by mid 2020, demand driven inflation picked up, and in 2021-2022, supply constraints reappeared, especially in services.

When added to a standard BVAR, these factors would have warned in December 2020 about a rapid and persistent inflation surge and then captured the mid 2022 disinflation that surprised many observers. Forecast accuracy improves by about 20 percent at horizons of six to twenty four months for both total and core PCE inflation. As the authors note, “the Federal Reserve’s initial characterization of that inflation episode as ‘transitory’ proved too optimistic.”

Leiva-León, Danilo and Sheremirov, Viacheslav and Tang, Jenny and Zakrajšek, Egon, Inflation Factors (August, 2025). FRB of Boston Working Paper No. 25-5, Available at SSRN: https://ssrn.com/abstract=5396820 or http://dx.doi.org/10.29412/res.wp.2025.05

Dividends as Recessionary Stimulus

Stable dividends look like small premia in good times and a cash payout when recessions hit.

Using portfolio holdings from Thomson Reuters Global Ownership Holdings, the study shows many institutional investors prefer dividend payers yet rebalance only gradually after increases, which helps keep dividends sticky and bolsters consumption when growth stalls. An intermediary asset pricing model calibrated to these slow-moving preferences closely matches aggregate payout behavior and persistence, and it is particularly strong around recessions.

The key mechanism is muted investor response to payout changes, which lowers firms’ incentive to adjust and encourages stability. The paper then quantifies the macro bite: keeping dividends smooth looks like paying a small ongoing premium, but at the start of a recession aggregate payouts rise meaningfully, supporting spending.

In the estimates, the recession lift is about ten percent of quarterly payouts, roughly fifteen billion dollars in 2023. As the conclusion puts it, “smoothing dividends may take the form of a simple insurance contract.” And “during recessions, the insurance contract pays out.” This is a calibrated U.S. model and does not directly account for retained earnings or capital gains, so totals are illustrative rather than comprehensive.

Douglas, Reed, The Role of Sticky Dividends During Recessions (August 21, 2025). Office of Financial Research Working Paper No. 25-04, Available at SSRN: https://ssrn.com/abstract=5400499 or http://dx.doi.org/10.2139/ssrn.5400499

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.