Recent Academic Research

The predictability of Treasury returns from debt cycles, the contrarian signal of magazine covers, the instability of US market weighting, and the detection of rational bubbles.

Welcome back to another issue of Recent Academic Research! Let’s get into it.

Magazine Cover Indicator

When a financial trend finally appears on a magazine cover, the market move is usually over.

Investors often suspect that mainstream magazine covers signal the end of a trend. This study tests that theory by analyzing covers from The Economist and Time to see if they serve as reliable contrarian signals. The results confirm that magazine covers work as a strong reverse indicator, especially when the cover story is bearish.

The authors identified magazine covers as bullish or bearish for specific asset classes, and then tested the forward returns after the magazine was published. We would expect bullish (bearish) covers to have negative (positive) future returns, given the contrarian hypothesis.

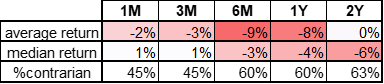

Bullish Magazine Covers (23 covers)

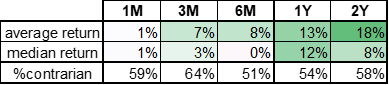

Bearish Magazine Covers (39 covers)

The data shows that asset prices typically reverse direction shortly after publication, and the signal strengthens over the following year. This happens because a cover story represents “peak social mood” and narrative exhaustion.

National Debt and Treasury Returns

The national debt ratio fails to predict market returns until you separate the long-term trend from the short-term cycle.

Fiscal theory suggests that a high Debt-to-GDP ratio should predict future surpluses or lower bond returns, yet the raw data rarely supports this. The authors resolve this issue by splitting the ratio into two components to separate the slow long-term trend from the faster local cycle. They find that the slow trend hides predictive signals, while the local component accurately forecasts Treasury returns.

The study shows that this local component offers “substantially improved out-of-sample forecast gains” compared to historical averages. This distinction matters because it shifts the focus from total debt levels to cyclical deviations. Bond traders can find a genuine edge by tracking these local cycles rather than waiting for absolute debt levels to force a market correction.

Zhou, Mingtao and Yu, Deshui and Chen, Li, Mean-Reversions in the Debt-to-GDP Ratio and Predictability of Treasury Debt Returns and Surpluses. Available at SSRN: https://ssrn.com/abstract=5852459 or http://dx.doi.org/10.2139/ssrn.5852459

Bubble Detection

Market bubbles can form when rational agents aggressively switch strategies to chase extraneous signals.

Economists struggle to define bubbles, but this paper models them as a competition between fundamental investors and those chasing trends. The authors use evolutionary game theory to show that investors switching strategies based on recent performance can create price explosions.

They confirm that the Generalized Sup Augmented Dickey-Fuller test effectively detects these episodes in real time. The model indicates that bubbles persist only as long as enough “reflectivist” investors remain to support the trend.

This matters because it suggests bubbles are not necessarily irrational but rather the result of traders rationally chasing short-term performance.

Waters, George, Detecting Mysticism in Asset Markets. Available at SSRN: https://ssrn.com/abstract=5896615 or http://dx.doi.org/10.2139/ssrn.5896615

A Pitch Against U.S. Equities

Allocating sixty percent of a global portfolio to US stocks relies on a model that breaks down under slight uncertainty.

This is the part 2 of a paper I highlighted last week, which takes the other point of view. Global market capitalization suggests investors should hold roughly sixty percent of their equity portfolio in US stocks.

This paper challenges that standard by showing that mean-variance optimization is highly sensitive to small errors when assets are correlated. When the authors introduce minor uncertainty into return forecasts, the model’s optimal allocation to the US drops significantly.

If the authors use methods that do not rely on return forecasts, the optimal portfolio shifts toward an equal weight across regions. This implies that the standard heavy allocation to American equities is a bet on perfect forecasting rather than a mathematical requirement for diversification.

Battistella, Arnaud and McLoughlin, Nicholas, How much is too much? Part 2: Why 60% in US equities might be just as crazy as it sounds (November 28, 2025). Available at SSRN: https://ssrn.com/abstract=5841007 or http://dx.doi.org/10.2139/ssrn.5841007

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.