Recent Academic Research

Momentum in REIT markets, a simple recession forecasting model, ML credit risk models, and the robustness of covered call strategies

Welcome back to another issue of Recent Academic Research! Let’s get into it.

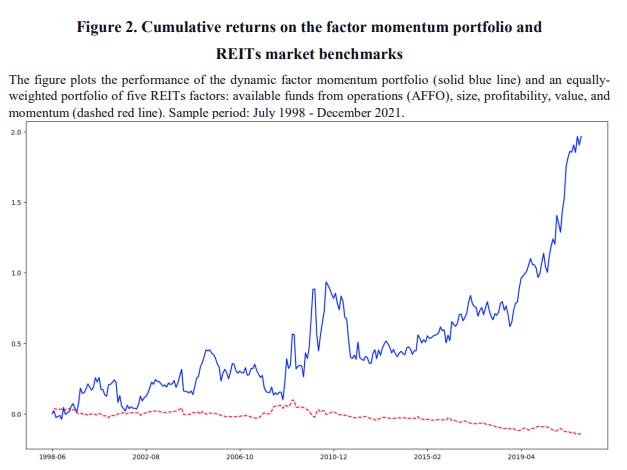

Momentum in REITs

What happens when you apply popular factor strategies like momentum and value to the REIT market? It turns out, not much... until you start timing the factors themselves.

Investors who apply standard equity factor strategies to the Real Estate Index Trust (REIT) market are often disappointed. This study confirms why, finding that traditional factors like momentum, value, and size failed to generate systematic positive alpha in the US REIT market from 1998-2021. In fact, a diversified multifactor portfolio actually lost money on average. The data shows REIT factors behave differently than stock factors, spending nearly 70% of the time in ‘bear’ or ‘rebound’ phases.

But the researchers uncovered a powerful alternative: while the factors themselves underperformed, there was strong momentum in the factors. They created a dynamic “factor momentum” strategy that buys the two best-performing factors from the past year and shorts the two worst, rebalancing monthly.

This strategy-of-strategies worked, generating a significant annualized alpha of about 6%. This approach was particularly effective during market downturns, suggesting it may offer valuable “safe-haven” properties for a diversified portfolio.

Dobrynskaya, Victoria and Tomtosov, Aleksandr and Rechmedina, Svetlana, Momentum Factor or Factor Momentum in REIT Market? (October 10, 2025). Available at SSRN: https://ssrn.com/abstract=5631072 or http://dx.doi.org/10.2139/ssrn.5631072

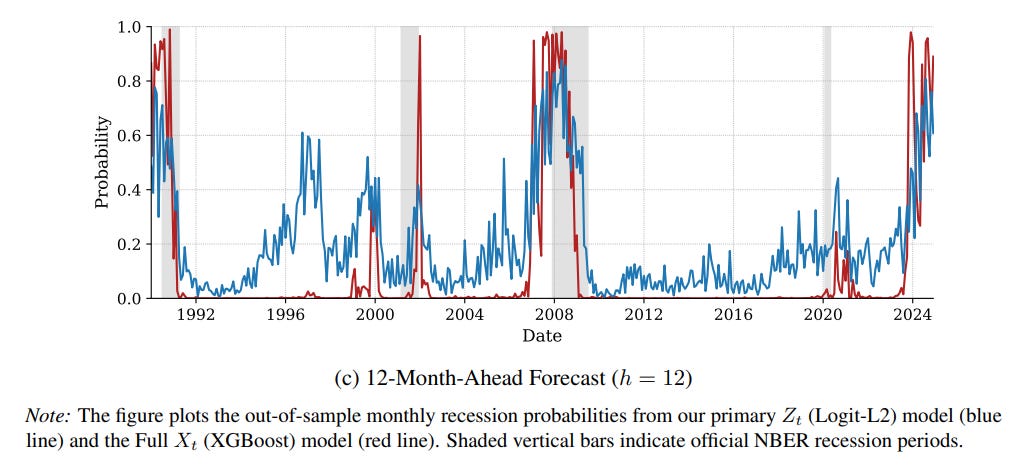

Forecasting Recessions

When forecasting recessions, transforming complex economic data into simple binary “at-risk” signals makes linear models surprisingly competitive with advanced machine learning.

Forecasting recessions is a notoriously difficult challenge, and the standard approach involves feeding complex models with continuous data. This paper tests a radically simpler idea: what if the only thing that matters is whether an indicator has crossed into “unusually weak” territory?. The authors propose an “at-risk” transformation, converting each predictor into a simple binary (Yes/No) signal based on its historical distribution.

In out-of-sample tests, a basic logistic regression model fed these binary signals, rather than the raw data, consistently improved forecasting performance.

In fact, this simplified linear model often proved superior to, or highly competitive with, more complex non-linear classifiers like XGBoost. This suggests that for rare events like recessions, the most important information is captured by the signal (crossing a threshold), not necessarily the model’s complexity.

Billakanti, Rahul and Billakanti, Rahul and Shin, Minchul, At-Risk Transformation for U.S. Recession Prediction (October, 2025). FRB of Philadelphia Working Paper No. 25-34, Available at SSRN: https://ssrn.com/abstract=5684442 or http://dx.doi.org/10.21799/frbp.wp.2025.34

Credit Risk Models

In emerging markets with sparse financial data, new machine learning models are proving significantly better at predicting credit risk than traditional methods.

Traditional credit scoring models, like logistic regression, often perform poorly when trying to assess risk in emerging markets. The core challenge is a lack of reliable, structured financial data and credit histories. This paper investigates whether modern machine learning (ML) models, such as Random Forest and XGBoost, can do a better job. Using a dataset of small and medium-sized enterprises, the authors found that ML models “significantly outperform conventional approaches”.

The key to their success lies in their ability to handle complex, non-linear relationships and to incorporate “alternative data” sources. Instead of just using balance sheets, these models can learn from utility bills, mobile payment records, and cash-flow ratios to build a more accurate picture of creditworthiness.

Ali, Osaf and Ali, Osaf, Machine Learning Models for Credit Risk Assessment in Emerging Markets (October 06, 2025). Available at SSRN: https://ssrn.com/abstract=5570578 or http://dx.doi.org/10.2139/ssrn.5570578

Covered Calls

Do Covered Calls Deliver Superior Returns?

Nam Nguyen shared an interesting paper a few weeks ago that I wanted to highlight.

The study evaluates the performance of a covered call strategy relative to the SPY ETF benchmark over the period from July 2009 to April 2023. Three covered call variations are analyzed: at-the-money (ATM), two percent out-of-the-money (OTM), and five percent OTM call options. The results show no statistically significant difference between the covered call strategies and the benchmark in terms of overall performance.

Among the tested strategies, the five percent OTM covered call achieved the highest annualized return of 16%, followed by the two percent OTM with 15%, compared to SPY’s 13%. The findings suggest that while covered call strategies may offer comparable or slightly better returns in some conditions, their advantage is not statistically robust.

Overall, the study highlights the limited evidence supporting the superiority of covered call strategies over a simple buy-and-hold approach for ETFs.

Tomáš Ježo, Effect of covered calls on portfolio performance, 2023, Charles University

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.

My vote is for forecasting recessions.

Covered calls are also a very interesting topic; it's a pity that the dataset is limited to 2023. I think if we re-run the research with recent data, buy-and-hold will crush covered calls, but it's only my speculation.

For me it would be “Momentum in REITs”