Recent Academic Research

The power of earnings call narratives, ML gold-silver pair trading, passive fund-driven turn-of-the-month corporate bond demand, and the forward shift in housing market seasonality.

Welcome back to another issue of Recent Academic Research! Let’s get into it.

Turn-Of-Month Anomaly in Corporate Bonds

What if all your corporate bond returns for the entire month happened during a single week?

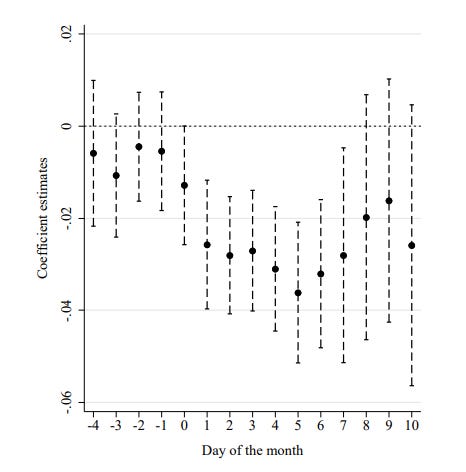

While traditional finance theory dictates that predictable seasonal patterns should be quickly arbitraged away, the corporate bond market harbors a glaring exception: nearly all of the credit premium for investment-grade bonds is earned in a tight, ten-day window around the turn of the month.

Specifically, yield spreads compress by about four basis points as the previous month ends and the new one begins. A portfolio that only holds bonds during this turn-of-the-month period captures the entire credit premium relative to Treasuries, while holding them during the rest of the month earns near-zero excess returns.

This anomaly is not driven by information releases or retirement contributions, but by institutional flows: the monthly bond mutual fund reinvestment cycle. Index-tracking passive funds are incentivized to concentrate the reinvestment of their cash flows (coupons and maturing bonds) at the month-end to avoid tracking error against their benchmarks. The effect is predominantly driven by these passive funds, reflecting the more rigid tracking error constraints faced by passive funds.

I have highlighted this anomaly in other markets before, including equities and Treasury markets. It is fascinating to see how robust this anomaly is across asset classes.

Sialm, Clemens and Shin, Sean Seunghun and Zhu, Qifei, Recurring Demand for Corporate Bonds (November 18, 2025). Available at SSRN: https://ssrn.com/abstract=5763762 or http://dx.doi.org/10.2139/ssrn.5763762

Forecasting Power in Earnings Sentiment

If the numbers are the same, why does the CEO’s tone still change the market’s forecast?

For too long, financial modeling has acted as if only the quantitative data matters, but this paper demonstrates that the narrative woven by corporate management is an incremental and powerful driver of analyst expectations.

Using large language models (LLMs) and a clever “text-morphing” technique, the researcher was able to generate counterfactual earnings call transcripts that systematically varied topical emphasis (the prevailing narrative) while holding quantitative content fixed. This controlled experiment revealed a predictable, and perhaps irrational, systematic bias in expectation formation: analysts consistently over-react to managers’ expressions of optimism and sentiment, while simultaneously under-reacting to discussions of risk and uncertainty. This linguistic content, which goes beyond standard numerical characteristics, significantly improves the prediction of future realized earnings and analyst forecasts.

The findings show that corporate communication isn’t just disclosure, it’s a powerful tool of persuasion, one that helps explain why analyst expectation formation can often feel more behavioral than purely rational.

Matera, G. (2025). Corporate Earnings Calls and Analyst Beliefs. https://arxiv.org/abs/2511.15214

New Seasonality in the Housing Market

Is the spring housing rush starting earlier than it used to, or are you just imagining things?

For decades, the rhythm of the U.S. housing market was utterly predictable: a slow, cold winter yielding to an active spring and summer, with activity peaking in late spring. This paper confirms that this underlying seasonality is alive and well, but the COVID-19 pandemic seems to have permanently shifted the clock.

Researchers found a significant forward shift in the annual peak for both housing prices and sales volumes, which now tend to surge earlier, often hitting their high point around March or April. Moreover, this seasonal effect has become amplified, meaning the swings between the hot and cold seasons are now more pronounced.

The market’s climate matters as well, as colder regions like the Northeast and Midwest show much stronger seasonal swings compared to the milder South and West. The results suggest a thick-market momentum behavior, where rising sales volumes and prices move in lockstep.

Hu, Yihan et al. “Seasonality in the U.S. Housing Market: Post-Pandemic Shifts and Regional Dynamics.” (2025). https://arxiv.org/abs/2511.10808

Gold-Silver Ratio

Trading the gold-silver ratio with machine learning

The gold-silver ratio has been a statistical arbitrage playground for decades, yet this paper shows that the classic mean-reversion strategy can be dramatically improved with ML techniques.

The core idea relies on cointegration, confirming that the long-term relationship between gold and silver prices (using futures and ETFs from 2015-2025) is strong enough for the pair’s spread to be mean-reverting. The technical upgrade starts with using a Kalman filter to dynamically estimate the spread’s hedge ratio, a superior method compared to static Ordinary Least Squares (OLS) which fails to adapt to changing volatility regimes. The final, and most impactful, step is augmenting the trading signal with a machine learning regime filter (using models like Gradient Boosting) trained on volatility, macroeconomic, and sentiment features.

Backtests demonstrate that this ML-filtered approach delivers superior Sharpe ratios and significantly lower drawdowns, especially during high-stress periods like the 2020 COVID crisis.

Mittal, Vineet Kumar and Mittal, Richa, Gold Silver Pair Trading -Mean Reversion Strategy Using Machine Learning (October 01, 2025). Available at SSRN: https://ssrn.com/abstract=5710242 or http://dx.doi.org/10.2139/ssrn.5710242

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.