Recent Academic Research

This week’s best academic research on financial markets

Welcome back to another issue of Recent Academic Research! Let’s get into it.

Crisis Mitigation with PE and VC

During economic meltdowns, alternative investments like private equity and venture capital don’t just provide capital, they are strategic accelerators of recovery.

When economic crises hit and traditional bank financing dries up, private equity (PE) and venture capital (VC) investments step forward as essential, counter-cyclical financial lifelines. This research highlights that the value delivered goes far beyond mere capital injection, encompassing critical strategic guidance, governance improvements, and access to vital networks.

Established PE-backed firms demonstrate remarkable resilience, showing higher operational efficiency, greater revenue growth (an average of 12% higher than non-backed peers in developed markets), and superior employment retention, maintaining 90-95% of pre-crisis workforces within two years. Meanwhile, VC-backed startups drive disproportionate innovation and job creation, particularly in crisis-resilient sectors like technology, healthcare, and renewable energy.

The overall success of these strategies depends heavily on local institutional strength: developed markets with robust regulatory frameworks see faster recovery, while emerging markets face higher risks despite offering superior growth potential.

Ndukaji, Adaobi, Private Equity and Venture Capital in Driving Post-Crisis Economic Recovery: Evidence from Global Markets (September 01, 2025). Available at SSRN: https://ssrn.com/abstract=5460294 or http://dx.doi.org/10.2139/ssrn.5460294

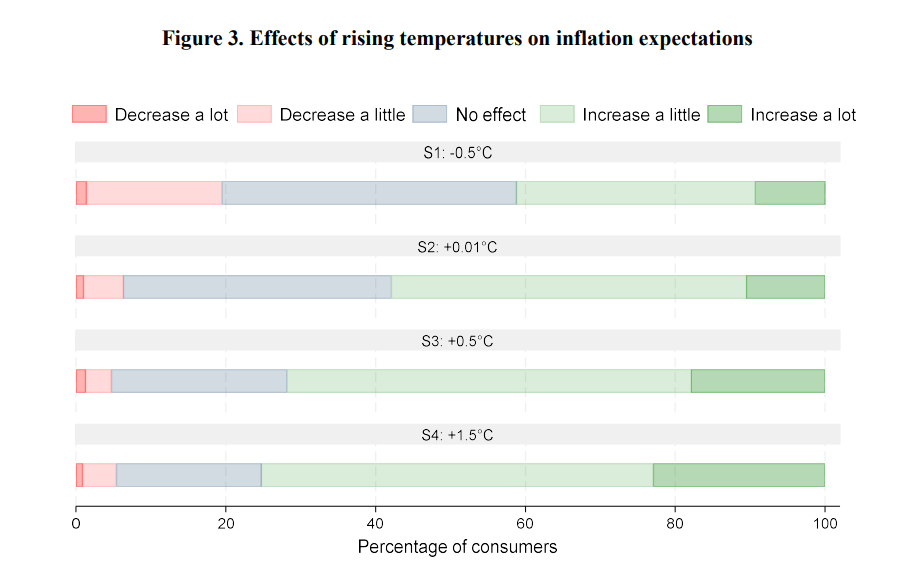

Temperature and Inflation Expectations

How do rising global temperatures instantly reshape consumer expectations for long-term inflation and economic stability?

Researchers utilized a rigorous methodology, conducting a Randomized Control Trial (RCT) within a large-scale, population-representative survey of euro area consumers to estimate the causal effects of climate change scenarios on financial expectations.

By randomly assigning respondents to various hypothetical global temperature change scenarios, the study quantified the economic fallout perceived by households. They found that even a modest 0.5°C rise in global temperatures induces a significant 0.65 percentage point increase in five-year-ahead inflation expectations.

This perceived surge in future prices is primarily attributed by consumers to supply-side issues, such as crop failures, escalating production costs, and supply chain disruptions. Critically, this climate-driven pessimism is broad, leading respondents to anticipate adverse impacts across the macroeconomy, including lower economic growth, higher unemployment, increased government debt, and heavier tax burdens.

Although consumers recognize the damaging economic implications, the study warns that for central banks, “more knowledge about climate change may make it more difficult to maintain price expectations”, posing a direct challenge to anchoring long-term inflation targets.

Georgarakos, Dimitris and Kenny, Geoff and Meyer, Justus and van Rooij, Maarten, How do Rising Temperatures Affect Inflation Expectations? (October 02, 2025). De Nederlandsche Bank Working Paper No. 843, Available at SSRN: https://ssrn.com/abstract=5556539 or http://dx.doi.org/10.2139/ssrn.5556539

Fed Tone and Rates

When monitoring the Federal Reserve, should investors pay more attention to news headlines than to the official statements analyzed by complex AI models?

A simple, straightforward index quantifying the media’s interpretation of central bank tone surprisingly provides valuable and timely insights into market expectations, often outperforming indices built using complex, state-of-the-art language models (LLMs). Researchers created a “Dovishness Index” by tracking the relative frequency of dovish (accommodative) versus hawkish (restrictive) terms in press coverage related to the Federal Reserve.

They found that this measure correlates strongly and significantly with financial asset performance. Most notably, a more dovish reading on the index precedes lower US Treasury bond yields across the curve. The index exhibits an immediate negative relationship with the short-term, two-year bond yield and acts as a leading indicator for the five- and ten-year yields by three months.

This index also anticipates bullish turns in investor sentiment and shifts in short-term consumer inflation expectations. The key takeaway is that market repricing is heavily influenced by “the media’s interpretation of central bank messaging, rather than just the merely capturing the official tone, is key for predicting market reactions”.

Torres, Diego José and Garcia, Pilar and Garcia, Pilar, Perceiving Central Bank Communications through Press Coverage (January 21, 2025). Banco de Espana Working Paper No. 2505, Available at SSRN: https://ssrn.com/abstract=5552578 or http://dx.doi.org/10.2139/ssrn.5552578

Market Concentration and Stock Index Weighting

Does the famous size effect in equal-weighted portfolios truly hinge on the stability of market concentration?

The historical tendency of equally-weighted (EW) stock indices to outperform their capitalization-weighted (CW) counterparts (a phenomenon often associated with the size effect) is shown to be deeply and analytically linked to the degree of market concentration. Using Stochastic Portfolio Theory (a mathematical framework for analyzing portfolio policies), researchers precisely decompose EW relative performance into two key elements: the change in market concentration (how much a few giant stocks dominate the market) and an accumulating benefit called the “excess growth rate”.

A rapid rise in concentration, such as the increase observed since 2016 in the US market, negatively impacts EW performance. However, the study confirms that EW indexing inherently involves contrarian rebalancing, meaning it systematically sells relative winners and buys relative losers during periodic rebalancing, a process that profits from short-term price fluctuations known as “noise harvesting”, leading to perpetually growing gains.

For investors, this decomposition matters immensely, because if market concentration simply stabilizes or mean-reverts historically true for long US samples, notwithstanding the recent increase), the accumulated benefits from contrarian trading are strong enough to ensure long-term outperformance. The analysis indicates that “a mere stabilization of market concentration would thus be sufficient to revive the size effect”.

Rabault, Guillaume and Sivitos, Stamatis and Zheng, Ban, Equal-Weighting: The Contrarian Trading View (October 02, 2025). Available at SSRN: https://ssrn.com/abstract=5557363 or http://dx.doi.org/10.2139/ssrn.5557363

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.