Recent Academic Research

This week’s best academic research on the financial markets

Welcome back to another issue of Recent Academic Research! Let’s get into it.

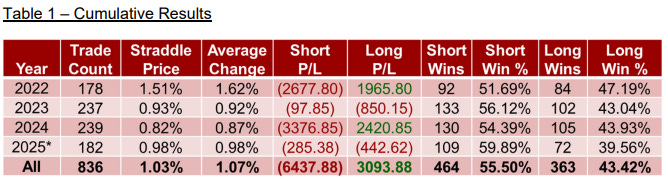

0DTE Index Option Straddle Strategy

Testing Long/Short short-dated option strategies on the Nasdaq-100

The widespread availability of daily-expiring index options (0DTEs) has made collecting premium decay (theta) a common short-term strategy, particularly in the highly liquid Nasdaq-100 (NDX) index. The authors wanted to test if this premium collection is consistent across the week, so they examined the simplest strategy: consistently buying or selling a 1-day At-the-Money (ATM) NDX straddle at the close the day before expiration.

The authors found that from 2022 - 2025 YTD, a long straddle strategy resulted in positive PnL, while a short straddle strategy resulted in negative PnL.

Additionally, the authors found that results varied by the day of the week that the option expires. Specifically, the short straddle strategy produced positive returns on Mondays while neither long or short strategy produced positive returns on Tuesdays. On Wednesday, Thursday, and Friday, the long straddle strategy produced positive PnL and the short straddle strategy produced negative PnL.

This suggests that market participants, whether by systematic demand, market-maker positioning, or liquidity conditions, price next-day volatility differently depending on the day of the week.

Rhoads, Russell, NDX 1-Day Straddle Pricing: Are there Better Days than Others to Buy or Sell Straddles? (October 19, 2025)., Available at SSRN: https://ssrn.com/abstract=5628270 or http://dx.doi.org/10.2139/ssrn.5628270

Disagreement on Tail Risk

What if investors disagree about a stock’s potential for total catastrophe?

The degree of investor disagreement about a firm’s outlook is a well-known factor in asset pricing, but conventional measures tend to focus only on differences in average forecasts. The authors hypothesized that belief dispersion about extreme downside events is actually more critical and developed a new measure, Disagreement on Tail (DOT), to capture it.

Their rigorous method used 100 distinct neural network models (NNMs) to simulate “investors” and quantified DOT as the standard deviation of their probability forecasts for a stock incurring a massive loss. They found a robust, negative relationship: stocks with high DOT values (high disagreement on tail risk) tend to have significantly lower subsequent returns. A value-weighted (equal-weighted) long-short portfolio that shorts stocks in the bottom DOT decile and goes long in the top yields an average monthly return of -1.07% (-0.98%), underscoring DOT’s predictive power.

The evidence aligns with a mispricing channel, where optimistic investors (unconstrained by short-sale rules) bid up the price based on their divergent, rosy forecasts of disaster avoidance.

Chen, Haiwei and Chen, Haiwei and Chen, Yong and Li, Jiangyuan and Luo, Dan, Disagreement on Tail (October 05, 2025). Available at SSRN: https://ssrn.com/abstract=5628930 or http://dx.doi.org/10.2139/ssrn.5628930

Crypto Carry

Is the extremely high, persistent yield from the crypto carry trade a sign of inefficiency caused by limited arbitrage, or is it compensation for fundamental risk?

For years, the difference between crypto futures and spot prices, known as the crypto carry, has offered a consistently high yield, sometimes exceeding 40% per annum for major coins like Bitcoin and Ether. The authors’ analysis demonstrates that this volatile premium cannot be explained by standard economic factors, such as interest rate differentials or fundamental risk. Instead, they attribute the anomaly to a substantial market inefficiency driven by two structural forces.

First, heavy buying pressure from trend-chasing investors seeks leveraged futures exposure, thereby structurally bidding up the futures price. Second, the persistent size of the carry reflects “structural limits to arbitrage” (specifically, regulatory hurdles and margin constraints) that prevent sophisticated players from fully executing the cash-and-carry trade that would normalize pricing.

BIS Working Papers, No 1087, Crypto carry, by Maik Schmeling, Andreas Schrimpf and Karamfil Todorov. Monetary and Economic Department. April 2023 (revised October 2025). https://www.bis.org/publ/work1087.pdf

0DTE Options and Market Volatility

Does the recent explosion in Zero-Days-to-Expiration (0DTE) S&P 500 options trading actually destabilize the market, or does it quietly stabilize it?

The popular narrative holds that the massive growth in Zero-Days-to-Expiration options (0DTEs) is a dangerous new source of “gamma-driven” volatility in the S&P 500. The authors, however, present a compelling case challenging this view, finding precisely the opposite effect: the mere presence of 0DTEs on a given day actually dampens S&P 500 index volatility.

By carefully using exogenous variation in expiration days, they observed that the index’s daily realized volatility is, on average, lower by 61 annualized basis points on days when these contracts expire.

The stabilizing mechanism is found in the systematic hedging of market makers. The shifting exposure from options maturing into 0DTE status forces market makers to execute trades in the underlying index futures that move against the index’s price direction. This acts as an automated, counter-cyclical force that strengthens order-flow reversals and reduces momentum. The authors’ evidence shows the option intermediary’s systematic role can “lead to a reduction in aggregate volatility”.

Adams, Greg and Dim, Chukwuma and Eraker, Bjorn and Fontaine, Jean-Sebastien and Ornthanalai, Chayawat and Vilkov, Grigory, Do S&P500 Options Increase Market Volatility? Evidence from 0DTEs (October 17, 2025). Available at SSRN: https://ssrn.com/abstract=5641974 or http://dx.doi.org/10.2139/ssrn.5641974

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.