Recent Academic Research

Expert forecasts on AI impact, earnings strategy from prediction market information, importance of climate risk, and an improved bond model

Welcome back to another issue of Recent Academic Research! Let’s get into it.

Forecasts for AI’s Impact

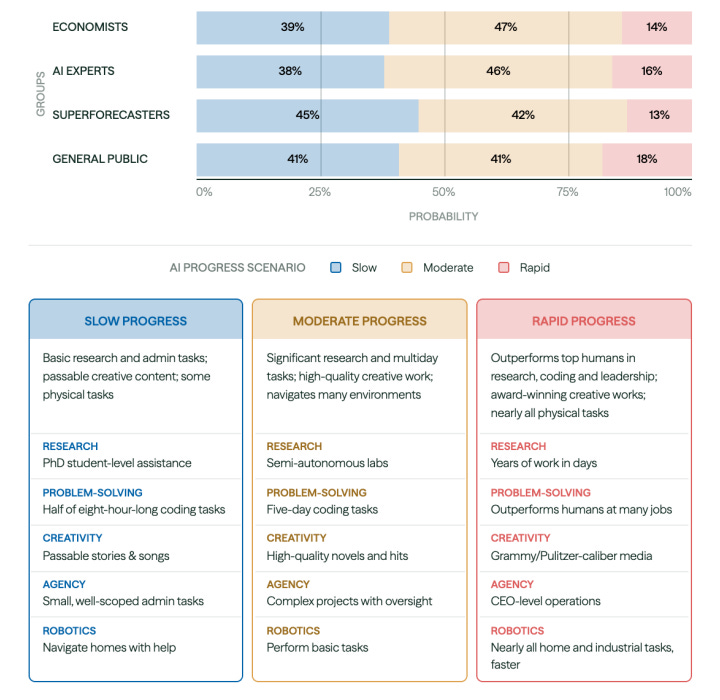

Most experts anticipate significant breakthroughs in artificial intelligence by 2030, yet they expect historical adoption lags and structural bottlenecks to keep the resulting economic growth within historical bounds.

This week, I found an NBER paper that surveys the “brain trust” (everyone from academic economists to the engineers building frontier models) and the results offer a new perspective on how AI will shape markets.

While almost everyone expects systems to surpass human ability in most tasks by 2030, the median forecast for economic growth stays remarkably close to historical trends at roughly 2.5 percent. The real friction, according to these experts, isn’t the code itself but the messy reality of how slowly businesses actually retool their operations and how aging populations might drag on productivity gains.

Interestingly, the industry insiders are far more bullish on growth than the academics, who worry more about a permanent dip in labor force participation.

This gap suggests that while the technology is moving quickly, the markets will likely not exhibit a rapid change, but rather an uneven and slow change. Investors should keep an eye on the transition period, as the authors argue that “policymakers cannot simply plan for the median outcome” given the high uncertainty involved.

Ezra Karger, Otto Kuusela, Jason Abaluck, Kevin A. Bryan, Basil Halperin, Todd R. Jones, Connacher Murphy, Philip Trammell, Matt Reynolds, Dan Mayland, Ria Viswanathan, Ananaya Mittal, Rebecca Ceppas de Castro, Josh Rosenberg, and Philip Tetlock, “Forecasting the Economic Effects of AI,” NBER Working Paper 35046 (2026), https://doi.org/10.3386/w35046.

Prediction Markets and Earnings

A small minority of prediction market traders consistently outperforms analyst consensus by identifying earnings misses that trigger significant, multi-day stock price declines.

A new research paper explores how traders on the Polymarket platform are outperforming traditional analyst consensus by betting on corporate earnings results.

While sell-side analysts often provide a "walk-down" estimate, which is a systematically depressed figure that companies can easily beat to signal competence, the prediction market crowd provides a more objective reality check.

The study demonstrates that when these markets assign a low probability of a beat, a short-only strategy earns 5.90 percent over the following ten days. This accuracy is not driven by the general public but by a small "contrarian minority" of 22 sophisticated wallets that specialize in specific market domains.

This bearish signal is particularly effective because institutional constraints, such as borrowing costs or fiduciary rules, often prevent equity markets from pricing in bad news immediately. The paper concludes that "the crowd's advantage is concentrated in pricing operating fundamentals".

Feng, Chloe, Minority Report: Contrarian Traders, Prediction Markets, and the Return of Post-Earnings Drift (March 18, 2026). Available at SSRN: https://ssrn.com/abstract=6477080 or http://dx.doi.org/10.2139/ssrn.6477080

Integrating Climate Risk

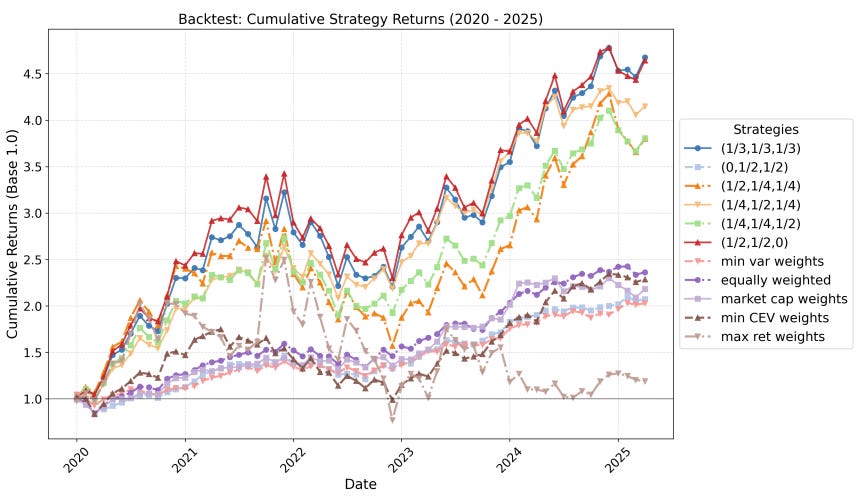

Integrating local temperature anomalies into portfolio optimization can nearly double annual growth rates by systematically reducing exposure to climate driven volatility.

A new research paper introduces two sophisticated metrics (Climate Risk Exposure and Climate Exposure Volatility) to help investors navigate the growing financial threats of extreme weather. While many traders rely on static country level indices to guess environmental risk, these new tools track how the changing frequency of heatwaves and temperature spikes actually interacts with a company’s physical assets.

By analyzing global equity portfolios between 2020 and 2025, the study found that portfolios optimized for climate resilience significantly outperformed traditional benchmarks. For example, a balanced strategy that weighed climate risk alongside market returns achieved a 33.5 percent annual growth rate, more than doubling the 15.8 percent return of a standard market cap weighted approach.

The authors argue that “extreme temperature events exert a negative effect on most sectors,” making climate exposure a critical factor in managing future drawdowns. Identifying firms with high asset intensity in volatile regions is becoming a fundamental way to generate returns in an increasingly unstable environment.

Azzone, Michele et al. “Temperature Anomalies and Climate Physical Risk in Portfolio Construction.” (2026).

Improving Bond Models

Compressing daily news, market data, and macro releases into a single vector reveals hidden economic risks that traditional yield curve models fail to capture.

A new research paper proposes a novel way to quantify the aggregate economic state by treating each trading day like a word in a sentence, mapped into a dense vector through machine learning. This “world embedding” fuses everything from news narratives and geopolitical risk to raw financial data and central bank communications into a unified, daily metric.

For decades, fixed income traders have struggled with the “spanning puzzle,” which is the observation that the yield curve shape often fails to account for all relevant macroeconomic information. By using this multimodal representation, the author finds that “economic similarity is encoded as distance in the learned space,” allowing the model to uncover unspanned risks that standard models ignore.

In practice, adding these embedding factors increases the predictive power for bond excess returns by 10 to 34 percentage points beyond traditional yield curve factors.

Tabatabaei, Elham, World Embedding: The Daily Economic State and Bond Risk Premia (March 31, 2026). Available at SSRN: https://ssrn.com/abstract=6503446

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.