Recent Academic Research

This week’s best academic research on financial markets

Welcome back to another issue of Recent Academic Research! Let’s get into it.

Macro Announcements and Intraday Momentum

In China, macro news creates same-day trends in stocks, strongest when the news adds stock-specific information.

The paper asks why intraday momentum spikes on policy days, then tests an information channel. It measures each stock’s incremental news content with DVAR, a simple gauge that compares the variance of a stock’s abnormal returns in a short announcement window to nearby non-event days after removing six standard risk factors. Higher DVAR means the announcement added more stock-specific information that prices have not fully absorbed.

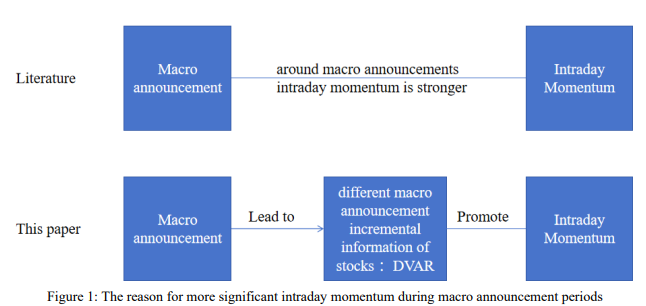

Using A-share tick data from 2013 to 2023, the authors split trading into non, pre, mid, and post announcement windows. They confirm that the opening half-hour predicts the closing half-hour on most days, and the link is much stronger during the announcement window. The key result is that momentum intensifies precisely in stocks with higher DVAR during the announcement window across top meetings, fiscal, and monetary news, pointing to incremental information rather than the event label as the driver. The figure below, from the paper’s literature review, contrasts the older view (“macro days have more momentum”) with the authors’ mechanism where macro news adds uneven information across stocks, which then fuels same-day trends.

Mechanism tests show institutions adjust positions infrequently and, when DVAR is high, those slow rebalances line up from morning to close, while retail “late-informed” trading weakens. Results come from China’s largely unscheduled policy environment, so portability to scheduled regimes may be limited.

Zhang, Xiang and Zhang, Ke and Li, Yulu and Pan, Zhiyuan, Stock’s Macro Announcement Incremental Information and Intraday Momentum. Available at SSRN: https://ssrn.com/abstract=5413265 or http://dx.doi.org/10.2139/ssrn.5413265

Spillovers of Earnings Surprises

Earnings news does not stop at the firm that reports. It spills over to close peers and moves their prices too.

The paper shows a simple way to track those spillovers. It turns each firm’s earnings call into a short text fingerprint, finds the closest peers by language, then projects the reporter’s earnings surprise onto those peers. The authors call this projected SUE, which is just the reporter’s surprise weighted by text similarity. When a company reports, its own stock moves about 12 basis points for a one standard deviation surprise. Its closest peers move about 3 basis points the same day, and about 2 basis points the next day, showing that news travels across related names. The gap does not close right away. Returns drift for several days after the news before they die out.

A simple peer long short portfolio built on projected SUE earns about 11 percent a year with a Sharpe near 1.75 in sample. At the market level, aggregating these projected surprises helps explain many so called anomaly returns and improves next day forecasts for value style returns. As the authors put it, “drift sustains for around 20 days.” The effect fades by about day 20 and depends on earnings call text, so thin coverage can weaken it.

Zhang, Cong and He, Zhenzhi and He, Zhenzhi, Cross-Sectional Spillovers of Earnings Surprises and Asset Price Anomalies (August 28, 2025). Available at SSRN: https://ssrn.com/abstract=5415255 or http://dx.doi.org/10.2139/ssrn.5415255

LLMs for FX Markets

A small fine tuned LLM reads FX news more accurately than older tools and turns it into a tradable signal.

The authors fine tune an open Llama 3.1 model on FX news and classify each article’s view of the past and the next few days for the G10 currencies, the major developed market currencies. They combine human labels with distant labels, which are tags inferred from five day returns before or after publication to scale training data efficiently. Legacy baselines like FinBERT, VADER and the Loughran McDonald dictionary cannot separate past and future and require sentence by sentence aggregation, whereas the fine tuned model reads full articles and assigns both labels directly. On a small human test set, the fine tuned version leads on both past and future classification. Figure 2 tracks a simple zero cost long short G10 portfolio built from daily article signals and shows the fine tuned model as the only approach with steady gains across sources, with DailyFX exceeding 10 percent since 2020, which signals economic relevance beyond accuracy.

The authors put it plainly, “fine tuned LLMs offer strong potential for sentiment analysis in the FX market.” They also conclude, “The fine tuned Llama model generates profitable trading signals.” The main caveats are that performance differs by news source and that truly neutral stories remain hard to classify, so practitioners should monitor source mix and focus signals on clear appreciation or depreciation cues.

Ballinari, Daniele and Maly, Jessica, FX Sentiment Analysis with Large Language Models (August 26, 2025). Swiss National Bank Working Paper No. 2025-11, Available at SSRN: https://ssrn.com/abstract=5406332 or http://dx.doi.org/10.2139/ssrn.5406332

Volatility Forecasting

Can an interpretable regime switching model beat deep learning at forecasting next day market volatility?

The paper compares classic econometric models with popular machine learning models for predicting realized volatility of the S&P 500. It tests linear HAR models and their regime switching versions, which allow dynamics to change in high versus low volatility states, against tree based and neural network models across 1996 to 2023. The headline finding is consistent, when only past volatility is used as input, the threshold and smooth transition HAR models, especially STHAR, beat both linear HAR and a wide set of ML models on forecast accuracy and practical use.

“The clear winner in terms of achieving the lowest MSPE and QLIKE is the STHAR model.” Beyond accuracy, STHAR delivers the best risk forecasts and strong realized utility, and its Value at Risk coverage is reliably closer to target, which matters for portfolios that must size positions to a risk limit. The authors conclude that model choice should track the data you actually have, not the flashiest architecture, since “ML models are not a one-size-fits-all solution to the challenges of RV prediction.”

Kılıç, Rehim, Linear and Nonlinear Econometric Models Against Machine Learning Models: Realized Volatility Prediction (August, 2025). FEDS Working Paper No. 2025-61, Available at SSRN: https://ssrn.com/abstract=5401194 or http://dx.doi.org/10.17016/FEDS.2025.061

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.

very interesting insights