Recent Academic Research

An exploration of the hidden structural, behavioral, and technological mechanisms driving market liquidity, risk management, and price formation.

Welcome back to another issue of Recent Academic Research!

Let’s get into it.

How Interest Rate Swaps Flatten the Yield Curve

Access to efficient interest rate swaps flattens the government bond yield curve by lowering the cost of managing interest rate risk over time.

When a major economy opens its financial borders, it gives us a clean look at how derivative markets interact with cash assets. By evaluating China’s recent integration of its onshore swap market, this research reveals that giving investors access to high-quality hedging tools compressed the government bond term spread by about nine basis points. Interestingly, this flattening effect is not driven by investors stripping out risk when a trade is initiated, but rather by their ability to dynamically manage duration over the entire holding period. When managing active exposure becomes cheaper and less plagued by basis risk, investors are naturally more comfortable holding longer-dated bonds.

This increased willingness to hold duration means that financial intermediaries absorb less risk on their balance sheets, requiring less compensation. Ultimately, the data confirms that “better-functioning interest rate derivative markets can flatten the government bond yield curve”. This highlights a powerful complementarity: a healthy derivatives ecosystem does not cannibalize cash trading, it strengthens it, lowering long-term financing costs for issuers and creating a more stable environment for macro portfolios.

Institute for Monetary and Financial Research, Hong Kong, How Interest Rate Swaps Reshape the Yield Curve (May 13, 2026). Hong Kong Institute for Monetary and Financial Research (HKIMR) Research Paper No. 03/2026, Available at SSRN: https://ssrn.com/abstract=6756880

The Dollar as an FX Liquidity Superspreader

A new study reveals that while the US dollar acts as an efficient, passive intermediary for global currency trading during normal times, it transforms into a dangerous systemic “superspreader” of illiquidity during financial crises.

The foreign exchange market is the largest financial market in the world, but its plumbing relies on a hidden geometry where most minor currency pairs cannot be traded directly and must instead be synthesized through the US dollar. In tranquil periods, this triangular setup works beautifully, allowing market makers to quietly disperse local shocks across the network. However, when market stress binds dealer balance sheets, this efficient intermediary mechanism abruptly breaks down. Instead of acting as a passive vehicle, liquidity shocks now originate directly within core dollar pairs and rapidly radiate outward, synchronizing a market-wide evaporation of liquidity across seemingly unrelated currency crosses.

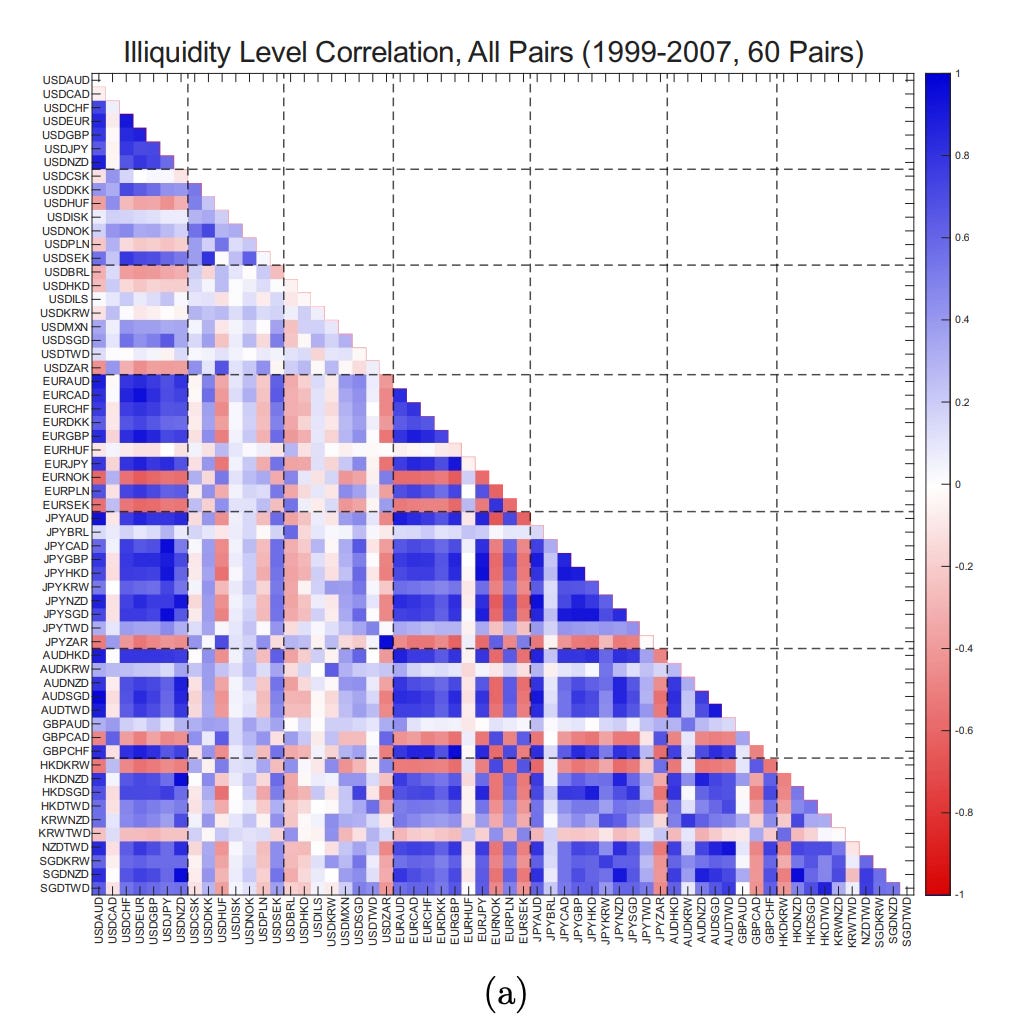

Figure 1: Illiquidity level correlations. Panel (a) displays the correlation matrix for 60 currency pairs from 1999–2007, showing a mix of positive (blue) and negative (red) correlations, indicating varied liquidity dynamics during this period. Panel (b) presents the same matrix for 2007–2013, revealing a significant shift toward stronger, widespread positive correlations (dominantly blue), suggesting increased systemic liquidity risk and market integration during the crisis era.

This regime shift causes traditional risk models to fail precisely when accuracy is most critical, because they mistakenly assume currency correlations remain static during a panic. For investors and traders, this finding matters because it uncovers the hidden structural costs of execution risk. Ignoring this triangular geometry means systematically underestimating how fast transaction costs can spike during a crisis, proving that the dollar is an efficient bridge in calm waters but a major vector for contagion when the wind blows. As the author notes in the paper’s conclusion, “ignoring network topology leads to a systematic mispricing of liquidity risk.”

Institute for Monetary and Financial Research, Hong Kong, FX Illiquidity Networks and Vehicle Currencies (May 13, 2026). Hong Kong Institute for Monetary and Financial Research (HKIMR) Research Paper No. 04/2026, Available at SSRN: https://ssrn.com/abstract=6756859

De-Risking Momentum with Adaptive Execution

By pairing traditional trend strength strategies with an adaptive machine learning layer, investors can capture steady market gains while actively dodging catastrophic momentum crashes.

Traditional trend following strategies are notoriously difficult to manage because they are highly vulnerable to sudden, violent market reversals. When market regimes abruptly shift, yesterday’s winning stocks can instantly plummet, causing devastating portfolio drawdowns. This paper introduces an elegant fix by separating asset selection from execution timing, utilizing a smart reinforcement learning model that treats trading as a series of dynamic, daily choices rather than rigid monthly actions. Tested across both the United States and Chinese equity markets, this framework consistently outpaced traditional passive indexes and static trend strategies.

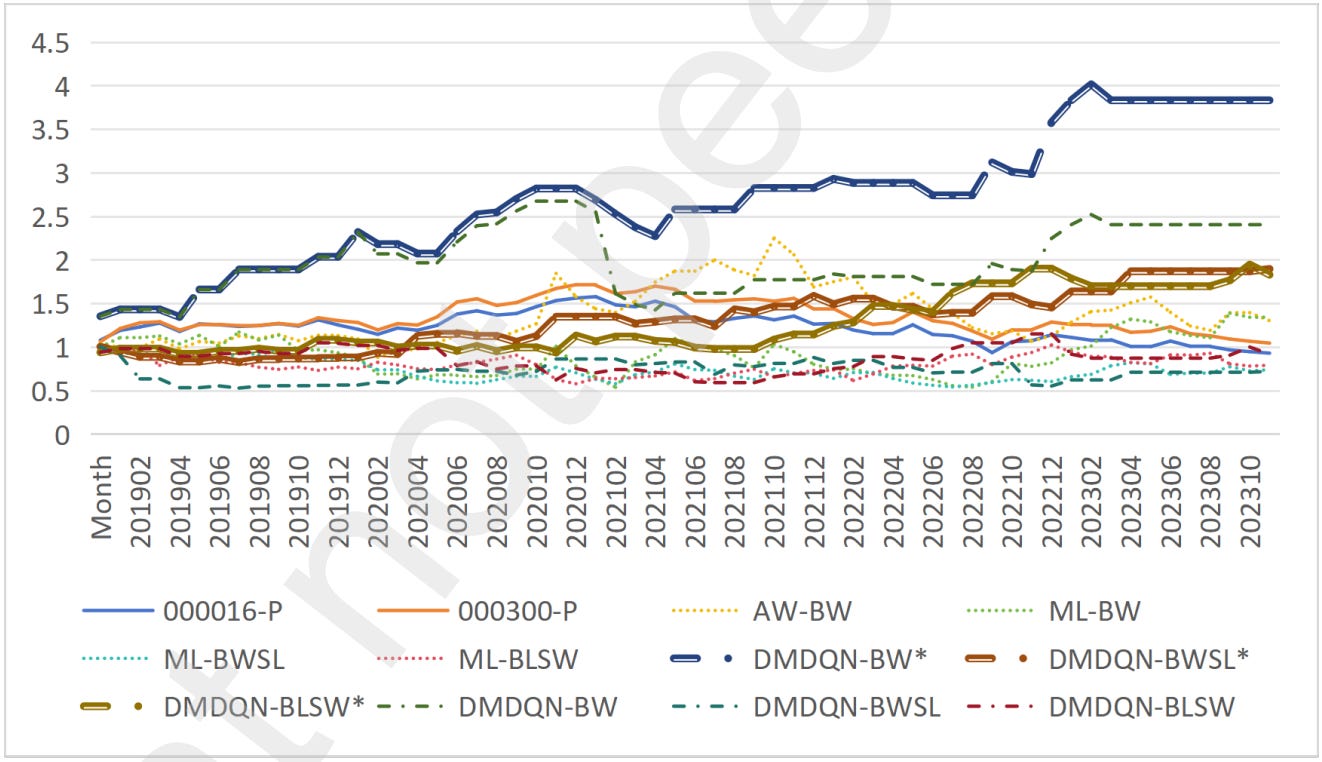

Figure 2: Monthly cumulative return net (RN) trajectories of DMDQN and benchmark strategies in the China market (HP signal), 2019–2023. ∗ indicates stop-loss liquidation triggered at RN < 0.94.

The real magic happens during market panics, where the automated agent learns to step aside, lock in profits, or trigger disciplined liquidations. By shifting exposure away from toxic environments, the system managed to cap historical drawdowns significantly while keeping equity curves remarkably smooth. For investors, this demonstrates that execution timing matters just as much as stock picking. Ultimately, this adaptive framework proves that intelligent timing “effectively reduces the crash risk associated with traditional momentum investing,” turning a notoriously brittle anomaly into a resilient asset management tool.

Deng, dongya and Xu, Donghai and Li, Yuanshun and Ji, Xiaodong and Xu, Wei, Dynamic Momentum Trading via Deep Q-Networks: An Intelligent Execution Framework for Portfolio Management. Available at SSRN: https://ssrn.com/abstract=6765671 or http://dx.doi.org/10.2139/ssrn.6765671

How Human Cognition Shapes Market Prices

Standard financial market behaviors, such as volatility clustering and price unpredictability, can emerge naturally from the basic ways the human brain processes information and makes decisions.

This paper introduces a simulated market model showing that complex financial behaviors are fundamentally a reflection of human psychology. By applying a prominent cognitive model of binary choice to simple buy and sell transactions, the researchers demonstrate how independent market participants accumulate noisy evidence before executing their trades. When these individual psychological processes are combined with a basic price impact mechanism, the model naturally replicates major market phenomena like volatile trend changes and long memory in trading patterns without needing complex institutional rules.

Intriguingly, because the model relies entirely on how individual traders respond to shifting price loops, it also spontaneously generates realistic market cycles and asset bubbles. This close alignment tells us that “asset prices may indeed be essentially traced back to the way human cognition” operates. This pedagogical exercise implies that deeply ingrained human biology, rather than intricate market architecture, may be the primary driver behind the persistent irregularities, trading risks, and structural breaks we observe in daily market data.

Mazzon, Andrea and Patacca, Marco and Torricelli, Lorenzo, Cognitive Models for Market Price Formation (May 12, 2026). Available at SSRN: https://ssrn.com/abstract=6753698 or http://dx.doi.org/10.2139/ssrn.6753698

This week for paid subscribers

Paid subscribers are diving into the structural mechanics of ERCOT power markets to exploit the Volatility Risk Premium. This walkthrough explores a Virtual INC strategy, maps out the "sunset anomaly," and includes a sensitivity analysis on transaction friction. Python backtest code included.

Disclaimer: The content provided in this newsletter, “Alpha in Academia,” is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.