When Is the Crowd Wrong?

[WITH CODE] A 16-year test of the "Managed Money" positioning signal across silver, gold, and copper.

Hello and welcome back to another paid post!

Today we are going to take one of the most repeated headlines in all of commodity markets and ask whether there is any money in doing the exact opposite. The idea is old and intuitively appealing: The fast money crowds into a trade, the trade gets stretched, and the crowd, as crowds tend to, eventually gets carried out. If that story is true, then the crowd’s own positioning should tell you when to fade it.

Let’s dive right in.

The Cheat Sheet the Government Publishes Every Friday

Every week, the Commodity Futures Trading Commission (CFTC) releases something called the Commitments of Traders (COT) report, and it is one of the closest things retail traders have to seeing the other side of their own hand. The report takes every major futures market and sorts the people holding positions into buckets, based on who they actually are and why they are there. Two of those buckets matter for us, and the whole strategy lives in the tension between them.

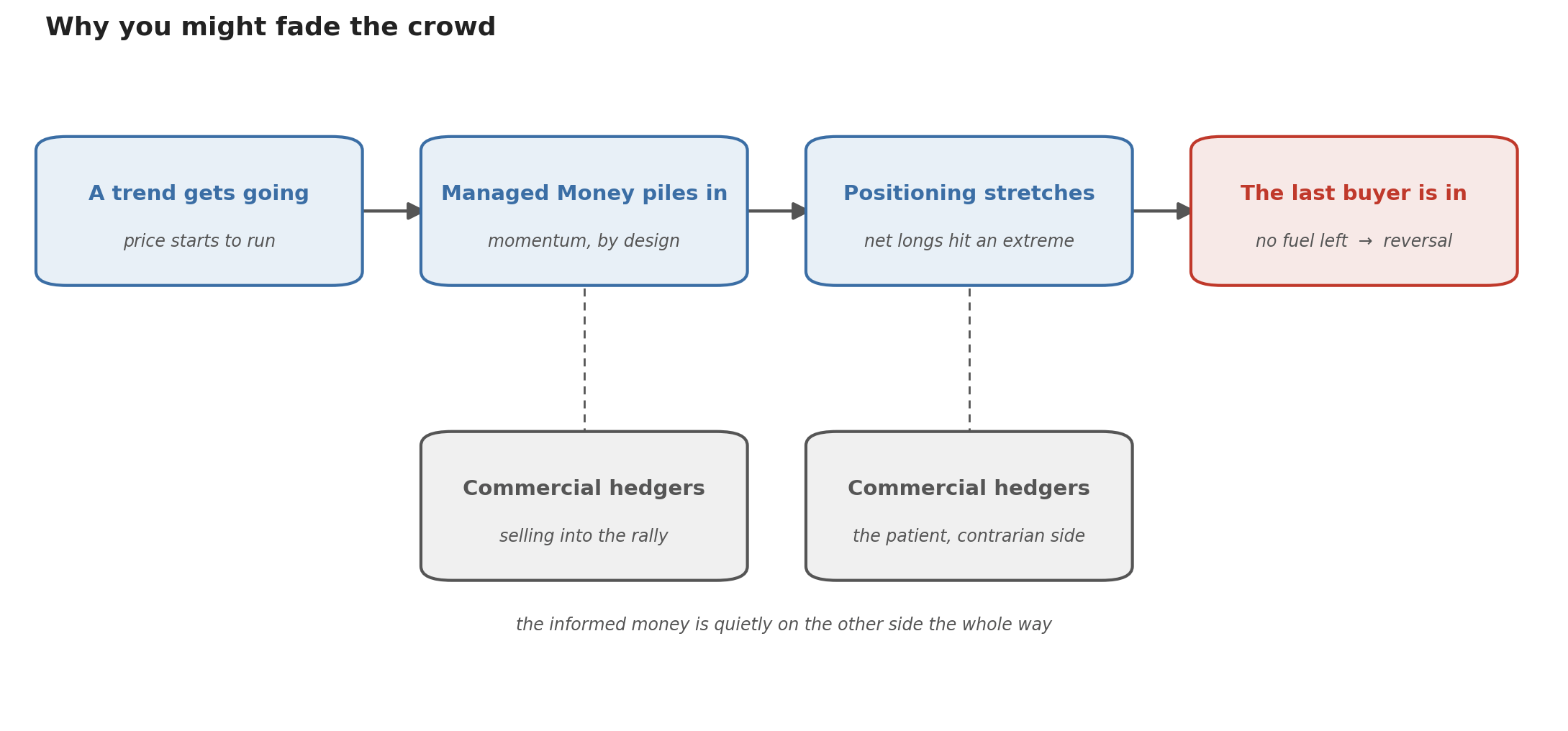

The first is Managed Money. The hedge funds, the commodity trading advisors, the systematic algorithms that now do much of the trading in commodity futures. This is the fast money, and it has one defining behavioral trait: It chases trends. When a price move establishes itself, these strategies pile in, and the further the move runs, the heavier they lean into it.

The second bucket is the producers and merchants. The commercial hedgers, the mining companies and refiners and farmers who are in the market not to speculate but to offload the price risk of an actual physical business. They sell into strength and buy into weakness, because that is simply what hedging looks like from the inside.

This split is worth being precise about, because it is the entire foundation of the trade. The behavior falls out of what each group is actually there to do. The fast money is, by design, momentum money. Trend-following is the strategy, so a position gets bigger precisely because the trend has already been running. The commercial hedger does the opposite, selling into rallies and buying into dips, because that is the mechanical consequence of hedging a physical business rather than a view. So the two buckets are almost always leaning against each other, and the informed, patient side of that tug-of-war tends to be the boring one: the hedger. The exciting money, the money that makes the headlines, is the crowd that supplies the fuel on the way up and, potentially, the exit liquidity at the top.

The theory in one line: Crowded speculative positioning is supposed to mark the moment a trend runs out of fuel. The commercial hedgers are quietly on the other side of that trade the whole way up.

That sets up a clean and testable hypothesis. If Managed Money is structurally the trend-chasing crowd, then a genuinely extreme Managed Money position should mark the moment of maximum exhaustion, the point where the trend has pulled in the last willing buyer and has nowhere left to go but back. Fade the extreme, and in theory you are stepping in front of the crowd at exactly the right moment.

Keep reading with a 7-day free trial

Subscribe to Alpha in Academia to keep reading this post and get 7 days of free access to the full post archives.