Regime-Based Momentum in Rates

[WITH CODE] Exploring a high-Sharpe ratio momentum result in the rates market

Reviewed and updated — 22 July 2026.

Hello!

Today, we will be investigating momentum in the U.S. Treasuries market.

First, I will highlight two academic papers that influenced this post. Then, I will show my exploratory analysis and a retrospective, in-sample regime exercise. The final result is useful for generating a hypothesis, but it is not a validated trading strategy because the cycle boundaries were identified with hindsight.

Let’s get into it.

Academic Literature

The papers below find significant evidence of momentum in the U.S. Treasury market, identifying persistent return patterns that are not fully explained by standard financial models.

Sihvonen’s1 research focuses on time-series momentum, where a bond’s own past returns predict its future returns. He finds this effect is driven primarily by autocorrelation in yield changes, rather than by bond “carry”.

Because yield changes are tied to monetary policy, this phenomenon is also related to the post-FOMC announcement drift (which Alpha in Academia has explored in prior paid-only posts). The paper’s central conclusion is that this momentum factor is “unspanned” (which simply means that the momentum factor provides new, additional predictive information about future bond returns that is not already contained in the current yield curve). This finding contradicts standard term-structure models, which imply all predictive information should already be priced into current yields.

Durham’s paper2, in contrast, investigates cross-sectional momentum by creating trading rules that compare different “duration buckets” along the yield curve. He designs a strategy that goes long the bonds that were “winners” and short the “losers,” while remaining “duration-neutral” to insulate the portfolio from parallel shifts in the yield curve. This strategy generated “sizeable excess returns”; a long-short, zero-duration version yielded up to 207 basis points annually with an information ratio up to 1.01.

Similar to Sihvonen’s findings, Durham concludes that these abnormal returns cannot be fully explained by standard Gaussian arbitrage-free affine term structure models (GATSMs). The momentum strategy demonstrated a “meaningfully positive” alpha, suggesting a persistent anomaly that is not simply compensation for known duration risks.

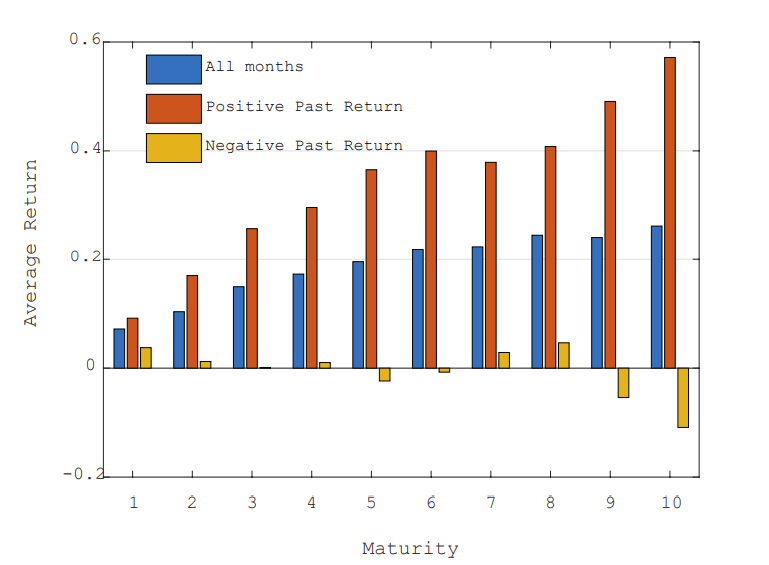

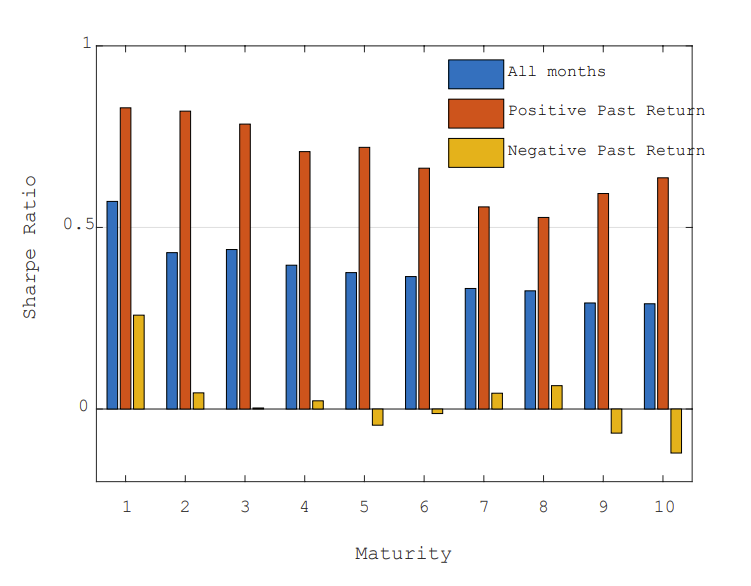

Together, these papers provide evidence that momentum in Treasury returns is worth investigating. My exercise below is much simpler: it uses changes in constant-maturity yields rather than bond total returns, and it should not be read as a replication of either paper.

Keep reading with a 7-day free trial

Subscribe to Alpha in Academia to keep reading this post and get 7 days of free access to the full post archives.