Recent Academic Research

The frequency spectrum of inflation, the gap between economic data and market expectations, and the credibility trap in the Fed put

Welcome back to another issue of Recent Academic Research! Let’s get into it.

Forecasting Inflation

If you want to predict where inflation is going, you have to stop treating it like a single number and start treating it like a frequency spectrum.

Most inflation models fail because they smash short-term noise and long-term trends into one aggregate mess, but this paper from the Bank of Finland argues that the “sum-of-the-cycles” method offers a vastly superior alternative. By using wavelet decomposition, the author breaks inflation down into distinct frequency components ranging from quarterly shocks to multi-year structural shifts.

This allows for a modular forecasting approach where you might use financial variables to predict high-frequency noise while using labor market slack or shortage indicators to forecast the low-frequency trend. The results are striking because this method reduces forecast errors by nearly 50 percent at long horizons compared to standard benchmarks like the random walk.

Crucially, the model didn’t break during the post-2020 inflation surge because it was able to isolate and incorporate supply bottlenecks at the correct frequencies.

Verona, Fabio, Forecasting Inflation: The Sum of the Cycles Outperforms the Whole (January 07, 2026). Bank of Finland Research Discussion Paper No. 1/2026, Available at SSRN: https://ssrn.com/abstract=6043714 or http://dx.doi.org/10.2139/ssrn.6043714

Credibility and Fundamentals

The market reacts wildly differently to identical Federal Reserve actions depending on whether investors fundamentally trust the rules of the game.

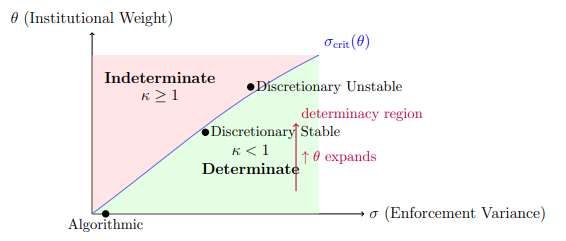

This paper builds on the idea of “monetary scarcity” (the foundational promise that money is limited and cannot be printed at will). The core concept introduced is “enforcement variance,” which measures the uncertainty regarding whether the central bank will actually stick to its rules.

When enforcement variance is low (high credibility), we are in a “determinate regime” where stocks trade logically based on growth expectations. But when variance spikes (meaning investors fear the Fed might debase the currency to solve a crisis) we flip into an “indeterminate regime” where fundamental values don’t matter, and inflation fears dominate.

The authors demonstrate that a strategy switching between equities, volatility instruments, and gold based on this signal generates significant alpha.

This implies the “Fed put” is not guaranteed; aggressive easing during a high-variance regime can actually crash the market because it confirms investors’ fears that the monetary constraints are broken.

Posselt, Johannes Maria, Trading Scarcity Credibility: An Equity Index Strategy Based on Monetary Enforcement Regimes (January 05, 2026). Available at SSRN: https://ssrn.com/abstract=6029194 or http://dx.doi.org/10.2139/ssrn.6029194

Market and Data Divergence

The bond market is theoretically forward-looking, yet it frequently lags behind realized economic data in ways that create predictable repricing opportunities.

This paper introduces “Macro-Market Divergence” (MMD) to quantify the friction between “hard” economic data and the “soft” expectations implied by bond yields. Instead of just looking at price levels, the authors compare the “regime” implied by the data (e.g., is the economy objectively in a recession?) against the regime priced into the yield curve.

When the distance between these two probability distributions widens (meaning the data screams one thing while the bond market prices in another) it signals that the market has failed to update its priors. High divergence is distinct from simple volatility (MOVE index) and serves as a specific diagnostic for when the market is “wrong” about the macro state.

The research finds that these periods of denial are statistically associated with a subsequent snap-back in the “belly” of the curve (intermediate maturities) over the following year, offering a clear signal for mean-reversion trades.

Ismail, Mohamed Iqbal and Donfack, Hermann, Macro-Market Divergence: A Regime-Based Distance Between Fundamentals and Bond Market Expectations. Available at SSRN: https://ssrn.com/abstract=6023492 or http://dx.doi.org/10.2139/ssrn.6023492

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.