Recent Academic Research

Bond market-making toxicity, retail liquidity provider dynamics, monetary policy leverage cycles, and compounding volatility drag boundaries

Welcome back to another issue of Recent Academic Research!

Let’s get into it.

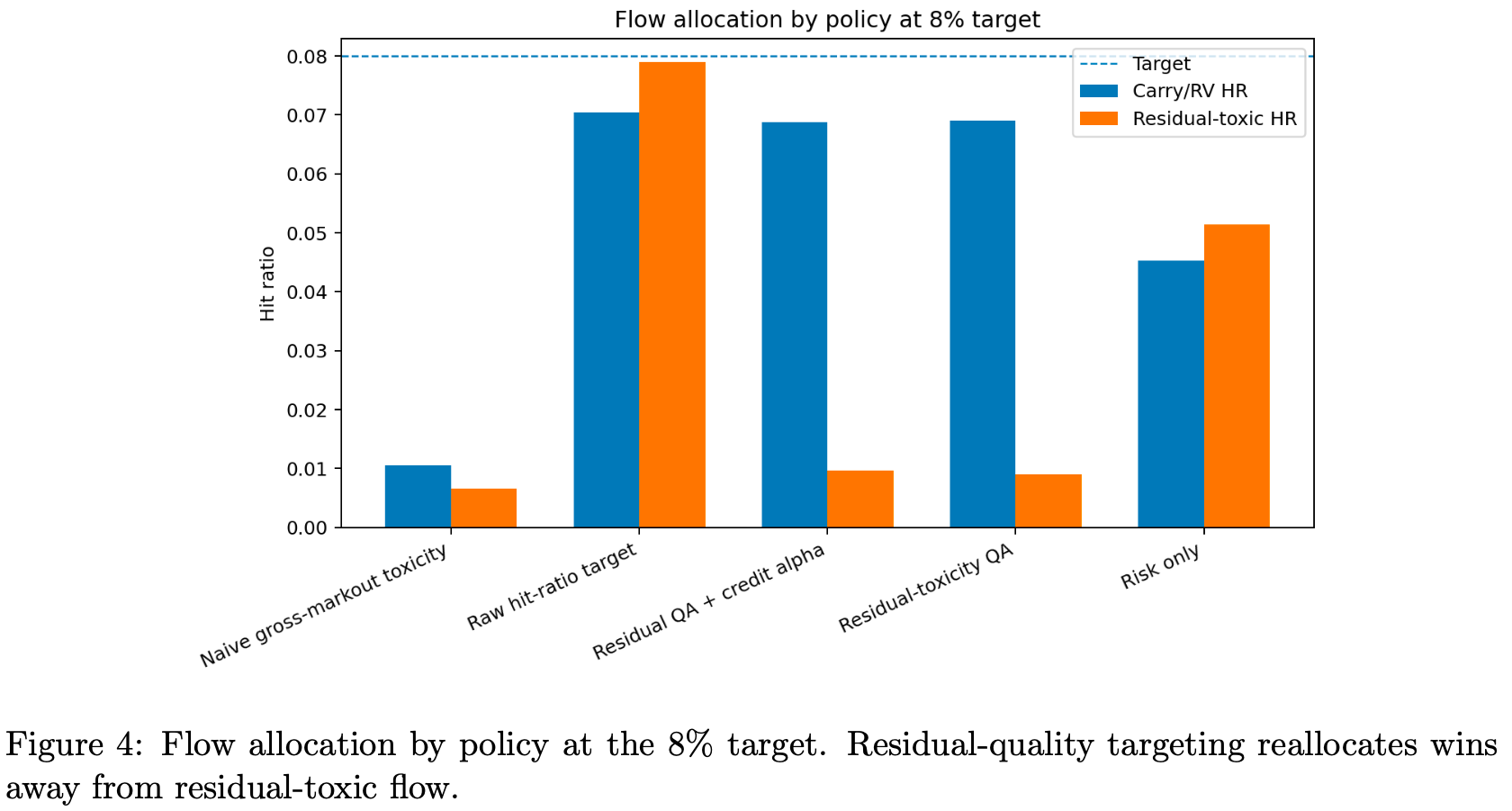

Credit Alpha and Hit-Ratio Targeting

Standard corporate bond market-making targets can severely hurt profitability because winning an order from a highly informed trader costs significantly more than winning one from a retail investor trading for simple rebalancing reasons.

Electronic bond market makers typically use a “hit ratio,” the percentage of client requests they win, as their primary metric for success. However, treating all client flow equally forces dealers to aggressively quote and inadvertently subsidize highly informed, toxic order flow. By replacing raw targets with a residual-quality-adjusted metric, we can mathematically strip out public credit factors, carry, and index trends from post-trade performance, isolating true client toxicity. When tested in a multi-bond framework, this quality-adjusted pricing naturally tightens quotes for low-risk, inventory-recycling clients while widening out against toxic counter-parties.

Shifting focus from raw volume to residual quality allows a desk to achieve its client service mandates while dramatically cutting adverse-selection costs, turning a rigid institutional metric into an optimized, risk-aware profit driver. Niang concludes that a uniform raw target is bad especially when the economic quality of fills is heterogeneous and suggests that the optimal strategy would be to “subsidize service selectively for low-residual-toxicity, recyclable, and forecastable flow” opposed to blindly chasing every hit.

Niang, Bouna, Residual-Quality-Adjusted Hit-Ratio Targeting in Corporate Bond RFQ Market Making Credit Alpha, Client Flow Quality, and Style-Aware Warehousing (May 19, 2026). Available at SSRN: https://ssrn.com/abstract=6815279 or http://dx.doi.org/10.2139/ssrn.6815279

Liquidity Provision in Korean Retail Markets

In retail-dominated markets like South Korea, foreign institutional investors act as primary liquidity providers in illiquid stocks, earning significant short-term premiums for absorbing local order imbalances.

In the US, retail traders typically act as the marginal liquidity providers, stepping in to absorb order flow from big institutions and earning a small premium when the market overextends. This paper flips that dynamic on its head by analyzing eleven years of weekly trading data from the Korean equity market, which is structurally dominated by domestic retail volume.

The researchers found that when foreign investors aggressively buy less liquid Korean stocks, those same equities experience positive abnormal returns over the following week. This isn't necessarily a sign of superior fundamental intuition, but is actually classic, risk-averse liquidity provision. Foreigners are stepping up to absorb order flow pressure in corners of the market where immediacy is expensive, trading against contemporaneous price moves to pocket a temporary concession.

This structural behavior becomes starkly apparent when tracking the holding horizons, as the abnormal per-week alpha decays eighteenfold from the first week to the twelfth week. This highlights that “the foreign abnormal return reflects compensation for risk-averse liquidity provision” rather than a slow, structural repricing of fundamental information. For global investors navigating emerging or retail-heavy cross-sections, it serves as a reminder that the identity of the stabilizing marginal trader is highly dependent on local market architecture.

Sujin, Pyo and Lee, Woojin, Who Provides Liquidity in Retail-Dominated Markets? Evidence from Korea. Available at SSRN: https://ssrn.com/abstract=6885262 or http://dx.doi.org/10.2139/ssrn.6885262

Hedge Funds in Debt

The Federal Reserve’s monetary policy stances dictate hedge fund exposures to corporate and sovereign debt, transforming these funds into central transmitters of market shocks during modern tightening cycles.

The Federal Reserve's post-2015 money market operations have fundamentally tightened the link between monetary policy and hedge fund behavior. When the central bank adopts a hawkish stance, rising short-term rates systematically drive expansionary bond market exposures across nearly all major fund strategies. This relationship shifts the focus away from traditional alpha generation toward a highly policy-sensitive setup.

This shift is particularly acute in corporate debt markets, where higher rates coincide with increased fund sensitivity to credit factors. However, this dynamic changes drastically during market stress. During crises, funding liquidity from prime brokers dries up or becomes prohibitively restricted, causing funds to aggressively shed debt holdings, withdraw leverage, and shift capital into cash.

Consequently, structural shifts in the post-pandemic era have transformed hedge funds from net absorbers of market noise into prominent net transmitters of idiosyncratic volatility to the broader financial ecosystem. Noori specifically emphasizes that modern debt markets exhibit a “stronger and more policy-sensitive HF role in bond markets.” This dynamic footprint matters deeply for market participants, as modern fixed-income stability is now intrinsically linked to the regulatory and speculative leverage cycles of non-bank financial intermediaries.

Noori, Mohammad, Hedge Funds in Debt (May 30, 2026). Available at SSRN: https://ssrn.com/abstract=6858498 or http://dx.doi.org/10.2139/ssrn.6858498

Volatility Drag and the Admissible Financing Boundary

A disciplined, rule-based borrowing policy implemented after market drawdowns can systematically recover the wealth lost to compounding volatility drag without increasing the long-term risk of ruin.

Modern Portfolio Theory beautifully explains what assets to hold, but it leaves us completely stranded when the path goes sideways. Every risky portfolio suffers from a hidden tax known as volatility drag, or Itô's Zeta, which automatically shaves a chunk off your compounded returns over time. For instance, a diversified portfolio with 15% volatility faces a predictable math drag of exactly 1.125% per year, turning a theoretical million-dollar nest egg into a significantly smaller realized sum over a thirty-year horizon.

While traditional finance treats this drag as an unalterable cost of doing business, this paper demonstrates that we can fight back using a mechanical, second-mover financing rule. By establishing an arithmetic benchmark of where the portfolio should be and borrowing small, strictly bounded amounts to maintain equity exposure only after the market drops, investors can generate “McKean's Alpha” to offset the drag.

The raw model is annoyingly difficult to beat, provided you follow a precise deviation rule rather than just blindly buying dips. In extensive simulations across thirty-year horizons, a precise rebalancing rule recovered virtually 100% of the volatility tax even under steep 9% borrowing costs. However, the math has a hard ceiling, meaning that “disciplined financing restores the path, and excessive financing ends in ruin.” For investors, this changes the entire game, as volatility shouldn't just be feared as a risk metric, because it can actually be utilized as the raw material for path optimization, proving that a structured financing policy is just as vital to lifetime wealth as asset allocation.

Anderson, Thomas, Volatility Drag and the Perpetual Borrowing Option: The Admissible Financing Boundary (May 18, 2026). Available at SSRN: https://ssrn.com/abstract=6795058 or http://dx.doi.org/10.2139/ssrn.6795058

This week for paid subscribers

Paid subscribers are getting a look at whether prediction markets can forecast macroeconomic data more accurately than professional economists. We run Diebold-Mariano and probability calibration tests on Kalshi distributions to evaluate their predictive edge over the Survey of Professional Forecasters across inflation, unemployment, and Fed rate decisions. Python backtest code included.

Disclaimer: The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.