Recent Academic Research

Changing returns from raw to standardized, bitcoin ETF flow impacts, safe haven assets, and the inherent convexity in the S&P 500

Welcome back to another issue of Recent Academic Research! Let’s get into it.

Redefining Returns

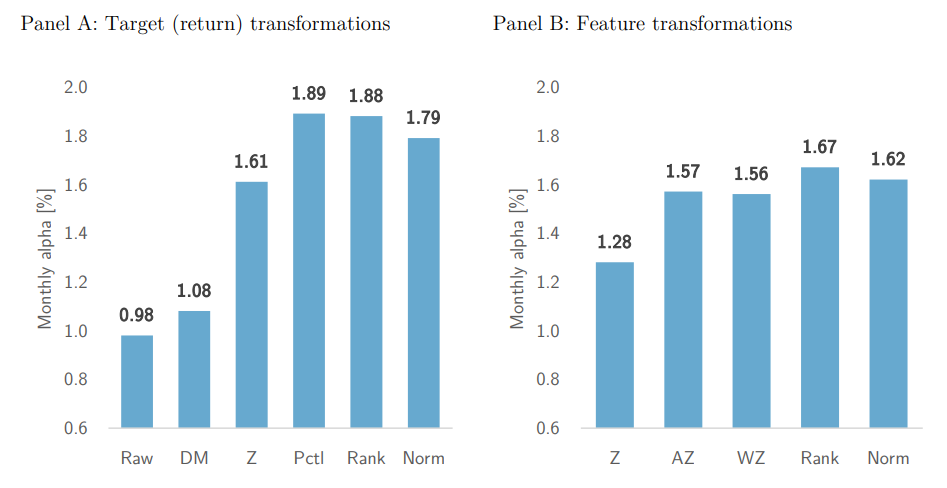

Defining target returns as relative ranks rather than raw values can nearly triple the predictive accuracy of machine learning models.

While most quant researchers focus on cleaning and scaling stock characteristics, this study reveals that how you define your target is actually the primary driver of performance.

By switching from raw returns to rank-based or standardized targets, models can filter out common market noise and focus on what actually matters: which stocks outperform their peers within a specific month. This shift is particularly powerful for nonlinear models (like random forests) which can fail entirely when presented with raw, heavy-tailed data but thrive once targets are stabilized.

However, ranking is not a universal solution because it discards information about the actual magnitude of price moves. This loss is costly in volatile segments like micro-cap stocks or emerging markets where extreme outcomes contain genuine economic signals rather than just noise.

Ultimately, the best transformation depends on the return distribution of the specific market (investors who ignore the shape of their data risk optimizing for the wrong objective).

Cakici, Nusret and Zaremba, Adam, Getting the Target Right in Return Prediction (April 20, 2026). Available at SSRN: https://ssrn.com/abstract=6615698 or http://dx.doi.org/10.2139/ssrn.6615698

Safe Haven Assets

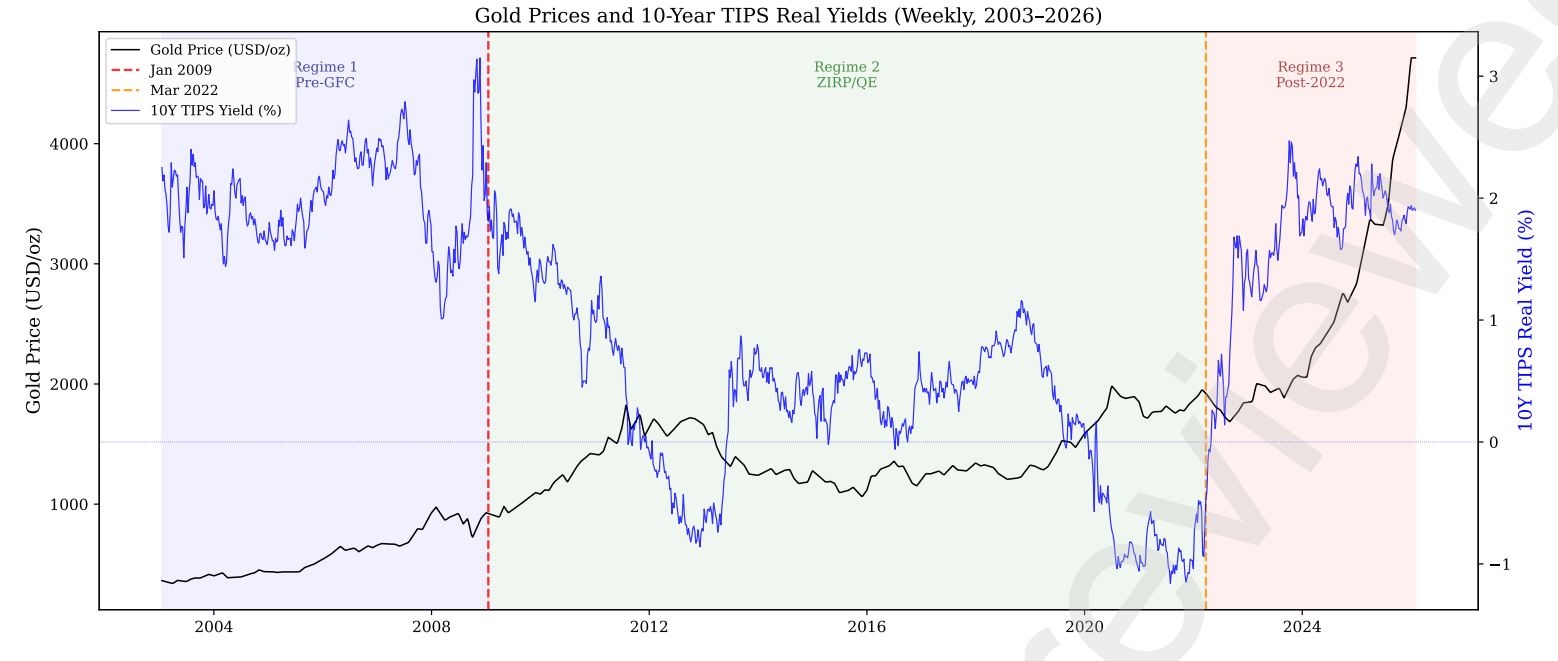

The historical relationship between gold and Treasury yields is not a constant market law but a regime dependent one that only activates when real interest rates are exceptionally low or negative.

While gold is often viewed as a simple inverse play on interest rates, this study reveals that the two assets only behave as rivals under specific conditions. By examining global data, the researchers identified three distinct eras where the link between gold and bonds fundamentally shifted.

During the era of near zero interest rates following the global financial crisis, gold and Treasuries acted as close substitutes because a scarcity of safe options forced investors to choose between them based on small yield differences. However, before that crisis, the two assets actually moved in the same direction because they both responded to broader market stress.

Most striking is that this relationship has decoupled in recent years. Despite the return of positive real yields, gold prices have surged due to central bank demand and geopolitical risks rather than interest rate moves.

This breakdown means that relying on old correlations to hedge a portfolio can be dangerous. Investors must recognize that gold’s role in a portfolio is not static (it adapts to the broader supply and demand for safety).

Batten, Jonathan A. and Lončarski, Igor and Szilagyi, Peter G. and Zhou, Han-Xian, Gold and U.S. Treasuries as Competing Safe Assets. Available at SSRN: https://ssrn.com/abstract=6627301 or http://dx.doi.org/10.2139/ssrn.6627301

S&P 500 Convexity

The S&P 500 systematically outperforms active managers not because of superior stock selection, but because its passive structure preserves the outsized, “convex” returns of winning stocks that professional managers are forced to trim.

The persistent failure of active managers to beat the benchmark is usually blamed on fees, but this research suggests even the most gifted stock pickers are being sabotaged by their own structural constraints.

The authors introduce the “convexity gap,” a phenomenon where professional fund rules (such as five percent position limits and style mandates) force managers to sell their biggest winners prematurely.

While the S&P 500 naturally allows a single high performer to compound from a tiny fraction of the index into a massive driver of returns, active funds are structurally required to “cut their flowers” and redistribute that capital into laggards. It is a bit humbling to realize that the index often wins simply because it is too passive to interfere with its own success.

Data shows that nearly 70 percent of institutional accounts underperform even before fees are taken into account. This suggests that the primary engine of market wealth is the outsized growth of a few extreme winners, which active management is designed to prune away.

Milligan, Nina and Milligan, Michael, The Convexity Gap: How the S&P 500 Preserves Convexity and How Active Managers Can Too (April 03, 2026). Available at SSRN: https://ssrn.com/abstract=6543859 or http://dx.doi.org/10.2139/ssrn.6543859

Bitcoin ETF Flows

An inflow of one hundred million dollars into Bitcoin ETFs typically triggers a fifty-three basis point price jump, but this immediate impact is actually a temporary surge masked by a relentless cycle of new money.

The launch of spot Bitcoin ETFs created a direct bridge between traditional brokerage accounts and digital asset prices, establishing a measurable link where investor demand dictates market movement.

This research quantifies that connection, finding that every hundred million dollars in net flows explains roughly twenty-one percent of daily price variation.

More interestingly, the study identifies a “flow-persistence illusion” where price jumps appear permanent only because new money arrives in waves, hitting the market before previous shocks have a chance to reverse.

While individual trades move the needle temporarily, the consistency of institutional flows creates a cumulative drift that nearly doubles the initial impact over ten days. This discovery suggests that ETFs act as a momentum machine, where initial price gains attract further inflows in a self-reinforcing feedback loop.

Lim, Boon Chuan, The Price Impact of Spot Bitcoin ETF Flows. Available at SSRN: https://ssrn.com/abstract=6592830 or http://dx.doi.org/10.2139/ssrn.6592830

This week for paid subscribers

Paid subscribers are working through a two-part event study on Treasury auction bid-to-cover ratios — measuring the impact on USD and SPY across 574 auctions from 2015 to present. Code included.

Disclaimer: The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.