Recent Academic Research

Using inflation in high-debt regimes, ML for investment factors, and gamma exposure's impact on bitcoin spot prices

Welcome back to another issue of Recent Academic Research! Let’s get into it.

Machine Learning for Value vs. Growth

The line between value and growth stocks is blurrier than index providers admit, but a clever clustering algorithm might finally sharpen the picture.

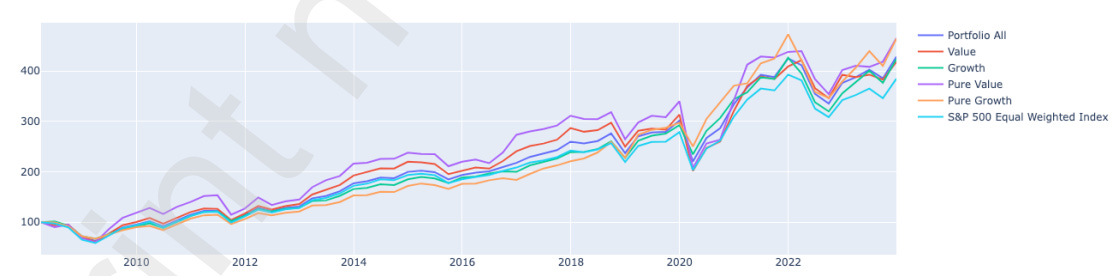

We generally classify stocks using simple, linear rules, assuming that a low P/E ratio automatically equals “value” and high revenue momentum equals “growth.” This paper argues that such one-dimensional sorting misses the complex, multivariate reality of modern markets.

The authors deploy an unsupervised machine learning technique called K-Means clustering to sort S&P 500 stocks, but with a critical mathematical twist. Instead of measuring the distance between data points using standard geometry, they use a method that accounts for how financial metrics naturally move together (correlations).

This hybrid approach creates much more stable clusters than traditional methods. When the researchers built a “Pure Growth” portfolio based on these stricter mathematical clusters, it significantly outperformed standard S&P style indices on a risk-adjusted basis from 2008 to 2023. It serves as a reminder that while the market is noisy, better categorization tools can still extract alpha from the chaos.

Weibel, Marc and Nyffeler, Lionel, Enhancing Value-Growth Stock Classification Using K-Means Clustering with Mahalanobis Distance. Available at SSRN: https://ssrn.com/abstract=5787311 or http://dx.doi.org/10.2139/ssrn.5787311

Optimal Policy in High-Debt Economies

When public debt hits the ceiling, a little inflation might not be an accident, but a necessary policy tool.

The economic playbook changes drastically depending on how much red ink is already on a nation’s balance sheet. By comparing the United Kingdom’s economy in 2007 against the high-debt reality of 2021, this research highlights a difficult constraint for policymakers.

In a low-debt environment, governments can comfortably borrow to smooth out economic shocks. However, when debt is already sky-high, that fiscal space evaporates. The researchers utilized a complex model to demonstrate that when tax hikes are politically or structurally impossible, the “optimal” policy response shifts toward allowing inflation to run hotter.

This essentially acts as a hidden tax that erodes the real value of the debt burden. The study finds that in these constrained scenarios, moderate inflation becomes an “endogenous and welfare-improving adjustment mechanism” rather than a failure of policy. This suggests that in high-debt regimes, betting on a swift return to low inflation might be fighting the government’s only viable survival strategy.

Rodrigues, Diego and Rodrigues, Diego, Loving or Fighting Inflation: Optimal Policy in High- and Low-Debt Economies. Available at SSRN: https://ssrn.com/abstract=5801558 or http://dx.doi.org/10.2139/ssrn.5801558

Bitcoin Gamma Walls

Do gamma walls influence the underlying cryptos?

There is a persistent belief in cryptocurrency circles that gamma walls influence the underlying due to the hedging activities of market makers.

Gamma, the second derivative of option value with respect to the underlying price, measures the sensitivity of an option’s delta to changes in the spot price. Market makers, who typically maintain delta-neutral positions, must continuously hedge their gamma exposure by buying or selling the underlying asset. When gamma exposure concentrates at particular strike prices, theory suggests these “gamma walls” may increase volatility (due to market makers’ short gamma exposure) or decrease volatility (due to market makers’ long gamma exposure).

This research runs the actual numbers on Deribit order flows and finds the theory completely lacking. While gamma squeezing is a very real phenomenon in equity markets (like the S&P 500) where options volume often exceeds spot volume, the crypto market structure is fundamentally different, due to 24/7 trading and lower option volume.

The study reveals that the hedging required by market makers amounts to roughly 0.025% of daily Bitcoin volume, a figure far too small to push the spot price around. The author concludes that these “gamma effects remain economically negligible” in Bitcoin.

Lachowicz, Pawel and Lachowicz, Pawel, Do Gamma Walls Actually Move Bitcoin Prices at Deribit? (November 21, 2025). Available at SSRN: https://ssrn.com/abstract=5782822 or http://dx.doi.org/10.2139/ssrn.5782822

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.