Recent Academic Research

The Beige Book's forecasting power, analyst impact on bond demand, a value premium in Brazil, and the long-horizon risk of bonds

Welcome back to another issue of Recent Academic Research! Let’s get into it.

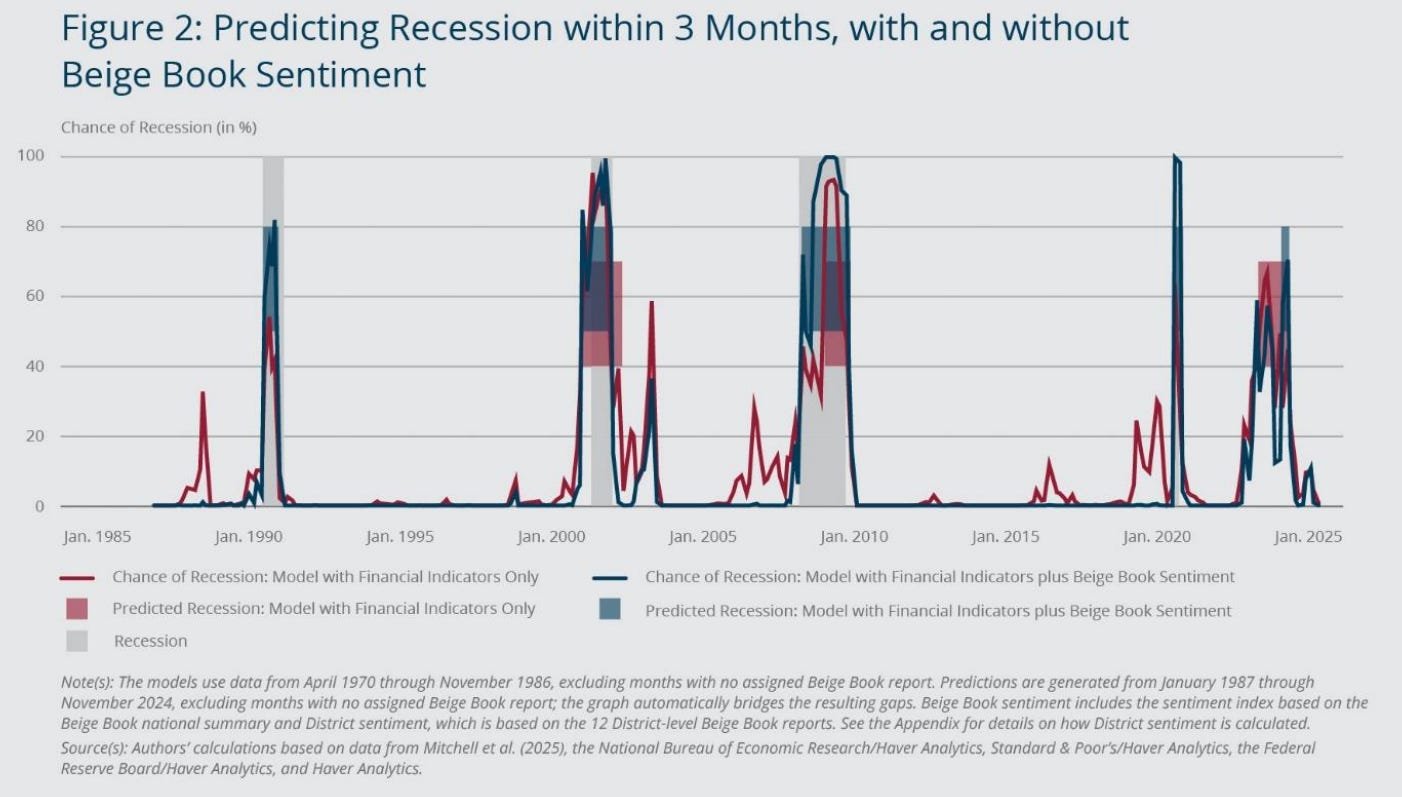

Forecasting Recessions with The Beige Book

Can the Federal Reserve’s qualitative Beige Book actually predict recessions better than hard financial data?

Researchers at the Boston Fed investigated whether the anecdotal economic summaries in the Beige Book add real forecasting power. By converting the report’s text into a quantitative sentiment index, they tested it against established recession models that rely on financial indicators like the Treasury term spread.

The answer is a clear “yes,” but with a crucial nuance. Adding Beige Book sentiment significantly improves recession forecasts for the short term (a three-month horizon), but its value is less clear for longer-term predictions.

A combined model that used both financial data and Beige Book sentiment had higher sensitivity (it spotted the 1990 recession, which the financials-only model missed ) and greater specificity (it flashed fewer false alarms during the 2022-2023 period ).

The study also found the most valuable information comes from the individual District reports, not the national summary, suggesting that “subjective factors” and business confidence on the ground offer a predictive edge that quantitative models miss.

Burke, Mary A. and Nelson, Nathaniel R. and Nelson, Nathaniel R., The Beige Book’s Value for Forecasting Recessions (November, 2025). Federal Reserve Bank of Boston Research Paper Series Current Policy Perspectives Paper No. 25-15, Available at SSRN: https://ssrn.com/abstract=5715584

Equity Analysts and Investor Demand

Do equity analysts, who focus on stocks, surprisingly hold the keys to driving demand in the corporate bond market?

This paper examines whether the work of equity analysts shapes investor demand for new corporate bonds. Using novel orderbook data, researchers found that greater analyst coverage and higher forecast accuracy significantly increase a bond’s oversubscription rate.

In contrast, high forecast dispersion (when analysts disagree) significantly reduces investor demand. The study argues this supports the “bright side view” that analysts reduce information asymmetry for all investors, not just equity traders.

The real insight, however, comes from when analysts matter most. Their influence is amplified in situations where information is murky, such as for firms with low ESG scores, high carbon emissions, or high stock price volatility.

Conversely, for bonds with high intrinsic transparency, like green bonds, the analysts’ impact was muted or nonexistent.

Cumming, Douglas J. and Kashefi-Pour, Eilnaz and Neupane, Biwesh and Zhou, Haoying, The Impact of Analysts on Investor Demand in the Corporate Bond Primary Market (November 12, 2025). Available at SSRN: https://ssrn.com/abstract=5739462 or http://dx.doi.org/10.2139/ssrn.5739462

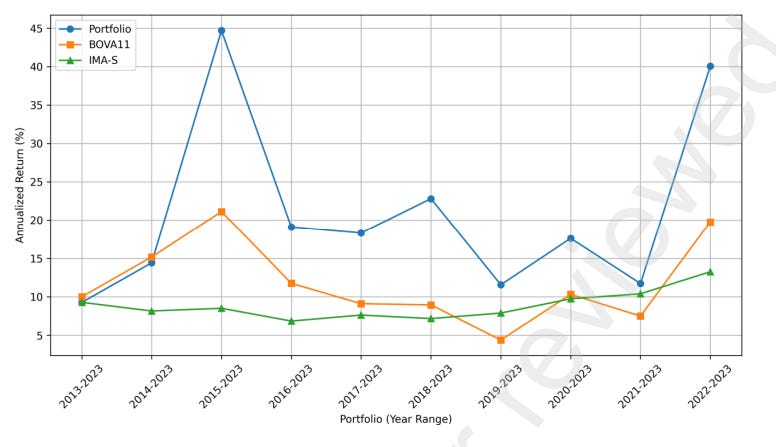

Value Investing Outperforms in Brazil

Can a simple, defensive value investing strategy based on Benjamin Graham’s rules still beat the market (and bonds) in Brazil?

Researchers tested a classic “defensive investor” strategy in the Brazilian equity market from 2013 to 2023. They built ten separate annual portfolios using strict Graham-inspired criteria: a low P/E x P/B multiple (<=22.5), a high current ratio (>2), and low debt (liabilities < equity).

They then compared these portfolios’ returns against the main stock market ETF (BOVA11) and a Treasury bond index (IMA-S). The value strategy worked exceptionally well. Over the full period, nine out of the ten annually-built portfolios outperformed both benchmarks. The strategy’s cumulative return was 152.48%, decisively beating BOVA11’s 87.57% and IMA-S’s 63.66%. (These results were after researchers removed one massive outlier stock to be more conservative ).

The strategy also delivered superior risk-adjusted performance, with eight of the ten portfolios achieving a higher Sharpe ratio than the market index. The main drawback was a lack of diversification; during the pandemic, for instance, the strict rules found only three qualifying stocks. Still, the findings confirm that “a value premium was observed” and that a disciplined, fundamental approach provided a statistically significant edge.

Anjos, Alexandre and Anjos, Alexandre and Sales, George and Nakamura, Wilson and Machado, Luciana, Value Premium: Evaluating Long-Term Returns Based on Value Investing Indicators Compared to Benchmarks. Available at SSRN: https://ssrn.com/abstract=5747601 or http://dx.doi.org/10.2139/ssrn.5747601

Bond Variance

Does holding long-term bonds really get less risky the longer you hold them?

This study challenges the conventional wisdom that bonds are a “safe” long-term hold by looking at risk from an ex-ante perspective. Instead of just measuring past volatility, researchers built a model to estimate the predictive variance (all the uncertainty an investor actually faces about the future) for a U.S. investor holding unhedged long-term foreign bonds. Their model used over two centuries of data and, crucially, included both observable predictors (like interest rate spreads) and unobservable predictors meant to capture massive, unpredictable regime shifts.

The analysis found that, contrary to popular belief, the predictive variance for long-term bonds grows significantly with the investment horizon. Any potential benefit from mean reversion (which would make bonds safer over time) is “outweighed by uncertainties in interest rate differentials and exchange rate returns”.

The single dominant source of this long-term risk was found to be the “unobservable predictors”, suggesting that big, unforeseen shifts in monetary and exchange rate regimes are what should really keep long-term bond investors up at night.

Della Corte, Pasquale and Gao, Can and Preve, Daniel P. A. and Valente, Giorgio, What 200 Years of Data Tell Us About the Predictive Variance of Long-Term Bonds (June 01, 2025). SAFE Working Paper No. 460, Available at SSRN: https://ssrn.com/abstract=5734512 or http://dx.doi.org/10.2139/ssrn.5734512

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.

Regarding the Beige Book research, it is fascinating to see the predictive power derived from qualitative data. Did the study also examine potential biases in how that anecdotal information is initialy collected or reported?

Interesting studies 👍🏻