Recent Academic Research

Sunset-driven bond mispricing, crypto forecasting with Reddit sentiment, the dollar's security premium, and the partisan cost of CEO activism

Welcome back to another issue of Recent Academic Research! Let’s get into it.

Sunsets and Municipal Bonds

In a striking example of investor myopia, municipalities with later sunset times enjoy lower borrowing costs, even though that late light increases the long-term economic risks from social jet lag.

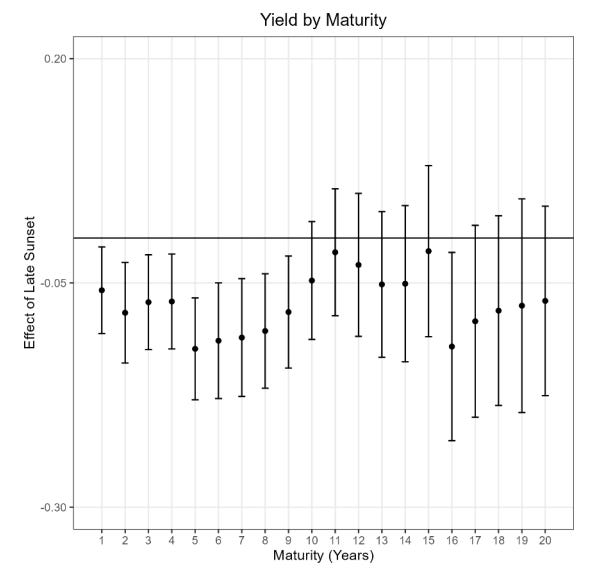

This paper explores one of the more peculiar forces in fixed income: the market impact of when the sun goes down. Using the arbitrary lines of U.S. time zone borders to isolate the effect, the research finds that counties with a later sunset pay significantly lower interest rates (lower yields) to issue municipal bonds.

This is counterintuitive, as a later sunset increases the risk of social jet lag (a chronic misalignment of sleep schedules), which correlates with poorer health and lower economic productivity, and should theoretically raise credit risk. This pricing advantage is only found in short-term bonds (under 10 years), which are primarily held by local retail investors. These investors appear myopic, focusing on the immediately tangible benefit, namely that later sunsets encourage residents to engage more in local consumption, leading to higher sales tax revenue despite no difference in total revenue.

For municipal bond investors, this highlights an overlooked behavioral anomaly and a potential systematic mispricing in the short end of the curve.

Kasten, Connor and Osborne, Banks, Is Time(Zones) Money? Sunset Times, Investor Myopia, and Municipal Bond Pricing * (September 13, 2025). Available at SSRN: https://ssrn.com/abstract=5648171 or http://dx.doi.org/10.2139/ssrn.5648171

Crypto, Sentiment, & Relative Value

Despite years of weak correlations, social media sentiment, when combined with relative discussion volume, can independently guide profitable trading in the notoriously volatile cryptocurrency markets.

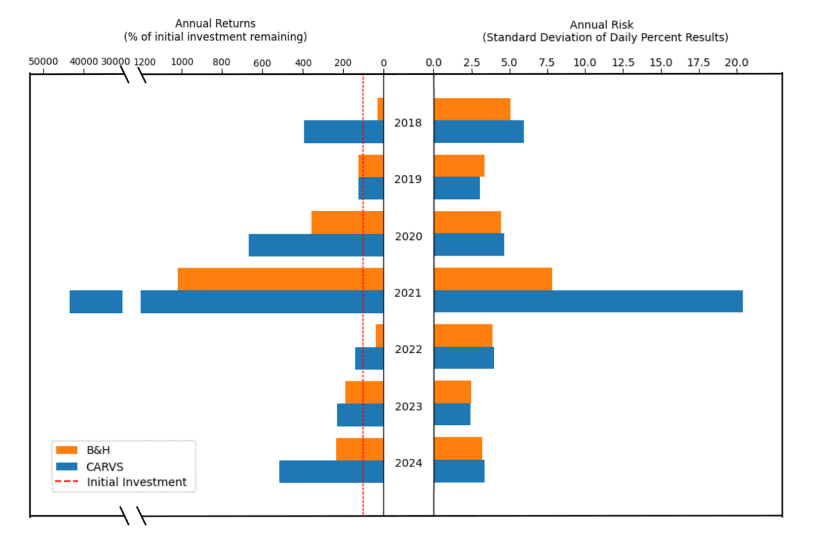

This research challenged the conventional wisdom that social media sentiment is too noisy to reliably predict crypto prices, finding instead that with a careful approach, it can be a powerful alpha signal. The authors developed a rule-based trading algorithm, CARVS (Cryptocurrency Algorithm using Relative Volume Sentiment), that analyzes the net positive or negative mood (sentiment polarity) in Reddit comments alongside the relative volume of discussion.

Between 2018 and 2024, CARVS significantly outperformed a simple buy-and-hold strategy, with annual returns improved by 1325%, 3%, 88%, 4150%, 295%, 23%, and 123% over seven years, while maintaining near-equal risk across most years.

The consistent results over a long, diverse seven-year period suggest that “social media sentiment, when properly handled, can independently guide profitable trading in volatile cryptocurrency markets”.

Noguchi, Rentaro and Noguchi, Rentaro and Mahadevu, Ashrita and Mahadevu, Ashrita and Aggarwal, Aariv and Aggarwal, Aariv and Qin, Huifang and Qin, Huifang, Forecasting Cryptocurrency Markets: An Algorithmic Approach with Reddit-Based Relative Volume and Sentiment (October 10, 2025). Available at SSRN: https://ssrn.com/abstract=5589290

Musk’s Politics and Tesla Sales

Did the CEO of the world’s most prominent electric vehicle maker alienate his core customer base and cost the company over a million units in sales?

This research quantifies the surprising financial cost of CEO political polarization, estimating the sales impact of Elon Musk’s increasingly public and partisan activities. Using county-level data on new vehicle registrations, the authors tracked how Tesla’s sales trajectory diverged in counties with high versus low shares of Democratic and Republican voters.

Over the period from late 2022 to early 2025, the Musk partisan effect is estimated to have depressed Tesla sales by 67–83%, a shortfall of over 1 million vehicles. Crucially, this wasn’t a general collapse in EV demand; the data suggests a substitution effect, as sales of other electric and hybrid vehicles rose by 17–22% over the same period.

The drop was concentrated in historically high-demand, Democratic-leaning areas, implying a large segment of the original environmentally-conscious buyer pool defected to competitors due to the CEO’s brand association.

Kenneth T. Gillingham, Matthew Kotchen, James A. Levinsohn, and Barry J. Nalebuff, “The Musk Partisan Effect on Tesla Sales,” NBER Working Paper 34413 (2025), https://doi.org/10.3386/w34413.

Global Stability and Treasuries

The dollar’s “exorbitant privilege” may not be a gift of history, but rather an explicit rent paid by the world to the U.S. for underwriting global security and enforcing contracts.

This research proposes a unified, general-equilibrium model that fundamentally links U.S. military hegemony to the persistent global imbalances and the dominance of the dollar. The core mechanism is the U.S. security umbrella, which acts as a global public good by stabilizing trade routes and strengthening the enforcement of international contracts. For allies, this reduces geopolitical risk, allowing them to redirect domestic spending toward investment and social insurance, thus stabilizing their local economies.

For the U.S., the same enforcement network creates a security-based convenience yield on dollar assets, meaning global investors accept lower yields on U.S. debt because they view dollar claims as uniquely safe and enforceable, particularly during crises. This system explains why the U.S. is the world’s largest debtor while its consumption and wealth shares rise when global stress episodes appreciate the dollar.

Kim, Sun Yong, Pax Americana: Security, Stability, and the U.S Exorbitant Privilege (October 20, 2025). Available at SSRN: https://ssrn.com/abstract=5633090 or http://dx.doi.org/10.2139/ssrn.5633090

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.

I like the paper about sunset-driven bond mispricing. It’s an impressively rigorous study.

I would argue, though, that the assumption "no observable fiscal improvement" equals "no difference between investing in the municipalities" is an oversimplification.

It’s very possible that the economic effects of boosted consumption are real and important enough to influence borrowing costs. They just weren’t reflected by coarse fiscal aggregates. But the market spotted them and priced correctly, without myopia.

When we price stocks, we pay attention to which revenue streams drive earnings. So why ignore the composition of municipal revenues?