Recent Academic Research

This week’s best academic research on financial markets

Welcome back to another issue of Recent Academic Research! Let’s get into it.

Retail Investors’ Impact on Volatility

Do retail investors talking on Reddit and Twitter actually move the market?

The rise of commission-free trading and online forums like Reddit’s r/wallstreetbets has given small-time retail investors a powerful collective voice, but does all that chatter actually translate into market-wide tremors? This study, analyzing five years of data from 2020 to 2025, suggests it does.

Researchers found a strong positive link between the volume of online discussions on platforms like Reddit and Twitter and short-term stock market volatility. Specifically, a 10% jump in online stock mentions was associated with a 2.8% increase in volatility on average. This effect was not just limited to meme-stock frenzies; it persisted across different market environments, from the stimulus-fueled rallies of 2021–2022 to the more subdued trading of 2023–2024.

The influence of retail chatter was particularly amplified during major economic events, such as Federal Reserve announcements, suggesting that the “digital crowd” has become a significant factor in how markets react to news. For investors, this means that monitoring social media sentiment is no longer just a niche strategy; it’s becoming essential for understanding and forecasting short-term market risk.

Saharkhiz, Sogand, The Impact of Retail Investors’ Online Activity on U.S. Stock Market Volatility (2020-2025) (September 08, 2025). Available at SSRN: https://ssrn.com/abstract=5457116 or http://dx.doi.org/10.2139/ssrn.5457116

Predicting Credit Spreads

Could a company’s non-financial data, like its governance score or media sentiment, be better at predicting bond risk than its balance sheet?

When it comes to predicting bond defaults, traditional credit rating agencies often lag behind the market, sometimes issuing downgrades well after a company’s financial health has clearly soured. This study suggests a better way forward by using machine learning models fed with a massive set of 167 indicators, including a novel addition of 30 non-financial data points.

These non-financial metrics cover everything from corporate governance scores and information disclosure quality to media sentiment and even the nature of a company’s ownership. The results are striking: adding this non-financial data more than doubled the predictive performance of the models. In fact, seven of the top ten most important predictors were non-financial, with corporate governance being the most critical signal.

These models effectively learned to identify high-risk traits like poor management or rising information asymmetry long before they showed up in financial statements. For investors, this shows that looking beyond the numbers to a firm’s “qualitative” data offers a powerful edge in spotting credit risk early.

Wu, Yanran, et al. “Predicting Credit Spreads and Ratings with Machine Learning: The Role of Non-Financial Data.” arXiv preprint arXiv:2509.19042 (2025).

Changing Bond-Stock Correlation

Are government bonds always a safe haven for investors?

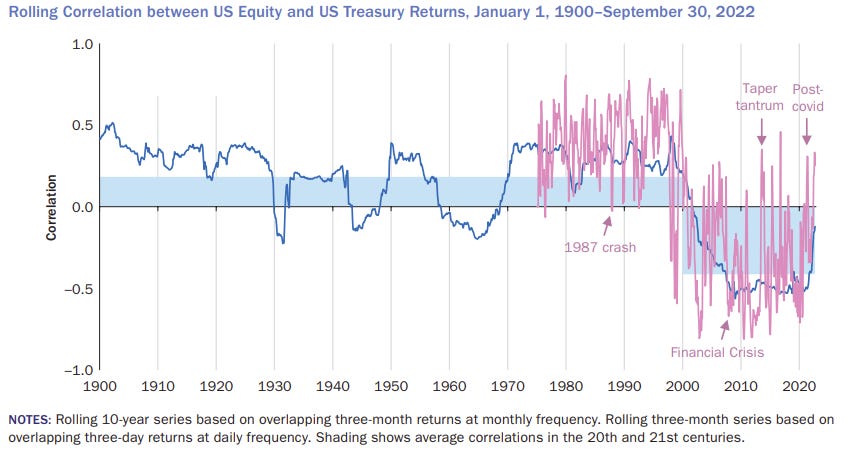

Once upon a time, stocks and government bonds moved in lockstep, both falling during tough times. But around the turn of the millennium, something flipped. Bonds started zigging when stocks zagged, becoming the reliable hedge investors have come to know and love. During the 2008 financial crisis, for example, bonds rallied while stocks plummeted, cushioning the blow for anyone holding a traditional 60-40 portfolio. The key to this shift lies in what drives the market.

Before 2000, “supply shocks” (like oil crises) made both stocks and bonds risky. After 2000, “demand shocks” (shifts in investor sentiment or economic optimism) became more dominant, causing stocks and bonds to move in opposite directions (figure below).

Now, with inflation resurfacing recently, the old positive relationship has made a brief comeback, raising questions about whether bonds will remain the safe asset they have been for the past two decades. For investors, this means the classic 60-40 portfolio’s safety isn’t guaranteed and depends entirely on the prevailing economic winds.

Campbell, John Y. and Pflueger, Carolin E. and Pflueger, Carolin E. and Viceira, Luis M., Bond-Stock Comovements (September 25, 2025). Available at SSRN: https://ssrn.com/abstract=5530338 or http://dx.doi.org/10.2139/ssrn.5530338

Volatility Forecasting Factors

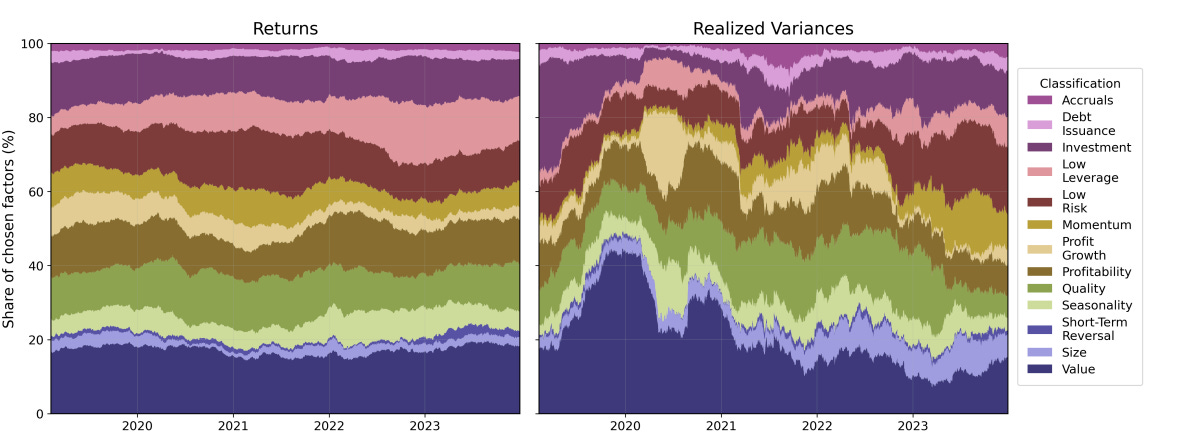

What if stock volatility isn’t just about earnings and interest rates, but also about which “story” the market is following?

Volatility is often seen as a mysterious force, but new research shows it might be more predictable than we think. By analyzing high-frequency data for 287 different market factors (think value, momentum, and size, but on a much grander scale), this study built a model that dynamically selects the most influential factor driving a stock’s volatility at any given time.

The model significantly outperformed standard forecasting methods, like the popular HAR model, because it recognizes that volatility isn’t driven by a single, static source. Instead, different factors take turns in the driver’s seat depending on the market regime.

Interestingly, the factors that best predict a stock’s future volatility are rarely the same ones that predict its future returns (figure above). This suggests that the narratives driving risk and return are often completely different. For traders and risk managers, this is a crucial insight: successfully forecasting volatility requires looking beyond an asset’s own price history to understand “the interplay between bonds’ real cash flow risks and time-varying risk premia”.

Cinquetti, Marco and Cinquetti, Marco and Hong, Seok Young and Nolte, Ingmar and Nolte (Lechner), Sandra, Volatility Forecasting Factors (September 18, 2025). Available at SSRN: https://ssrn.com/abstract=5502438 or http://dx.doi.org/10.2139/ssrn.5502438

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.