Recent Academic Research

Trading retail attention, filtering cash flow noise, targeting financial conditions, and quantifying AI's impact.

Welcome back to another issue of Recent Academic Research! Let’s get into it.

Sentiment and Investor Attention

Trading strategies based on retail investor attention generate strong short term profits, but this effect is heavily dependent on the underlying news sentiment.

Retail investors often rely on media buzz to make trading decisions, creating temporary pricing inefficiencies that quantitative strategies can exploit. This study tests a text mining strategy that buys stocks experiencing high search volume and media attention.

The authors discover that merely tracking attention is not enough to guarantee positive returns. The success of an attention driven trade relies on the emotional tone of the surrounding news.

When market attention spikes alongside positive sentiment, the trading strategy captures significant excess returns because retail buyers aggressively bid up the stock. Conversely, when the news is highly visible but negative, the strategy fails to produce the same short term gains. The authors summarize that "increased investor attention can improve the predictability of stock returns" when properly contextualized.

CHEN, Yao-Tsung and Yu, Cheng-Yen, Investigating the Interaction Effect between Sentiment and Attention on the United States Stock Market via a Trading Strategy Using Attention Words. Available at SSRN: https://ssrn.com/abstract=6437648 or http://dx.doi.org/10.2139/ssrn.6437648

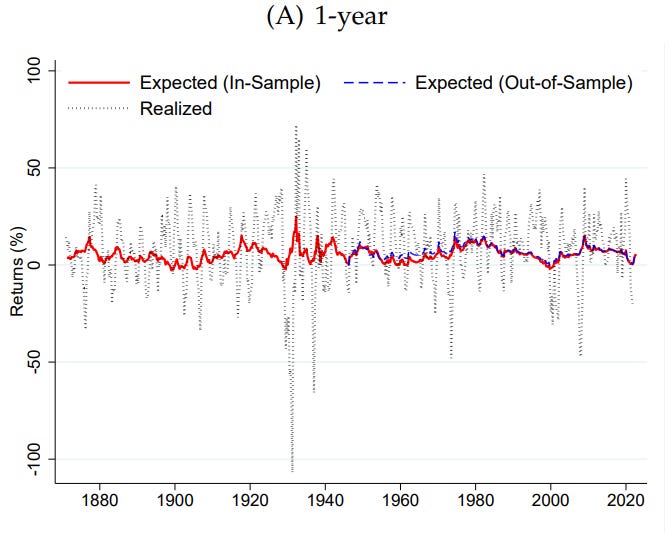

Forecasting Returns with Cash Flows

By separating permanent growth trends from temporary cycles, the predictive power of valuation metrics improves.

Asset pricing models often struggle because common metrics like the price to dividend ratio are notoriously poor and inconsistent at predicting future returns. This paper resolves the issue by proving that cash flows contain both a permanent growth trend and a short term cycle.

Researchers from Harvard and NYU demonstrate that adjusting for these underlying trends drastically improves out of sample forecasting for both short and long horizons, as the authors discovered an out-of-sample R^2 of 9% at one-year and 22% at five-year horizons.

This means the secular rise in valuation ratios over the past century is actually driven by higher trend growth rather than permanently lower discount rates.

The authors emphasize that "the apparent weakness of return predictability is an artifact of measurement error" in classic models.

Hillenbrand, Sebastian and McCarthy, Odhrain, Expected Returns with Cash Flow Trends and Cycles (March 02, 2026). Available at SSRN: https://ssrn.com/abstract=6332619 or http://dx.doi.org/10.2139/ssrn.6332619

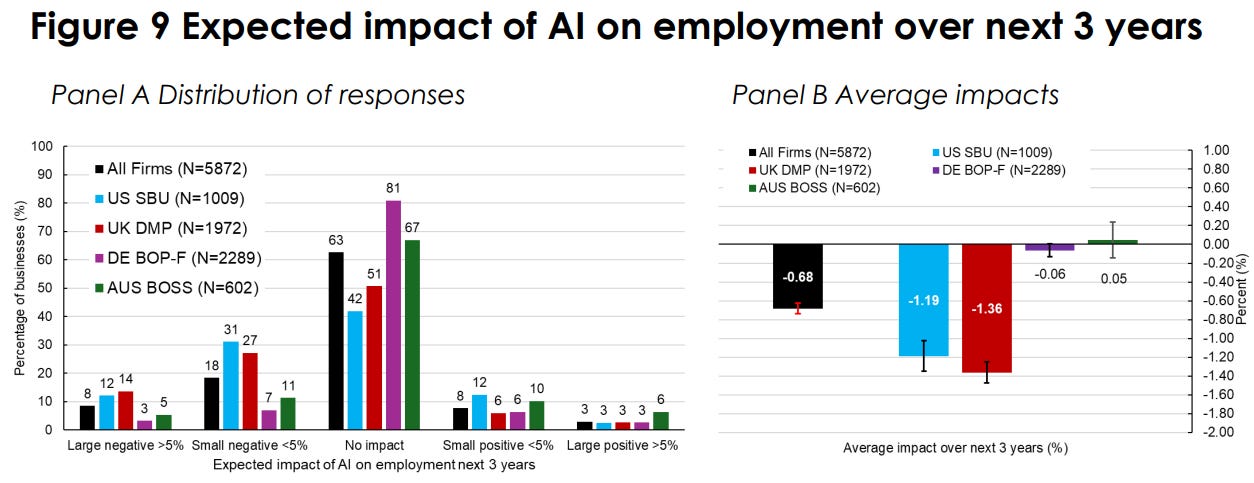

AI’s Impact on Employment

While businesses predict artificial intelligence will significantly boost future productivity, current adoption has yielded almost zero impact on employment or output so far.

There is a massive gap between the hype surrounding artificial intelligence and its measurable economic reality. Surveying thousands of executives across four major economies, researchers from various central banks (the Fed, BoE, etc.) found that while seventy percent of firms actively use these tools, the immediate economic effects are negligible.

The vast majority of business leaders report absolutely no changes to their hiring needs or labor productivity over the last three years.

Despite this muted recent past, the forward looking expectations remain incredibly optimistic. Executives forecast that these technologies will soon drive a noticeable surge in productivity and a slight reduction in overall headcount.

Interestingly, everyday employees hold a conflicting view, expecting the technology to actually create jobs rather than eliminate them. The researchers note a "sizable gap in expectations, with senior executives predicting reductions in employment" compared to their workers.

Yotzov, Ivan and Barrero, Jose Maria and Bloom, Nicholas and Bunn, Philip and Davis, Steven and Foster, Kevin and Jalca, Aaron and Meyer, Brent and Mizen, Paul and Navarrete, Michael A. and Smietanka, Pawel and Thwaites, Greg and Wang, Ben Zhe, Firm Data on AI (March, 2026). FRB Atlanta Working Paper No. 2026-3, Available at SSRN: https://ssrn.com/abstract=6466706 or http://dx.doi.org/10.29338/wp2026-03

A Better Target for Central Banks

Central banks achieve significantly better economic stability when they target a broad financial conditions index because it encourages market arbitrageurs to suppress financial noise.

This research explores how monetary policy should react to noisy financial markets in an open economy. Typically, central banks adjust interest rates to manage output gaps, which inadvertently spills volatility into connected markets like equities and foreign exchange.

The authors argue that explicitly targeting a broader financial conditions index (FCI) yields far superior macroeconomic results. When a central bank commits to this broad target, it signals to market arbitrageurs that the institution will forcefully counter non fundamental noise.

This shared commitment triggers a recruitment effect where private traders step in to stabilize prices alongside the central bank, which dampens volatility across all asset classes.

The authors find that "some degree of FCI targeting is always optimal" to smooth out market turbulence.

Ricardo J. Caballero and Alp Simsek, “Financial Conditions Targeting in a Multi-Asset Open Economy,” NBER Working Paper 34974 (2026), https://doi.org/10.3386/w34974.

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.