Recent Academic Research

Long-term macro predictability, interest rates and consumption, the automated future of labor, and institutional herding in markets.

Welcome back to another issue of Recent Academic Research! Let’s get into it.

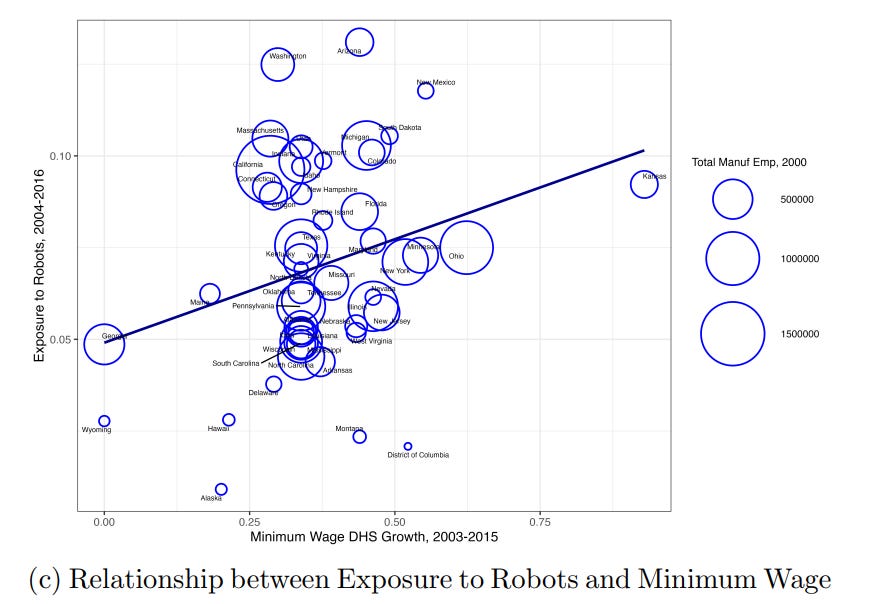

Minimum Wages and Robots

Does raising the floor on human wages increase the use of machines in the American factory?

While economists have long debated if minimum wage hikes reduce employment, this research shifts the focus to how such policies trigger technological substitution. Using U.S. Census data and robot import records from 1992 to 2021, the study compares manufacturing plants on opposite sides of state borders that face different wage floors.

The data reveals a clear "robot-substitution" effect: a 10% increase in the minimum wage leads to an 8% rise in robot adoption. This trend is most pronounced in routine-heavy production environments where labor costs are a significant portion of the overhead.

The authors find that "increases in minimum wages raise the likelihood of robot adoption in manufacturing". This suggests that labor-intensive industries in high-minimum-wage regions are prime candidates for rapid automation.

Erik Brynjolfsson, J. Frank Li, Javier Miranda, Robert Seamans, and Andrew J. Wang, “Minimum Wages and Rise of the Robots,” NBER Working Paper 34895 (2026), https://doi.org/10.3386/w34895.

Mutual Fund Investments and Momentum

In the Chinese A-share market, can following the “herd” of mutual funds actually generate alpha, or are institutional investors just chasing their own tails?

Herding behavior is often dismissed as irrational, but this study of the Chinese equity market suggests that institutional “flocking” can be a powerful signal.

The researchers found that when market sentiment is high, stocks heavily bought by mutual funds outperform those they sell by roughly 7% over the following six months. Interestingly, this outperformance does not suffer from a sharp reversal, suggesting that these funds are successfully incorporating fundamental information into prices, albeit slowly.

This slow “information diffusion” occurs because high sentiment often impairs objective processing, causing the market to take months to fully reflect institutional trades. The paper notes that “mutual fund herding behavior plays an important role in determining whether stock price momentum persists”. This could be an interesting filter to incorporate in screening tools.

Xu, Ruipeng, Mutual Fund Herding and Stock Price Momentum: The Role of Market Sentiment. Available at SSRN: https://ssrn.com/abstract=6360864 or http://dx.doi.org/10.2139/ssrn.6360864

Interest Rates and Consumption

Rate cuts make people spend more through the sudden surge in home equity

The “household debt channel” is a cornerstone of monetary policy, but its internal mechanics are often debated. By analyzing six million natural experiments in the UK where fixed-rate mortgages expired at different times, this study isolates exactly how rate changes move the needle on consumer spending.

A 1% drop in mortgage rates boosts household consumption by 3% over the following six months. Crucially, the primary driver is not the “mortgage cash flow effect” of lower monthly payments, but rather the ability of households to borrow against rising asset prices.

When rates fall, house prices typically climb, and households extract this new equity to fund everything from home renovations to non-durable goods. The researchers note that “monetary policy affects consumption in large part through asset prices and borrowing”. This highlights that the “wealth effect” from housing is far more potent than simple interest savings. It also explains the “long and variable lags” of policy, as the economic stimulus only kicks in when individual mortgage deals reset.

Angus K. Foulis, Jonathon Hazell, Atif R. Mian, and Belinda Tracey, “How Do Interest Rates Affect Consumption? Household Debt and the Role of Asset Prices,” NBER Working Paper 34911 (2026), https://doi.org/10.3386/w34911.

Long Term Macro Models

Simple models are superior for long term forecasting.

Long-run forecasting is often viewed as a “fool’s errand” due to the compounding uncertainty of structural shifts, yet it remains vital for pension funds and climate policy. This research evaluates six forecasting models using over 150 years of data across 10 macroeconomic variables, including GDP growth and interest rates.

The study finds that for stationary variables (those that tend to return to a long-term average, like GDP growth) a basic first-order autoregressive model (AR(1)) remains best for 10 to 25 years.

Conversely, for non-stationary variables like nominal interest rates, a simple random walk model (which assumes the future will look like the current value) outperforms other models.

The paper demonstrates that while no model remains perfectly accurate at the 50-year mark, simple univariate models with constant parameters can effectively quantify uncertainty for decades.

Kurt G. Lunsford and Kenneth D. West, “An Empirical Evaluation of Some Long-Horizon Macroeconomic Forecasts,” NBER Working Paper 34904 (2026), https://doi.org/10.3386/w34904.

Feedback

Thank you for reading this week’s edition of Recent Academic Research. Remember to fill out the poll to let me know which paper was your favorite and like the post if you enjoyed it.

Feel free to follow up with any questions, comments, or ideas for the future!

Disclaimer

The content provided in this newsletter, "Alpha in Academia," is for informational and educational purposes only. It should not be construed as financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. The financial markets involve risks, and readers should conduct their own research and consult with qualified financial advisors before making any investment decisions.

The interpretations, opinions, and analyses presented herein are those of the author and do not necessarily reflect the views of the original researchers, their institutions, or the full implications of the cited academic papers. While every effort is made to accurately represent the research discussed, readers should be aware that the summaries and interpretations may not capture the full scope or nuances of the original studies. The information contained in this newsletter is believed to be accurate and reliable at the time of publication, but accuracy and completeness cannot be guaranteed. The author and publisher accept no liability for any loss or damage resulting from reliance on the information provided.

This newsletter may contain links to external websites or resources. The author is not responsible for the content, accuracy, or reliability of these external sources.

By subscribing to or reading this newsletter, you acknowledge that you have read and understood this disclaimer and agree to hold the author and publisher harmless from any liability that may arise from your use of the information contained herein.