Origins of Bond Convexity and Convexity Bias

[WITH CODE] An analysis of the price-yield relationship, the Taylor Series expansion, and the structural convexity bias between futures and swaps

Reviewed and updated 25 July 2026

Hello!

Welcome back to another market investigation. Since you all loved the last series where we explained market structure with the underlying math and investigated inefficiencies, I wanted to stay on the same theme.

Today, we will discuss the price-yield relationship in bonds, how Taylor Series explain the origins of duration and convexity, convexity bias, and how to trade convexity bias.

Additionally, there are some fascinating research papers on this topic that we will explore.

Let’s get into it.

Bond Price-Yield Relationship

This post will start off simple, but gradually get more complex. Stay with me for the simple introduction; it will make sense later in the post.

Let’s say we have a stock XYZ that is priced at $100, and we buy one share of the stock. If the stock appreciates by 1% the next day, the new price is $101, and our P&L is $1. Simple.

Now, let’s say we own a zero-coupon bond with 10 years to maturity. Currently the bond yields 5%. If interest rates fall by 10 basis points (new yield is 4.90%), what is the new price of the bond? What is our P&L?

As many of you know, bond movements are not quoted in percent price changes (like stocks), but in yield changes (basis points). Crucially, a 1% change in yield does not equal a 1% change in price. Because the yield is in the denominator, the relationship is non-linear.

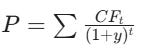

Rather, bonds are priced by summing the expected future cash flows of the bond, and then discounting them to the present value. The equation is displayed below.

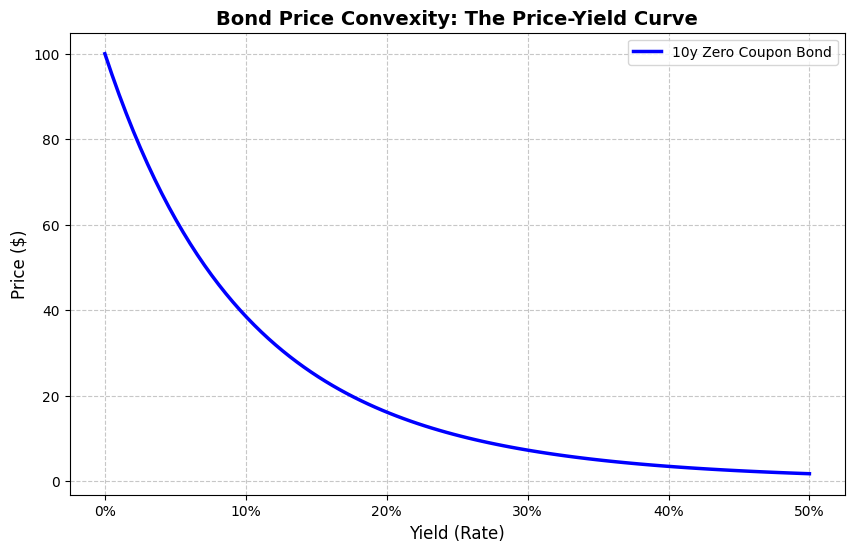

Because (1+y) is in the denominator, the function curves inward toward the origin. A depiction of this relationship is below:

Not only is there a difference in your P&L for a given 1bp move depending on what the current yield is (duration), but your gain from a 1bp fall will be greater than your loss from a 1bp rise (assuming you are long the bond).

The mathematical reasoning on why a bond has a convex relationship between price and yield is due to the price formula above, and what the derivative of the formula looks like.

Let’s say we have a linear function, where:

When you take the derivative (find the rate of change), you apply the power rule: multiply by the exponent (1) and subtract 1 from the exponent:

Therefore, the x disappears, and your “rate of change” is simply k. This relates to equities, as your P&L is (and always will be) your exposure to the stock (times the return of the stock).

However, for a bond, it is different. To see why this happens mathematically, let's simplify the complex bond formula down to its most basic structural form: an inverse function:

When you take the derivative here, the math changes because of that negative exponent.

The x stays in the equation. If you take another derivative, the x will be pushed to the cubed power. This looks similar to that of the bond price equation, which is why there is convexity in interest rates.

Because the rate of change is constantly changing based on where you are, the line must bend (positive convexity).

To summarize:

In a linear model, the variable x disappears from the risk equation, and your risk (duration) is constant.

In a convex model, the rate of change itself changes as x changes. That non-zero second derivative is the source of convexity.

This leads us into our next section.

Taylor Series Expansion

Now that we understand the “why” (the inverse relationship between price and yield), let’s look at the “how.”

To mathematically quantify this relationship, we use a Taylor Series expansion (which we used a few posts ago). In calculus, a Taylor Series allows us to approximate the value of a complex function at a new point based on its derivatives at a known point.

In our case, we want to estimate the new Price of a bond if yields change by a small amount. To do this, we treat the bond pricing formula from the previous section as a function of yield, denoted as P(y).

If we only used the first derivative (Duration), we would be assuming the relationship is a straight line. As we proved in the previous section, it is not. To get a more accurate price, we must add the second derivative (Convexity) to the equation.

Here is the Taylor Series expansion for a bond price:

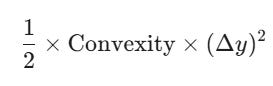

This formula might look dense, but we can translate it into the trading terms we use every day. P’(y) is the first price sensitivity, and P’’(y) is the second price sensitivity. Modified duration is −P’(y)/P(y), while convexity is P’’(y)/P(y) under this yield convention.

When we divide both sides by the Price (P) to get the percentage return, the equation simplifies into the standard risk formula used by portfolio managers:

This equation reveals the mathematical "magic" of convexity. Look closely at the second term:

For this positive-convexity bond, the squared term is positive whether rates go up (+Δy) or down (−Δy).

If rates sell off (+100bps), the Duration term hurts you, but the Convexity term adds positive value, cushioning the loss.

If rates rally (-100bps), the Duration term helps you, and the Convexity term adds even more positive value, boosting the gain.

Here’s a visualization of the price-yield relationship along with the duration and duration + convexity approximations from the Taylor Series.

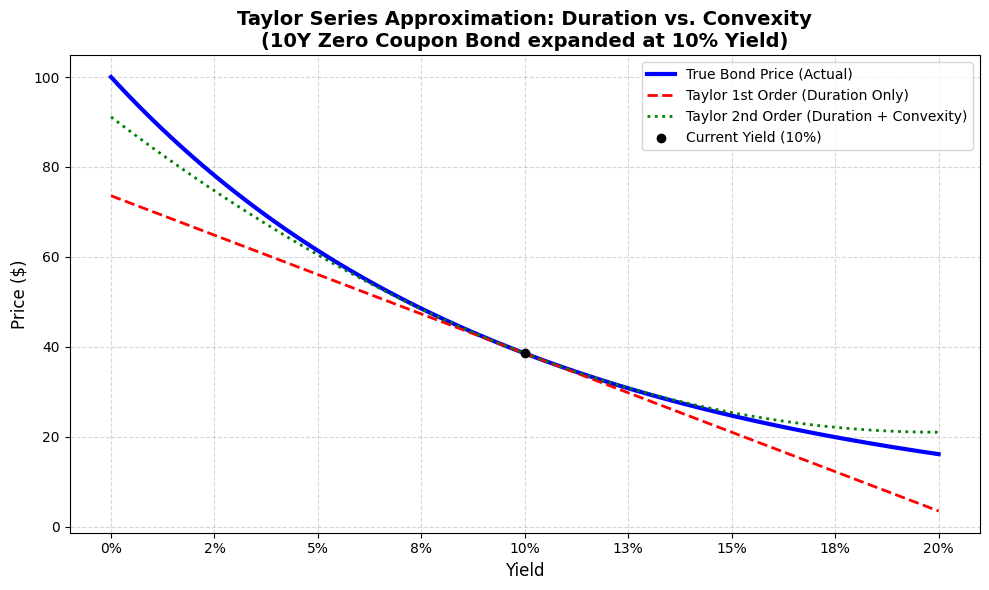

The chart above visualizes the Taylor Series in action. The Red Line (Duration) assumes a straight path, which is accurate for tiny moves, but dangerous for large ones. The Green Curve (Convexity) adds the squared term and follows the actual curve more closely near the 10% expansion point, but it still diverges for larger moves. The next omitted term is the third-order term, followed by the remaining higher-order terms.

Duration captures the first-order exposure to yield direction. Positive convexity adds value for larger moves in either direction, all else equal.

The futures-versus-forward problem is related, but it is not simply the blue bond curve against the red tangent line. The key difference is when gains and losses are settled and how future cash flows are discounted.

This phenomenon is known as the Convexity Bias.

Convexity Bias

This difference in settlement timing can create a pricing adjustment between an interest-rate future and a comparable forward rate. This is known as Convexity Bias.

The adjustment is not a free mathematical advantage attached to every swap. Its size and sign depend on the contract dates, the volatilities of the relevant rates, their correlation, and the discounting assumptions.

This brings us to the difference between Futures and forward-style cash flows. Short-term interest-rate futures are marked to market daily, so each price move produces a current variation-margin cash flow. Their quoted payoff is linear in the futures rate.

A forward rate agreement settles for a future interest period, while a swap is a series of future fixed and floating cash-flow exchanges. Those future values must be discounted, so their sensitivity also depends on the term structure used for discounting.

This is why “long a Swap” is too ambiguous. In the Burghardt and Hoskins convention, receiving fixed and paying floating is a short swap. Hedging that position with short Eurodollar futures produced positive convexity in their example, but the hedge ratio changed with rates and the position still depended on the forward rate and the zero-coupon discount rate moving together.

This yield differential is the Convexity Bias.

We can estimate how large this wedge should be under stated assumptions. Burghardt and Hoskins use a rule of thumb based on two volatilities and their correlation:

Quarterly drift ≈ σforward-rate changes × σzero-coupon returns × ρ / 4, with both annualized volatilities expressed as decimals and ρ as their correlation.

With positive correlation, the paper’s approximation puts the futures rate above the comparable forward rate. The gap grows with both volatilities, their correlation, and time to expiration; it is not determined by one variance term alone.

The spread can contain information about volatility assumptions, but it is not a direct volatility index. Curve shape, hedge ratios, basis, funding, collateral, liquidity, and model choice also matter.

Keep reading with a 7-day free trial

Subscribe to Alpha in Academia to keep reading this post and get 7 days of free access to the full post archives.