Did Bacon Kill Its Own Market?

A statistical autopsy of one of America's most famous futures contracts, using USDA cold-storage data.

Reviewed and updated 28 July 2026

Hello and welcome back to another paid post!

Today I will take a look at what a monthly USDA inventory series can—and cannot—tell us about one of America’s most famous agricultural futures contracts.

Let’s dive right in.

The Glamour Market

For about thirty years, if you wanted to gesture at the casino of commodity speculation without actually explaining anything, you reached for two words: pork bellies. It was the punchline. In Trading Places, pork bellies appear in the commodities monologue; frozen concentrated orange juice futures ruin the Duke brothers. Traders called it “the glamour market,” half in love with it and half embarrassed to be. Bellies were volatile, theatrical, and a little ridiculous, and everyone knew the name even if almost nobody could tell you what was actually in the contract.

And then, in 2011, it stopped. On 15 July, CME announced that frozen pork belly futures and options would be delisted after “a prolonged lack of trading volume” and “significant discussion with industry participants.” The infamous ticker went dark the following Monday.

The cold-storage record offers one clue. It can describe how frozen inventories changed, but it cannot establish what caused the market to disappear.

The Bet in the Freezer

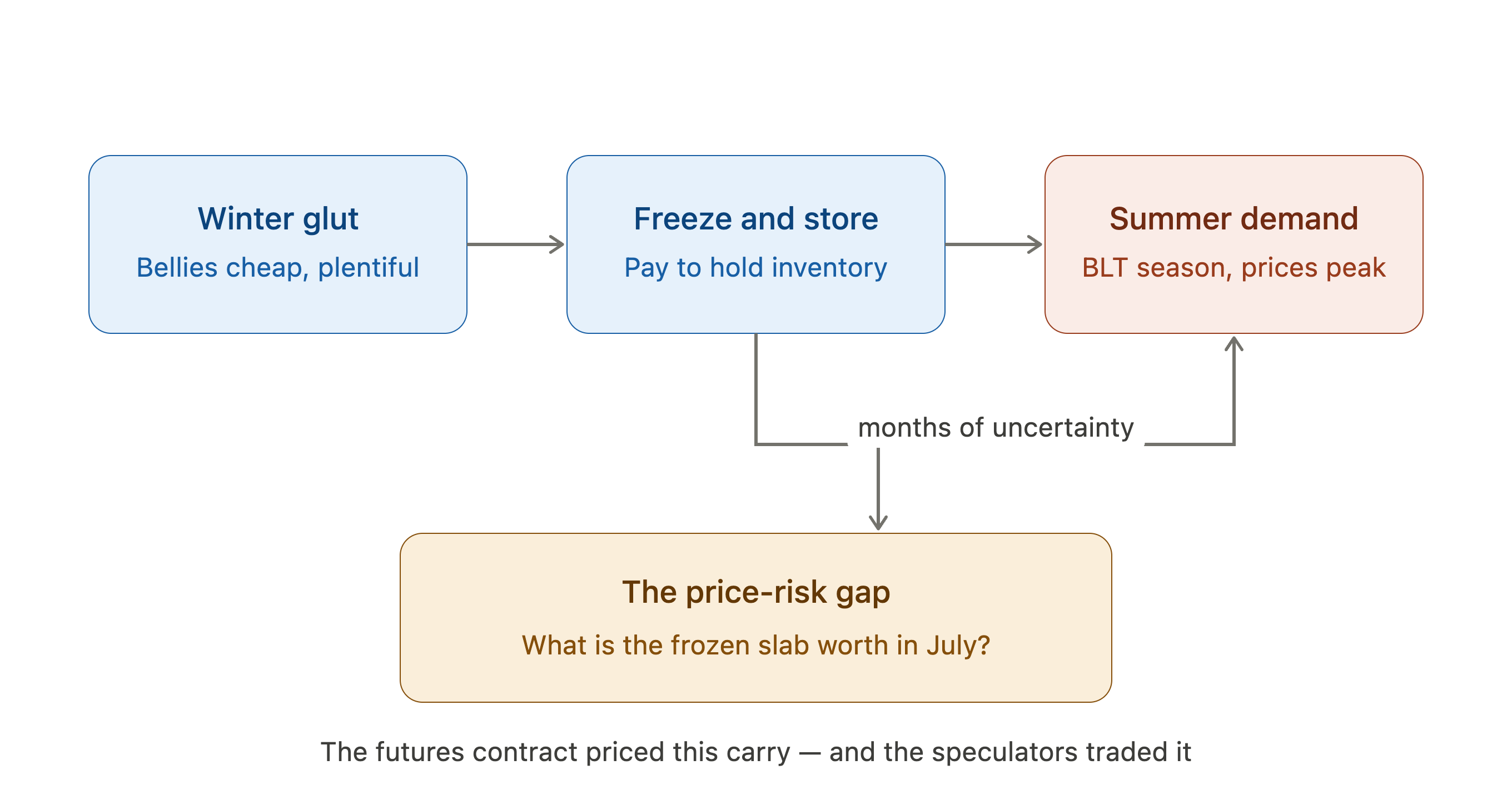

Let’s start with the thing itself. A pork belly is the slab of layered fat and muscle that runs along the underside of the hog — the cut that, cured and sliced, becomes bacon. One hog, two bellies, and for most of the 20th century a very specific scheduling headache.

The historical rationale was a seasonal inventory problem: bellies could be stored for later sale, leaving packers and buyers exposed to the price at which that inventory would eventually change hands.

Freezing does not remove that price risk; it converts a perishable product into inventory whose future value is uncertain.

That is a textbook hedging problem, the kind that can summon a futures market into existence. CME’s own history dates the first frozen pork belly futures trade to 18 September 1961. The date is fixed; the exact mix of hedging motives is a separate historical question.

The storage hypothesis goes like this: buy a belly cheap in the off-season, pay to keep it frozen, sell it dear when demand peaks. On that account, the futures curve was, in effect, the market quoting you the price of that carry. The speculators who made bellies famous would have been renting exposure to a seasonal storage cycle, dressed up in enough volatility to make it thrilling.

This explanation depends on two historical questions: whether demand and storage were seasonal, and whether firms actually used the contract to hedge that risk.

The analysis below can examine the storage series. It cannot tell us, on its own, whether a change in that series caused traders to leave the contract.

Keep reading with a 7-day free trial

Subscribe to Alpha in Academia to keep reading this post and get 7 days of free access to the full post archives.