Can You Beat the Market by Trading a Japanese Accounting Habit?

[WITH CODE] A 20-year structural backtest of the Gotobi anomaly and the Tokyo TTM Fix in USD/JPY.

Hello and welcome back to another paid post!

Today we will take a look at whether a Japanese corporate settlement tradition is associated with a recurring intraday pattern in USD/JPY.

Let’s dive right in.

The Invisible Clock of the FX Markets

Unlike equity markets, where almost every participant is driven by a singular goal, maximizing investment return, the $7.5 trillion-a-day global currency market is filled with massive players who do not care about alpha. Central banks trade to stabilize local inflation; multinational conglomerates trade to clear supply chains; international shipping firms trade simply to pay their overseas staff.

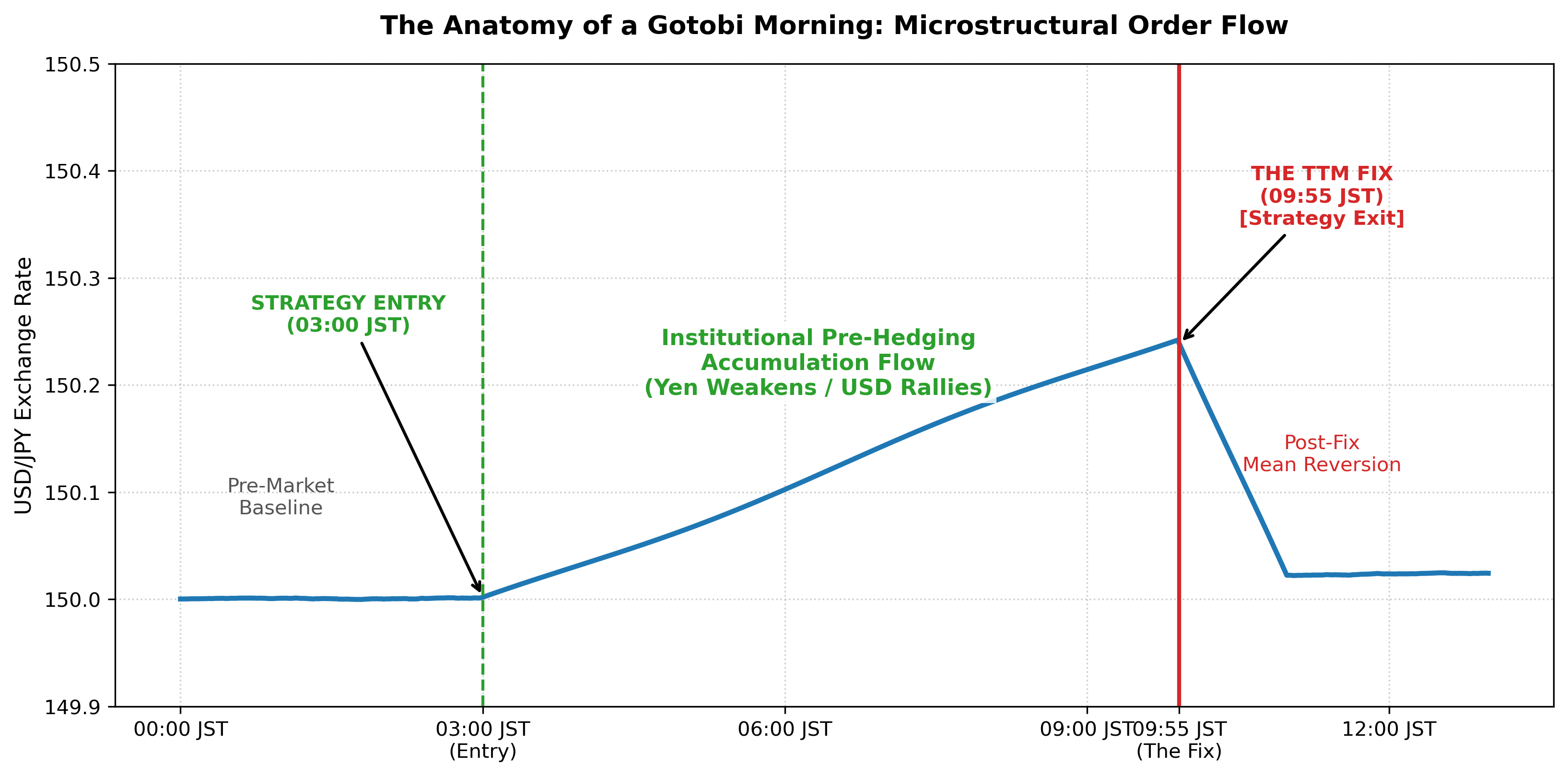

This can introduce structural non-economic flow into the market. When large, price-insensitive participants transact at similar times, they may leave footprints.

One proposed calendar effect in Tokyo is called the Gotobi Anomaly. The historical test below asks whether USD/JPY tends to rise before the stated fixing window on those dates.

The Core Microstructure Mechanic

The word Gotobi (五十日) translates literally to “days ending in five or zero.” The article’s stated calendar rule focuses on the 5th, 10th, 15th, 20th, 25th, and the final business day of the month.

The proposed mechanism is that Japanese firms with US Dollar-denominated liabilities may need to sell Japanese Yen and buy US Dollars around these dates. If that demand is concentrated, it could create a recurring rise in USD/JPY before the fixing window.

The Fix

The hypothesis centers on the Telegraphic Transfer Middle Rate (TTM), a customer exchange-rate benchmark used by Japanese banks.

For this test, the relevant fixing boundary is assumed to be 09:55 AM Tokyo Time (JST).

The proposed sequence is simple: if banks expect customer demand for US Dollars near that boundary, they may hedge beforehand, pushing USD/JPY higher. Once the window passes, that pressure may fade. The backtest examines the price pattern; it does not observe the customer orders or bank hedges directly.

Our core trading rule is beautifully simple: We buy USD/JPY at 03:00 AM JST and exit at the close of the timestamp-labeled 09:55 AM JST one-minute bar.

Keep reading with a 7-day free trial

Subscribe to Alpha in Academia to keep reading this post and get 7 days of free access to the full post archives.